Monetary Expectations: The Invisible Channel of Central Bank Transmission

Monetary policy acts above all through the expectations of economic agents, often before any effective decision. This invisible channel can amplify, delay or even counteract the intended effects of central bank action.

Monetary policy does not transmit only through rates or liquidity. It acts above all through the expectations of economic agents, often before any effective decision, and at times in contradiction with the central bank’s initial intent.

TL;DR

In late 2025, policy rates held steady while SME loan volumes kept slowing near ≈5% year-on-year, showing expectations moved credit ahead of any rate decision.

- In late 2025, with policy rates steady, long-dated yields already priced diverging inflation scenarios, with spreads of roughly ≈40 to 60 basis points on certain maturities.

- SME loan volumes slowed around ≈5% year-on-year over the same period, where the expectation of a constraining environment weighed more than the level of rates itself.

- Expectations feed back onto policy: when markets price easing or prolonged tightening too early, they shift financial conditions before the central bank acts, sometimes forcing it to adjust its trajectory.

- Banks act on the self-fulfilling channel, loosening criteria marginally when cuts are expected and contracting credit pre-emptively when elevated rates look durable.

The mechanism is institutional and discreet. Even before a policy rate is moved, banks adjust their lending conditions, firms revise their financing plans, and markets re-price expected macroeconomic trajectories. Monetary transmission thus begins in minds and models, well before showing up in the data. Also relevant: The mapping of how the monetary regime conditions earnings.

This general framework is laid out in our reference analysis on how monetary policy operates and its impact on the real economy. The angle here is narrower: understanding why the expectations channel can reinforce, delay or even counteract the intended effects of a monetary decision.

When expectations take over from instruments

In advanced economies, most agents no longer wait for effective decisions to act. As soon as an inflection is perceived in central bank communication, behavior shifts. In late 2025, while policy rates remained stable, long-term yields were already pricing diverging trajectories depending on inflation scenarios, with spreads on the order of ≈40 to 60 basis points on certain maturities.

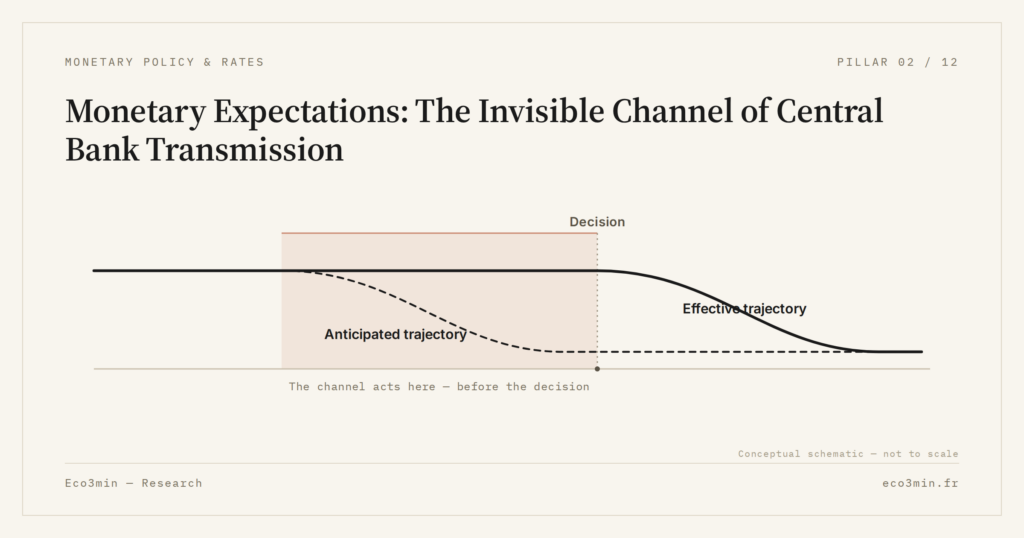

This gap illustrates a central point: monetary policy acts largely through perceived credibility and consistency. An isolated decision has little effect if it is not aligned with dominant expectations.

Dominant consensus and reading limits

This central role of expectations is largely explained by the hierarchy of monetary objectives, as analyzed in central banks’ choice to target inflation rather than growth, which conditions the credibility of trajectories perceived by markets and agents.

Part of the consensus assumes that expectations are merely a passive transmission channel, faithfully reflecting central bank decisions. In this reading, communication mainly serves to prepare markets for technical adjustments.

Our analysis diverges on this specific point. Expectations are not neutral: they feed back onto the decision itself. When markets price in easing too early or, conversely, prolonged tightening, they alter actual financial conditions before the central bank acts. This can force the institution to adjust its trajectory to avoid losing control of transmission.

- Treating central bank communication as a firm commitment, when it is mainly designed to steer expectations.

- Waiting for a formal decision to observe effects, when behavioral adjustments often precede action.

- Reading an isolated market move as a reliable signal, without considering the overall consistency of expectations.

An underestimated self-fulfilling effect

This mechanism is particularly visible in credit. If expectations of rate cuts become dominant, some banks marginally loosen their criteria, anticipating future margin improvement. Conversely, expectations of durably elevated rates lead to preemptive credit contraction, even without further hikes.

In late 2025, several aggregates thus showed nominal rate stabilization but a continued slowdown in SME loan volumes, on the order of ≈5% year-on-year. The expectation of a constraining monetary environment played a more decisive role than the level of rates itself.

Why this matters more now

The recent context reinforces the weight of expectations. After a prolonged tightening phase, perceived central bank room for maneuver is narrower. Each nuance of communication is over-interpreted, amplifying price movements and behavioral adjustments, sometimes beyond what fundamentals would justify.

What readers are really looking for

Behind interest in the role of expectations lies a simple implicit question: does monetary policy still act through its tools, or above all through what actors believe it will do? The real concern is not an abrupt rate change, but a growing gap between the anticipated trajectory and the one actually followed.

Common reading errors

First error: confusing communication with firm commitment. Verbal guidance does not necessarily imply immediate action, but already shapes behavior.

Second error: over-interpreting an isolated indicator. Expectations form from a set of signals, not a single number.

Third error: ignoring agent heterogeneity. Financial markets adjust their expectations faster than households or some firms, creating temporary lags in transmission.

Useful indicators for tracking the expectations channel

- Spreads between short and long rates, revealing anticipated trajectories.

- Credit conditions reported by banks, ahead of any formal decision.

- Volatility of rate-sensitive assets, an indicator of perceived credibility.

Alternative scenarios and limits

This framework rests on the assumption of intact central bank credibility. It could be challenged by an unexpected inflation shock or by financial instability forcing a rapid reaction. Conversely, deliberately more ambiguous communication could reduce the self-fulfilling effect of expectations, at the cost of slower transmission.

Reading perspective

The role of expectations in monetary transmission is less visible than that of rates, but often more powerful. It is not the central scenario put forward in public debate, but it is a key channel for understanding why some decisions appear effective before being applied, or ineffective once implemented.

To place this analysis in a broader perspective, the pillar page dedicated to monetary policy and rates situates this channel among other transmission mechanisms.

3 takeaways

- Expectations alter financial conditions before any effective decision.

- They can amplify or neutralize the initial intent of central banks.

- The gap between anticipated trajectory and actual trajectory is an underestimated risk.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…