The 1973 Oil Shock: the entry into stagflation

How, in 1973-1975, the United States tipped into an inflationary stagflation regime: a reading of the crisis through the Eco3min indicators.

The October 1973 oil embargo did not ignite inflation: it inflamed a price rise that was already in place. The end of Bretton Woods and the lifting of price controls had set the acceleration in motion; the energy shock turned it into stagflation, where prices and unemployment climb together while activity contracts. The U.S. regime moves from an ordinary cycle into the inflationary meta-regime.

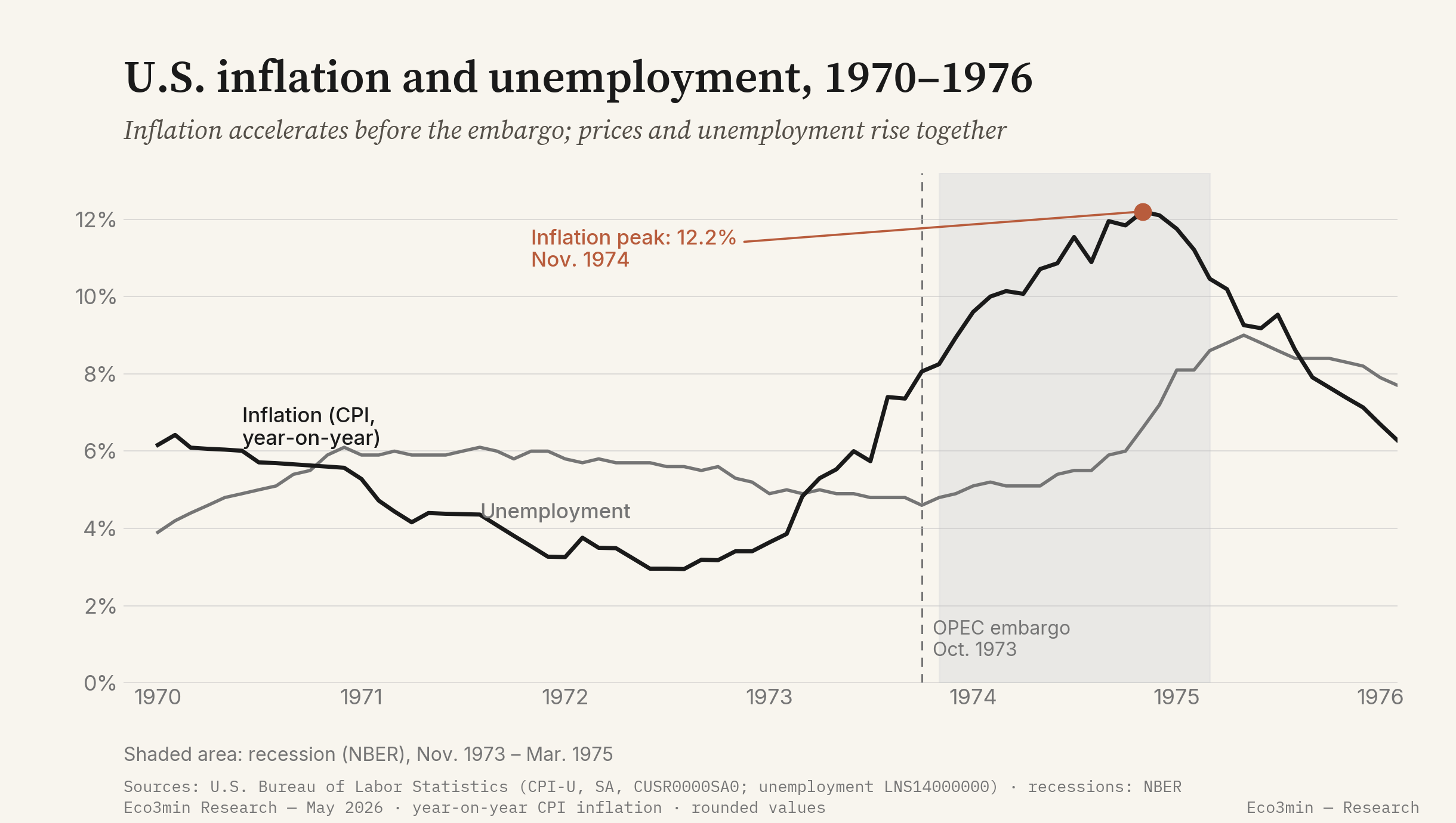

Over 1973-1975, the Eco3min cyclical grid places the United States in Stagflation (negative growth, high inflation: G− I+), within the inflationary meta-regime. The embargo declared by the Arab members of OPEC on 17 October 1973 did not create inflation: it inflamed an already-entrenched price rise, which pushed the consumer price index to 12.2% in November 1974 and unemployment to 9.0% in May 1975 (Bureau of Labor Statistics). Unlike 2008, which was disinflationary, inflation did not recede quickly: it would take Paul Volcker’s prolonged tightening, from 1979, to bring it down. Eco3min places this question within the 1986-2026 oil-inflation record.

Timeline of the regime shift

Seven milestones capture the move from an already-high-inflation regime to a stagflation entrenched for the decade.

- 15 August 1971 — Richard Nixon suspends the dollar’s convertibility into gold, ending the Bretton Woods system of fixed exchange rates. The dollar depreciates, and imported inflation adds to domestic pressures.

- Autumn 1973 — Before any oil shock, inflation is already entrenched: the consumer price index rises 7.4% year-on-year in September 1973 (Bureau of Labor Statistics).

- 6 October 1973 — The Yom Kippur War breaks out, serving as the catalyst for the Arab producers’ decision.

- 17 October 1973 — OAPEC (the Arab members of OPEC) declares an oil embargo and production cuts targeting Israel’s supporters. The benchmark crude price roughly quadruples within a few months.

- November 1973 — Activity peak dated by the National Bureau of Economic Research (NBER): the start of the recession, which will last sixteen months.

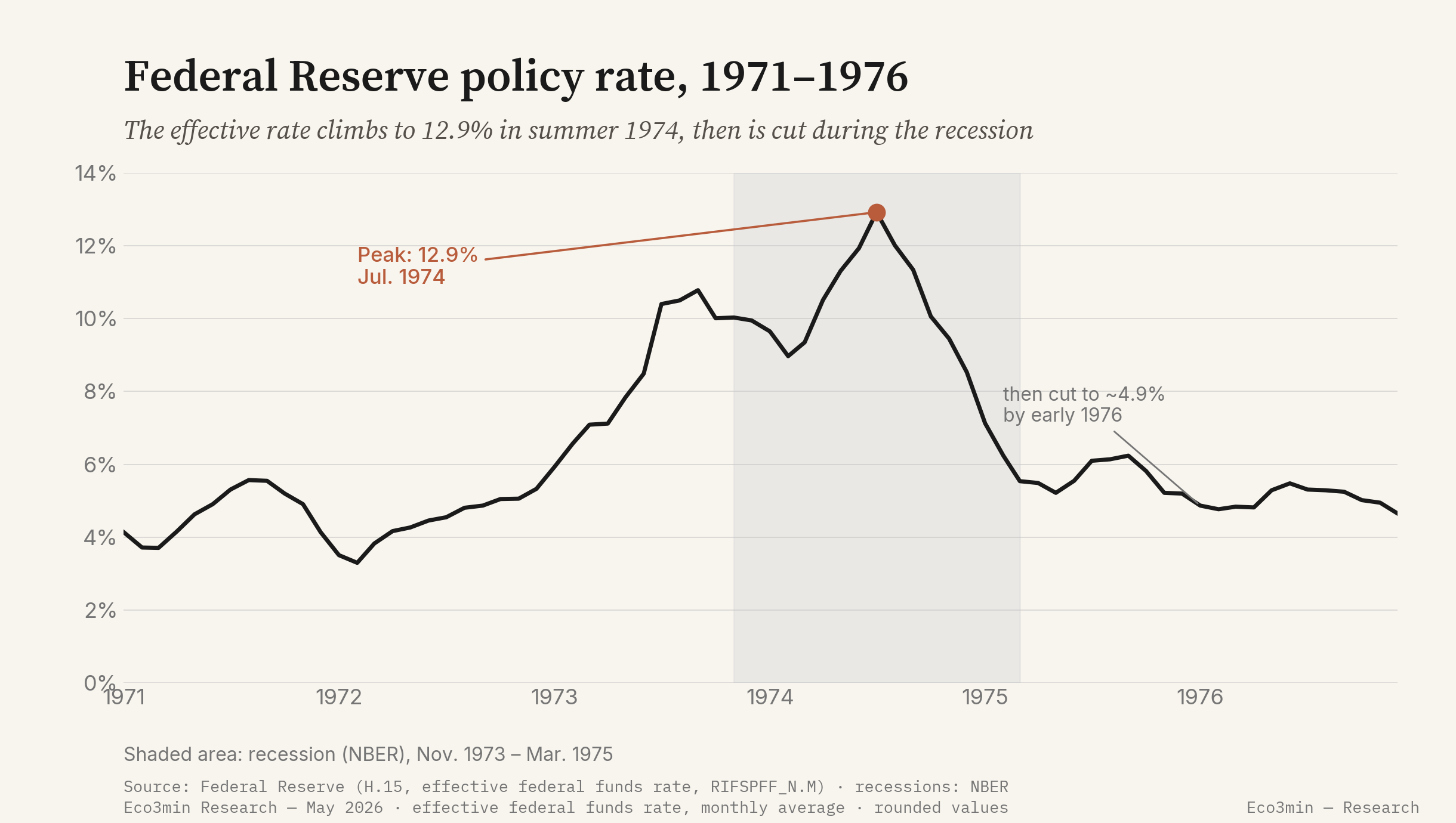

- July 1974 — The effective federal funds rate peaks at 12.9% (Federal Reserve, H.15) before being cut during the recession.

- November 1974 — Inflation reaches its high, 12.2% year-on-year (BLS). The recession continues to the trough dated March 1975; unemployment peaks at 9.0% in May 1975.

The indicators before the crisis

Reading this crisis through the indicators runs into a difference in kind with 2008. The 1973 trigger is largely exogenous and geopolitical: an embargo does not show up in a yield curve months ahead. What the series did signal, by contrast, was already-flammable ground. Inflation does not wait for the barrel to accelerate.

Already at 7.4% year-on-year in September 1973, before the embargo (BLS, seasonally adjusted consumer price index). The acceleration predates the oil shock: here it is the leading indicator of the destination regime.

consumer price index (CPI)The benchmark price quadruples after the October 1973 embargo; in real terms it rises about 3.5-fold between 1973 and 1974 (BP Statistical Review). It is the exogenous trigger, not the sole cause of inflation.

crude oil priceAt 5.9% in January 1973 (Federal Reserve, H.15), it rises with a lag behind inflation. Monetary policy chases inflation more than it anticipates it, a hallmark of the decade.

federal funds rateStill low at the onset of the crisis (4.8% in November 1973, BLS), it becomes the indicator that embodies the “stag” in stagflation: it rises even as prices rise, breaking the usual trade-off.

unemployment rateTwo structural conditions had prepared the ground. The end of Bretton Woods, in August 1971, lets the dollar float and raises the cost of imports. The gradual lifting of the price controls the Nixon administration had imposed in 1971 then releases increases that had been held down administratively. When the embargo arrives, it does not create a new regime: it amplifies an inflationary dynamic already under way.

The signature of stagflation lies in the joint path of two series. The trade-off described by the Phillips curve — less unemployment for more inflation, and vice versa — assumed the two variables move in opposite directions. In 1974-1975, they rise together. It is this simultaneity, not the level of inflation alone, that distinguishes the inflationary regime of 1973 from an ordinary overheating.

Inflation thus moves from 3.3% in January 1972 to 7.4% in September 1973, before the embargo carries it past 12% by the end of 1974 (BLS). Unemployment, starting from 4.8% at the November 1973 activity peak, reaches 9.0% in May 1975, a postwar high at that date.

The regime shift

The transmission follows an identifiable chain. The embargo reduces oil supply and quadruples its price; dearer energy spreads into production costs and retail prices; it weighs on activity at the same time, since an economy dependent on imported oil faces both higher prices and a supply contraction. This is the stagflation mechanism: a shock that pushes prices up and output down, whereas a demand overheating would push both up. A companion piece: Gold and oil read as a single macro instrument.

The core of the episode is that this supply shock adds to already-anchored inflation. Inflation expectations had settled in with the dollar’s depreciation and wage indexation; the embargo validates and amplifies them. Once anchored, these expectations make inflation persistent: it does not recede when the embargo is lifted in March 1974, but peaks later, in November 1974, and stays high for the rest of the decade.

Applied to 1973-1975, the Eco3min cyclical grid places the period in Stagflation (G− I+): growth contracts — the NBER dates a recession from November 1973 to March 1975, among the most severe of the postwar era — while inflation stays very high. That severe-recession-with-high-prices pairing shapes the comparison of which assets won in each episode. Three methodological points frame this verdict, in the spirit of the rule that separates the measured from the judged. First, the engine’s underlying-inflation axis, the Dallas Fed Trimmed Mean PCE, only begins in 1978: for 1973, the reading relies on headline inflation (CPI, PCE deflator), not on the live input. Second, the Eco3min classification was tested on the 2003-2026 window; 1973 predates that window by three decades. Third, this underlying-inflation axis is built to exclude energy: a transitory oil shock does not move it. What places 1973-1975 in I+ is therefore not the barrel itself — transitory by construction and excluded from the underlying measure — but the already-generalised inflation (wages, food, the dollar). Related discussion: how uranium differs from oil and gas.

The consequence is clear for how this page should be read. The layer-1 “Stagflation” verdict is here a retrospective application of the grid to period data, not a verdict produced in real time as for the 2008 crisis. The meta-regime destination, by contrast, is robust: whatever inflation measure is used, double-digit price increases place the period unambiguously in the inflationary column. It is this destination, more than the precise label of the cyclical state, that structures what follows.

The cyclical destination of this crisis is thus the inflationary meta-regime of the Eco3min Atlas (the inflationary regime). Unlike 2008, no dollar-shortage overlay is activated: the dollar depreciates in the early 1970s under the floating-rate regime, whereas the Dollar Shortage overlay assumes the opposite — an appreciating dollar and a drying-up of U.S.-dollar funding. This page describes the sequence of the shift; the Atlas page describes the destination state.

The central bank response

The monetary response of 1973-1975 contrasts with that of 2008 in its hesitation. Under Arthur Burns’s chairmanship, the Federal Reserve raises the effective federal funds rate from 5.9% in January 1973 (Federal Reserve, series H.15) to a peak of 12.9% in July 1974. Then, as the recession deepens, it cuts the rate rapidly, down to about 4.9% by early 1976. This profile of tightening followed by easing, while inflation remained high, has gone down in monetary history as “stop-go” policy.

This mechanism has a consequence for expectations. Cutting the policy rate while inflation is still in double digits amounts, in agents’ eyes, to validating the idea that the price rise will be tolerated. Inflation expectations de-anchor: firms and workers build durable inflation into prices and wage claims, which makes it effectively durable. It is precisely this loop that the Federal Reserve fails to break in the 1970s.

The contrast with the next sequence is instructive. From August 1979, under Paul Volcker’s chairmanship, the Federal Reserve runs a prolonged tightening that takes the policy rate well above 15%, breaks inflation, but at the cost of a deep recession in 1981-1982. The resolution of the stagflation that began in 1973 thus does not come from a one-off adjustment: it requires a change in monetary doctrine that plays out across the decade.

The 1973 shock and Paul Volcker’s tightening (1979-1982) are two moments of a single phenomenon: the entry into and the exit from the decade’s inflationary regime. This page documents the entry; the exit — the forced disinflation and the 1981-1982 recession that brings inflation back toward the disinflationary column — is the subject of a separate Crisis Hub page, the 1979 Volcker shock.

Assets and markets

Stagflation is an unfavourable environment for most financial assets at once, which sets it apart from disinflationary recessions where government bonds play their safe-haven role. U.S. equities go through one of the deepest bear markets of the postwar era: the S&P 500 falls about 48% between its January 1973 peak and its October 1974 trough. Bonds suffer in parallel, since inflation erodes their real return: the usual safe-haven status of government debt offers no protection in an inflationary regime.

Two assets behave differently. Oil, at the heart of the shock, sees its real price rise about 3.5-fold between 1973 and 1974 (BP Statistical Review). Gold, freed by the end of fixed convertibility, becomes a vessel for distrust of currencies and appreciates strongly over the decade. This behaviour differs from what was observed in 2008: in a disinflationary regime, the dollar and government bonds play the safe haven; in an inflationary regime, it is real assets.

The paths and levels described here are retrospective, for the purpose of historical analysis. They constitute neither a projection nor an investment recommendation, and past performance is no guarantee of future results.

One under-discussed financial signal completes the picture. In October 1974, Franklin National Bank fails, the largest U.S. bank failure to that date, amid foreign-exchange and funding losses. The stress does not carry the systemic signature of 2008, but it is a reminder that an inflationary regime with abrupt tightening also strains bank balance sheets.

What was different this time

The comparable of the same inflationary meta-regime is the second oil shock of 1979-1980, following the Iranian revolution. The Crisis Hub does not devote a dedicated page to it; its resolution is documented through the Volcker episode, which closes the decade’s inflationary cycle. The two shocks share the mechanism — a sharp rise in energy prices spreading into already-high inflation — but differ in the monetary response that follows.

Three factors set 1973 apart from an ordinary demand-driven inflation and from the 2008 crisis.

- A supply shock, not a demand excess. The embargo raises prices while reducing output. This combination breaks the Phillips-curve trade-off: prices and unemployment rise together, whereas a demand overheating would push them up in tandem but without a supply contraction.

- Inflation already anchored before the shock. The end of Bretton Woods and the lifting of price controls had launched the acceleration as early as 1972-1973. The embargo amplifies an existing regime rather than creating it; that is why inflation does not recede when the embargo is lifted.

- A hesitant monetary response. The Federal Reserve’s “stop-go” profile — tightening then easing while inflation stays high — lets expectations de-anchor. It is the opposite of Volcker’s prolonged tightening, and the opposite too of the massive, rapid easing of 2008, which was appropriate there because the regime was disinflationary.

What invalidated the “transitory shock” reading is measurable. Some observers in 1973-1974 took the price surge to be a passing episode, tied to oil alone and bound to fade once the embargo was lifted. The data proved otherwise: inflation peaks after the embargo is lifted, in November 1974, and stays high throughout the decade (BLS). The later re-examination by economists — notably Barsky and Kilian (2002) — emphasises, moreover, that monetary policy and expectations, as much as the barrel, explain the persistence of 1970s inflation.

One qualification is needed so as not to over-interpret the classification. The growth × inflation grid describes the regime, but does not, on its own, measure the structural dimension of the decade: durably negative real interest rates, which belong to a distinct long-run framework. Read as a simple cyclical state, the “Stagflation” label captures the conjuncture; read with the structural framework of financial repression in the background, it fits into a more durable distortion of the relationship between rates and inflation.

The 1973 oil shock did not create inflation: it turned an already-entrenched inflation into stagflation, with prices and unemployment rising together.

Where this crisis leads

The 1973 crisis leads to the inflationary meta-regime, in a structural environment of financial repression. The Atlas pages describe these states; this page documents the sequence of entry.

The meta-regime of the I+ column: high inflation, variable growth, financing conditions constrained in real terms. The destination is robust, even though the precise cyclical verdict of 1973 is a retrospective application of the grid.

Atlas — inflationary regimeThe decade’s long-run framework: durably negative real interest rates, which lighten debt at savers’ expense. This framework is not computed monthly by the engine; it shapes how the cyclical grid is interpreted.

Atlas — financial repressionSources

- U.S. Bureau of Labor Statistics — consumer price index (CPI-U, seasonally adjusted, CUSR0000SA0) and seasonally adjusted unemployment rate (LNS14000000).

- Federal Reserve — effective federal funds rate (H.15, series RIFSPFF_N.M); releases and monetary history of the Burns then Volcker chairmanships.

- National Bureau of Economic Research (NBER) — business-cycle dating (recession from November 1973 to March 1975).

- BP Statistical Review of World Energy — historical crude oil price (long real-terms series).

- Barsky, R. & Kilian, L. (2002), NBER Macroeconomics Annual — re-examination of the role of monetary policy and expectations in 1970s inflation.

- Eco3min data: consumer price index (CPI), unemployment rate, policy rate (federal funds), crude oil price.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →The 1929 Crash and the Great Depression

How, from 1929, the United States shifted into a durable disinflationary contraction: a reading of the Great Depression…

Japan’s Lost Decades (1989-2003)

The bursting of Japan's twin bubble in 1990-91 did not lead to an ordinary recession but to a…

The 1997 Asian Financial Crisis: a Dollar Shortage Outside the US Core

In 1997, the collapse of emerging-Asia currencies was a shortage of dollars outside the United States, leaving US…