WTI Supply Shocks and US Core Inflation, 1986–2026

Five episodes, five responses, and the one variable that predicts which is which

Five WTI supply shocks have hit the US economy since 1986. The two largest core CPI responses (+1.34 pp in 1990, +2.18 pp in 2022) both followed episodes where core inflation was already running above 4% before the shock. The three episodes with low pre-shock core inflation (2003, 2008, 2018) produced no lasting effect on core CPI. Oil amplifies the inflation that already exists — it does not create it. The European counterpart, working through gas rather than crude, is examined in gas transmission to euro-area consumer prices.

- Sample: 5 oil supply shocks (1990, 2003, 2008, 2018, 2022) identified by an explicit 3-criterion algorithm. Excludes the 2009-2010 and 2021 rebounds from crashed bases.

- Outcome variable: maximum core CPI YoY rise above its pre-shock 12-month baseline, measured over a 24-month post-WTI-peak window.

- Conditioning variable: pre-shock core CPI YoY at WTI peak minus 12 months. Threshold 3% separates “hot” from “cool” regime.

- Sample is small (n=5). The relationship described is a recurring pattern, not a statistical regression with claimed significance.

The five episodes

Oil shocks have a reputation for producing inflation. The 1973 OPEC embargo doubled crude prices over six months and contributed to a decade of US inflation above 5%. Our breakdown of the 1973 shock and its macro effects analyses its mechanics. The 1979 Iranian Revolution produced a second oil shock that pushed CPI above 13% by 1980 (the headline CPI YoY peak was 14.8% in March 1980). A comparable supply-driven episode in a soft commodity is documented in the role of swollen shoot in the deficit. The historical record from the regulated-price era is unambiguous: oil moves up, prices follow, and they stay up for years.

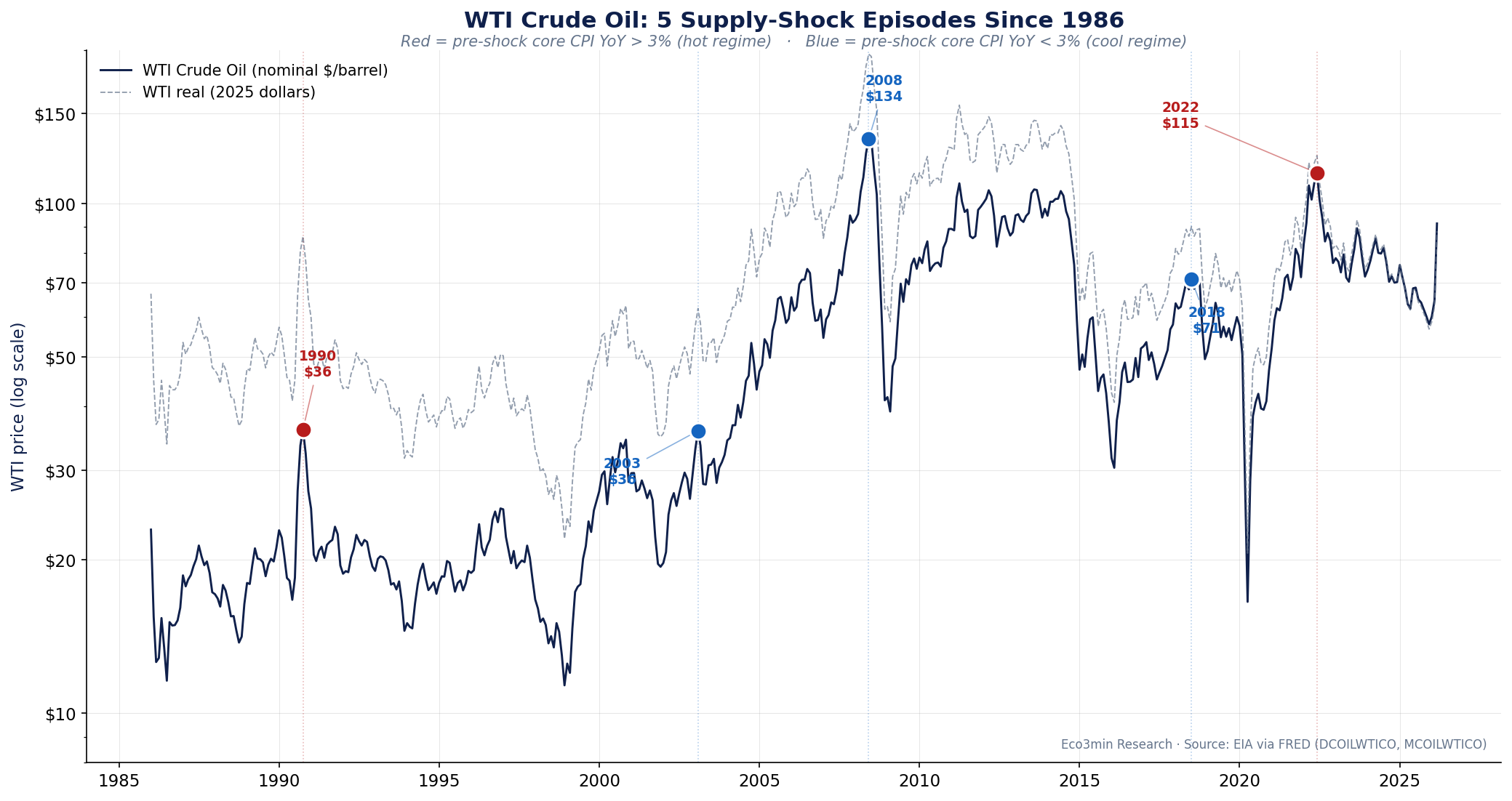

That record is the prior. Since 1986 — when WTI futures began trading freely on NYMEX and a comparable monthly price series became available — five episodes meet our supply-shock criteria (defined formally in the methodology). Their headline numbers:

| Episode | Peak month | WTI nominal | WTI real (2025 $) | WTI YoY at peak | Trigger |

|---|---|---|---|---|---|

| 1. Gulf War | Oct 1990 | $36.04 | $86.17 | +79.3% | Iraq’s invasion of Kuwait |

| 2. Iraq War run-up | Feb 2003 | $35.83 | $62.25 | +72.9% | US invasion build-up, Venezuela strike |

| 3. Commodity supercycle | Jun 2008 | $133.88 | $196.37 | +98.4% | Emerging-market demand, peak-oil narrative |

| 4. OPEC + Iran sanctions | Jul 2018 | $70.98 | $90.12 | +52.2% | OPEC+ supply discipline, US re-imposed sanctions |

| 5. Russia invasion | Jun 2022 | $114.84 | $124.19 | +60.9% | Russian invasion of Ukraine, SPR drawdowns |

The conventional reading of these episodes pairs each with a corresponding inflation surge: 1990 with the 1990-91 inflation pop, 2008 with the late-cycle CPI spike, 2022 with the post-pandemic peak. The implicit framework is that oil pushes prices, prices push core, and inflation accelerates. If oil is the cause, then the five episodes would produce five similar core CPI responses scaled by the magnitude of each shock.

They do not.

Hot regime, cool regime: the pattern

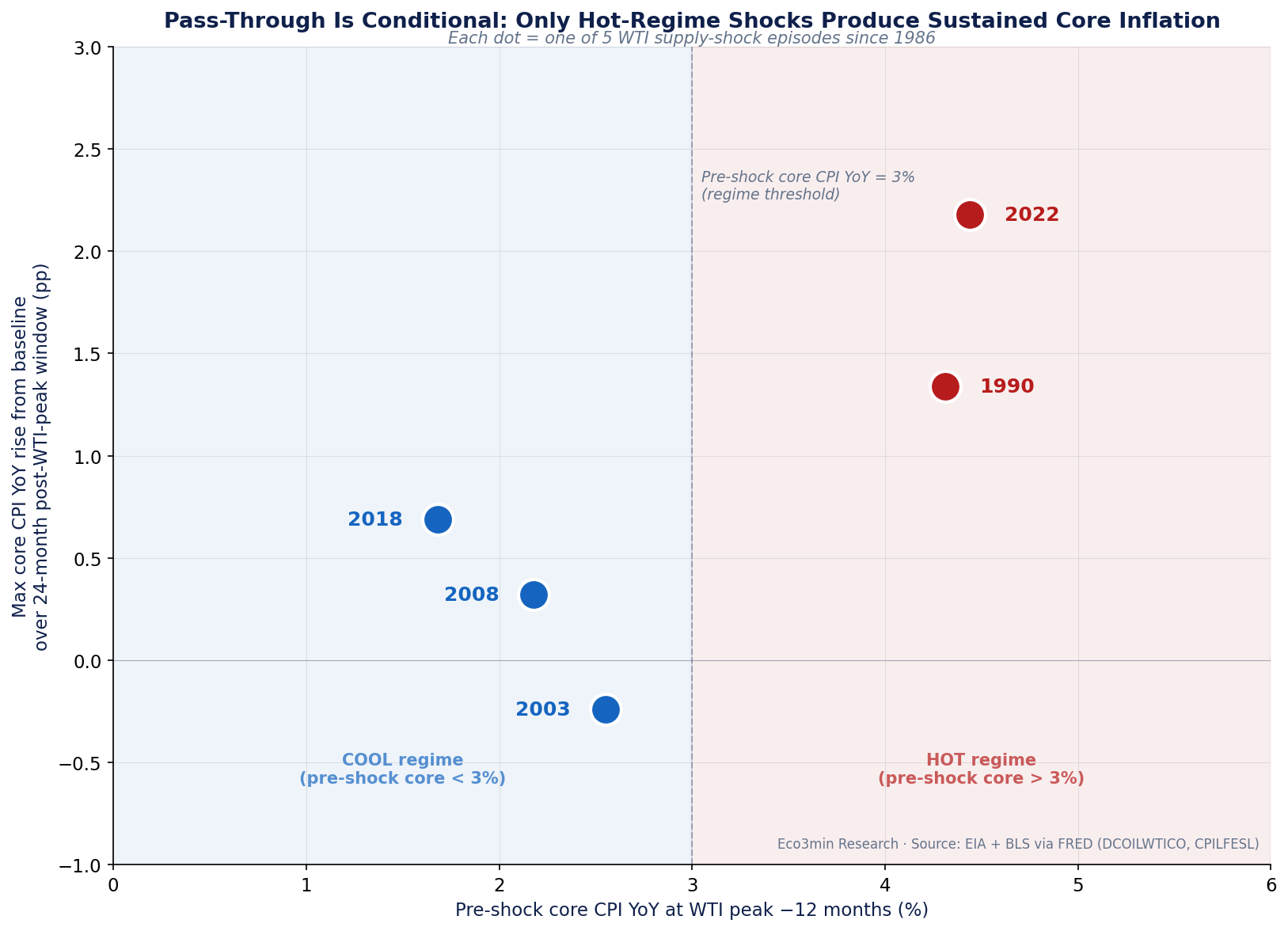

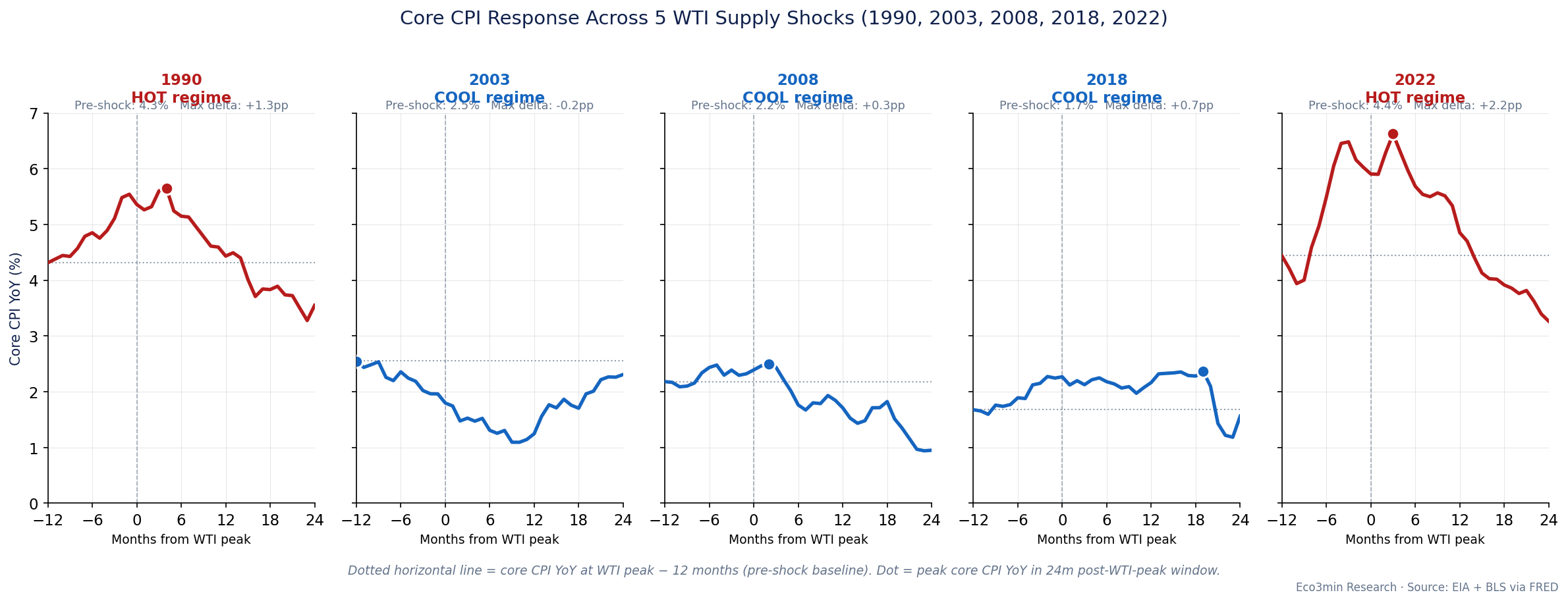

We measure the core CPI response to each shock by tracking core CPI YoY for 24 months following the WTI peak and comparing its maximum to its level 12 months before the peak (the “pre-shock baseline”). This isolates the rise in trend inflation associated with the shock, separately from the trend already in place.

| Episode | Pre-shock core CPI YoY | Max core CPI YoY in window | Max month | Max delta from baseline | Regime |

|---|---|---|---|---|---|

| 1990 Gulf War | 4.31% | 5.65% | Feb 1991 | +1.34 pp | HOT |

| 2003 Iraq War run-up | 2.55% | 2.31% | Feb 2005 | -0.24 pp | COOL |

| 2008 Commodity supercycle | 2.18% | 2.50% | Aug 2008 | +0.32 pp | COOL |

| 2018 OPEC + Iran sanctions | 1.68% | 2.37% | Feb 2020* | +0.69 pp* | COOL |

| 2022 Russia invasion | 4.44% | 6.62% | Sep 2022 | +2.18 pp | HOT |

*2018 episode: the +0.69 pp max occurs in Feb 2020, immediately before the COVID-19 onset. If the window is truncated at the +18-month mark (Jan 2020), the max delta is +0.68 pp, reached in Nov 2019; if truncated at +12 months (Jul 2019), the max is observed at the WTI peak month itself (Jul 2018) at 2.27%, giving a delta of +0.59 pp from baseline. The 2018 result is largely a pre-WTI-peak drift in core CPI rather than a post-peak rise — see limitations.

The pattern is striking. The two episodes with pre-shock core CPI above 4% (1990 and 2022) produced core CPI rises of +1.34 pp and +2.18 pp respectively — material, measurable, sustained for at least one quarter. The three episodes with pre-shock core CPI below 3% (2003, 2008, 2018) produced essentially no lasting impact: 2003 was net negative, 2008 peaked at +0.32 pp two months later before the financial crisis pulled it down, and 2018 is contaminated by COVID at the relevant horizon.

The pattern says: a WTI supply shock alone does not deliver a core CPI response. What predicts the response is the state of core CPI before the shock arrives. When core CPI is already running well above the Fed’s 2% target — which was the case in October 1989 (a year before the Gulf War peak) and in June 2021 (a year before the Russia peak) — the shock contributes another 1 to 2 percentage points of core inflation that persists for several quarters. When core CPI is already at or below target, the same kind of shock leaves no detectable mark. Related reading: Critical Minerals Geopolitics: The New Supply Chain and Market Risk Regime.

Methodology

Episode identification

A month t is classified as a WTI supply-shock peak if all three conditions hold:

- YoY threshold: WTIt / WTIt-12 – 1 > 50%.

- 36-month high: WTIt ≥ 98% × max(WTIt-35, …, WTIt). The 2% tolerance allows a peak to register the month before the strict maximum, which is more robust to single-month outliers.

- Local maximum: WTIt = max(WTIt-6, …, WTIt+6). This consolidates clustered peaks within a single episode into one observation.

The compound rule is stricter than the “+80% YoY” filter the casual reader might apply. It rejects two classes of spurious candidates that pure YoY thresholds would capture:

- Recovery bounces from crashed bases. April 2021 had +273% WTI YoY against the negative-price April 2020 base. The April 2021 price of $61.72 was nowhere near a 36-month high. It was a recovery, not a shock. The 36-month-high filter eliminates it. February 2010 (+95% YoY but $76 against a 2008 record of $134) is removed by the same rule.

- Trivial late-cycle bumps. Several years (1987, 1996-97, 2017) saw >30% YoY moves to absolute price levels that were unremarkable. The 50% YoY threshold filters these.

Pass-through measurement

For each peak month P, three variables are computed:

- Pre-shock baseline: core CPI YoY at P – 12 months. This is core inflation as the shock approaches, before any plausible spillover.

- Post-peak window: all months from P to P + 24 months.

- Max delta: max(core CPI YoY in window) – pre-shock baseline.

The max-delta measure was chosen over the “delta at +12 months” measure because the timing of the core CPI response varies across episodes. The 1990 Gulf War peaked in core CPI four months after the WTI peak; the 2022 Russia invasion peaked three months after; the 2018 OPEC episode appears to peak at +18 months, though that observation is contaminated by COVID. A related dataset: our US pump gasoline price record.

Regime classification

Episodes are split into “hot” (pre-shock core CPI YoY > 3%) and “cool” (≤ 3%). The 3% threshold is one percentage point above the Fed’s 2% target and is intended to flag periods where inflation is materially off-anchor, not periods where it is at-or-near target with normal noise. Sensitivity to the threshold is discussed in the limitations section.

Data sources and real-time availability

- WTI monthly: U.S. Energy Information Administration MCOILWTICO via FRED. Available monthly; revisions are minor.

- CPI (CPI-U, all items, seasonally adjusted): U.S. Bureau of Labor Statistics CPIAUCSL via FRED.

- Core CPI (CPI-U, all items less food and energy, seasonally adjusted): BLS CPILFESL via FRED.

- WTI prices in 2025 dollars use CPIAUCSL with January 2025 as the anchor (CPI = 318.961).

The 2025-10 CPI release was not published on its scheduled date; the underlying time series has a one-month gap at October 2025. The gap does not affect any of the five episode windows (the latest, 2022, ends in June 2024).

Why these five and not the conventional five

The conventional list of post-1986 oil shocks usually includes 1990, the late-1990s OPEC tightening peaking in 2000, the 2008 supercycle, the 2011 Arab Spring, and 2022. Our algorithm selects 1990, 2003, 2008, 2018, and 2022. Three of the five overlap with the conventional list; two do not. That late-1990s sequence played out against a collapsing Asian demand backdrop, documented in the 1997 Asian financial crisis, a dollar shortage outside the US core. The differences:

- 2000 OPEC episode. The September 2000 WTI peak of $33.88 was a 42% YoY rise against September 1999. It does not meet the 50% threshold. The OPEC tightening had been priced in gradually over 18 months from the 1998 trough, so the 12-month YoY metric understates the cumulative move. A sensitivity analysis with a 40% YoY threshold or a 24-month return would include this episode.

- 2011 Arab Spring. The April 2011 peak of $109.53 was a 30% YoY rise against April 2010. It does not meet the 50% threshold. More importantly, the $109.53 level was not a 36-month high — June 2008 still held the record at $133.88. The 2011 peak was a partial recovery within an already-elevated price regime, not a fresh shock.

- 2003 Iraq War run-up. The February 2003 peak of $35.83 was a 73% YoY rise and was a 36-month high — both criteria are satisfied. This is a real shock that the conventional narrative often folds into the longer 2003-2008 supercycle.

- 2018 OPEC + Iran sanctions. The July 2018 peak of $70.98 was a 52% YoY rise and a 36-month high. Algorithmically this is a peak. It does not feature in the conventional list because the absolute price level ($71) is unremarkable in long-series context.

Both differences cut both ways. Including 2000 and 2011 instead of 2003 and 2018 would not change the core finding. The pre-shock core CPI YoY readings for these episodes are 2.07% (September 1999, 12 months before the September 2000 peak) and 0.97% (April 2010, 12 months before the April 2011 peak) — both cool regime. Neither episode produced a sustained core CPI response. The hot/cool split would simply be 1990 and 2022 versus 2000, 2008, 2011, leaving the pattern intact. The 2011 window also overlapped Europe’s own funding squeeze, retraced in the eurozone crisis as a shift into dollar shortage.

Counter-arguments and limitations

n = 5 is small

This is the most important caveat. With five observations and one regime split, the strict statistical content of the comparison is limited. We report a recurring pattern, not a regression coefficient with claimed standard errors. The pattern is consistent with several economic mechanisms; it does not by itself prove any of them.

Energy intensity has declined

US primary energy consumption per real dollar of GDP has roughly halved since the early 1980s — from over 10 thousand BTU per chained 2012 dollar in 1983 to 5.05 thousand BTU/$ in 2020, the most recent year for which the EIA reports a complete figure (EIA Monthly Energy Review, Table 1.7). A given dollar move in oil therefore feeds through to the broader price level less mechanically than it did 40 years ago. This is a complementary explanation, not a competing one. It explains why oil shocks in general produce less pass-through than they used to; it does not explain why the 2022 oil shock produced more pass-through than 1990 (less energy-intensive economy, larger response). The pre-shock core CPI variable provides that explanation; the energy-intensity story does not. Further reading: What the gold-oil relationship reveals about the cycle.

The 2018 episode result is mostly pre-peak drift

The +0.69 pp max delta for 2018 falls in February 2020, the month before COVID-19 hit US economic data. If the window is truncated at January 2020 (+18 months from the July 2018 peak), the max delta is +0.68 pp, reached in November 2019. If truncated at +12 months (July 2019), the max is observed at the WTI peak month itself (July 2018, core CPI YoY 2.27%) — meaning that across the 12-month post-peak window, core CPI never exceeded its level at the WTI peak. The delta of +0.59 pp from baseline (1.68% at July 2017) therefore captures the pre-WTI-peak drift in core CPI between July 2017 and July 2018, not a post-peak response. Even at the longer +18m or +24m horizons, the delta is dominated by the pre-peak rise (the +0.59 pp at peak) with at most an additional +0.10 pp afterward. The 2018 episode is a cool-regime case with limited post-peak pass-through. On the same theme: the record of oil shocks and inflation.

Pre-shock core CPI is endogenous

Core CPI at the moment of the shock is itself the product of the macro state — fiscal policy, labor-market slack, the Fed’s recent posture, the path of energy prices over the preceding two years. To call it the “explanatory” variable is partly a labeling convention. A more cautious framing is: core CPI captures whatever macro conditions matter for pass-through better than any external proxy we tested. Whether it is the underlying expectations-anchoring story, the second-round wage-price dynamic, or the simple proximity-to-2%-target story is not identified from this data alone.

Kilian-decomposition concerns

Lutz Kilian’s 2009 work decomposes oil shocks into supply, aggregate demand, and oil-specific demand components. The 2008 episode is a textbook case where demand from emerging-market growth and financial flows drove a large share of the price move. By Kilian’s logic, that episode is not expected to produce strong core CPI pass-through, because rising oil from rising demand reflects exactly the conditions that do produce inflation through other channels — the core CPI rise from those other channels is what the pre-shock baseline already captures. Our framework does not contradict Kilian; it sits orthogonally to it, asking a different question about the state of the system rather than the type of the shock.

What to watch in 2026

WTI rose from $64.51 in February 2026 to $91.38 in March 2026 — a 42% one-month gain. The 12-month YoY at March 2026 is +27.8%, well below the 50% threshold our algorithm uses to flag a shock. If WTI sustains or extends from here, a sixth episode could register in mid-2026.

The pre-shock baseline that would be relevant for any 2026 shock is the March 2025 core CPI YoY reading: 2.81%. Headline CPI YoY was 2.38% in March 2025. Both are within or close to the Fed’s target band, below the 3% threshold that distinguished the hot-regime episodes.

If the March 2026 WTI move develops into a confirmed shock episode under the algorithm’s criteria, our framework would predict a response closer to 2018 (cool regime, small and short-lived) than to 2022 (hot regime, large and sustained). A response materially above +0.7 pp on core CPI within 24 months would constitute evidence against the pattern documented here.

This is a falsifiable prediction. Eco3min will revisit this question with updated data as the year develops.

Dataset and download

The full dataset is published as wti-core-inflation-shocks.csv. It contains 494 monthly observations from January 1985 to March 2026 with the following columns:

date— month start, YYYY-MM-01wti_nominal_usd— WTI Cushing spot, US dollars per barrel (MCOILWTICO)wti_real_2025_usd— WTI deflated to January 2025 dollars using CPIAUCSLwti_yoy_pct— 12-month percentage change in nominal WTIcpi_index— CPI-U all items SA (CPIAUCSL), 1982-84 = 100cpi_yoy_pct— headline CPI YoY, percentcore_cpi_index— CPI-U less food and energy SA (CPILFESL)core_cpi_yoy_pct— core CPI YoY, percentis_episode_peak— 1-5 if this row is an identified episode peak, 0 otherwisein_episode_window_id— 1-5 if this row falls within ±12 to +24 months of an episode peakmonths_from_episode_peak— signed offset in months from the nearest episode peak (NaN outside any window)episode_label— episode name stringepisode_pre_shock_core_yoy_pct— pre-shock baseline (core CPI YoY at peak -12m), constant within each episode windowepisode_regime— “hot” or “cool” based on pre-shock core CPI YoY threshold of 3%

The CSV, the production code, and the three charts in PNG, SVG, and PDF formats are released under CC BY 4.0. Citation: Eco3min Research (2026), “WTI Supply Shocks and US Core Inflation, 1986-2026”, https://eco3min.fr/en/wti-shocks-amplify-existing-inflation/.

Frequently asked questions

Why use core CPI rather than headline CPI as the outcome variable?

Headline CPI moves mechanically when oil moves, because energy products are a direct component of the index. A correlation between oil and headline CPI tells us nothing about pass-through to the broader price system; it just confirms that oil is in headline CPI. Core CPI strips food and energy, so any movement in core in response to an oil shock reflects second-round effects — propagation through transportation, petrochemicals, electricity, or expectations. That is the interesting question. Related analysis: The broader pass-through framework.

Why 1986 as the start date?

WTI spot prices were partially regulated under federal policy through 1981; NYMEX WTI futures began trading in 1983 but with thin liquidity in the early years; reliable free-market monthly WTI series begin in January 1986. Including the 1970s shocks would mix regulated and free-market price regimes, which the data does not support. The 1970s episodes are powerful historical evidence for oil-shock pass-through but cannot be apples-to-apples compared to the post-1986 sample.

Does the 3% pre-shock threshold drive the result?

The threshold separates 1990 and 2022 from the other three. At 2.5%, 2003 would also count as a hot regime — and it produced no pass-through. At 4%, only 1990 and 2022 still count as hot, and the same pattern holds. The result is not particularly sensitive to the threshold within the 2.5%-4.5% range because the actual pre-shock readings cluster well outside this band (1.7% to 2.6% for the cool episodes, 4.3% to 4.4% for the hot ones). There is a natural gap in the data.

What about the 1970s oil shocks?

The 1973 OPEC embargo and the 1979 Iranian Revolution were larger shocks in real terms than any of the post-1986 episodes. Eco3min measures how those energy shocks marked the price level in the mapping of all twelve U.S. inflation re-accelerations since 1948. They produced sustained core inflation for years. They also occurred during periods where US core inflation was already running well above the 3% threshold — BLS data show that core CPI exceeded 5% continuously from February 1974 through November 1982, consistent with the hot-regime pattern documented here. The 1970s episodes are evidence in favor of the pattern; they are excluded from the formal sample only because of the regulated-price data issue.

How does this compare to academic findings on oil and inflation?

Hooker (2002) finds that oil-price pass-through to US core inflation declined sharply after 1981, attributing the decline to better-anchored monetary policy. Blanchard and Galí (2007) reach a similar conclusion using a different methodology and time frame. Kilian (2009) decomposes oil shocks into supply, demand, and speculative components and finds that pass-through depends on which component dominates. Our finding sits comfortably within this literature: post-1986 pass-through is generally small, but it is not uniformly small — it depends on the state of core inflation when the shock arrives.

Is the 2026 spike already a confirmed shock?

No. As of the March 2026 data release, WTI YoY is +27.8%. Our algorithm requires +50%. The price is also not yet at a 36-month high — that record is held by June 2022 at $114.84. If WTI sustains above $90 through mid-2026 and breaks above $100, both conditions could be met. The pre-shock core CPI baseline that would apply is the March 2025 reading of 2.81%, which would place a 2026 shock unambiguously in the cool regime.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.