Why Central Banks Target Inflation Rather Than Growth

Central banks target inflation rather than growth not by ideological bias but by operational constraint. Inflation is a controllable variable; growth depends on factors outside the monetary sphere.

Why central banks target inflation rather than growth: an institutional choice that structures monetary policy, well beyond cyclical debates.

TL;DR

Monetary instruments move prices directly but reach growth only indirectly, through productivity, demographics and fiscal policy the central bank cannot steer; that asymmetry makes inflation the operational target.

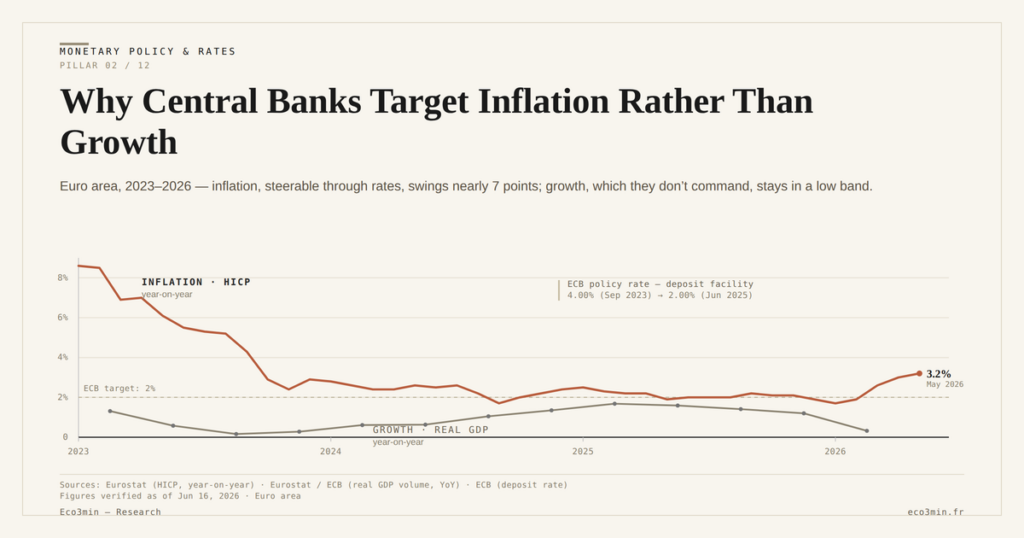

- In the euro area the deposit rate moved from -0.5% in 2021 to about 4% by late 2023, and headline inflation fell from above 10% at end-2022 toward 2.5-3% by late 2025, a trajectory the instruments can produce.

- The hierarchy follows from timing: inflation is anticipated and acted on ex ante, growth is observed ex post, so policy works on the variable it can still influence.

What prices reflect imperfectly is that central banks’ priority on inflation is not an ideological bias, but the outcome of an operational constraint. Since the monetary tightening that ran from 2022 to 2024, this hierarchy of objectives has resurfaced — visibly, sometimes contested, often misunderstood.

The starting point remains the same: monetary policy acts above all on financial conditions, not directly on output or employment. That framework explains why inflation has become the central target variable, at the expense of growth.

To understand how this choice fits into the broader transmission of monetary decisions to the real economy, the general framework is detailed in the reference analysis on monetary policy’s action on the real economy.

This institutional choice can only be understood within the broader framework of monetary policy and interest rates, which structures the hierarchy of objectives far beyond cyclical trade-offs between inflation and growth.

Part of the institutional consensus holds that price stability is the central bank’s best possible contribution to long-term growth. Dominant projections rest on the view that contained inflation reduces uncertainty, anchors expectations and supports investment.

What deserves refinement is the asymmetric nature of this reasoning: growth is a hoped-for outcome, inflation a controllable variable. That structural difference accounts for the hierarchy of objectives.

Inflation: a directly influenceable variable

This hierarchy of priorities becomes especially legible when examining monetary expectations in the transmission of monetary policy, which condition central bank credibility and explain why price stability remains the central variable. Related reading: the Eco3min dossier on the transmission of policy rates into margins.

Monetary policy tools act primarily on:

- the cost of credit, via policy rates;

- financial conditions, via liquidity and spreads;

- inflation expectations, via communication and credibility.

In the euro area, the deposit rate moved from -0.5% in 2021 to ≈4% by late 2023, before stabilizing in 2024–2025. That trajectory had a measurable impact on headline inflation, which fell from a peak above 10% at end-2022 to a range close to 2.5–3% by late 2025 according to harmonised aggregates.

Growth, by contrast, depends on factors the central bank does not directly control: productivity, demographics, fiscal policy, the geopolitical environment. Targeting it explicitly would expose the institution to objectives it cannot reach through its own instruments alone.

Why targeting growth would raise an operational problem

If a central bank announced an explicit growth target, two difficulties would arise immediately:

- no instrument allows fine-tuning of short-term GDP;

- the risk of conflict with price stability would become structural.

The monetary history of the 1970s illustrates the point: prolonged accommodative policies aimed at supporting activity fuelled persistent inflation, at the cost of a far harsher subsequent adjustment.

This historical reminder remains central to the current reference framework, even though the economic context is profoundly different.

What has quietly shifted since the return of inflation

Between 2015 and 2021, too-low inflation dominated debates. Since 2022, the situation has reversed. In 2025, the issue is no longer to revive activity at all costs, but to prevent a de-anchoring of price expectations.

This suggests that the priority on inflation has mechanically strengthened, even amid soft growth. The macro framework adopted by many participants assumes that inflation persistently above target would eventually damage growth more than a temporary monetary tightening.

What readers are really asking behind this question

The real question is not whether central banks ignore growth, but whether their focus on inflation risks worsening an already-underway slowdown. Beneath this question lies a simple concern: that monetary policy will remain restrictive for too long on principle, even as activity weakens.

The answer lies in timing: growth is observed ex post, inflation is anticipated ex ante. Monetary policy therefore acts on what can still be influenced.

An often-mentioned alternative scenario

Some current estimates favour the opposite assumption: a marked weakening of demand could pull inflation back down without prolonged high rates. In that case, the priority on prices would become less binding.

That scenario rests, however, on the assumption that recent supply shocks (energy, value chains, geopolitical strains) do not recur. It is precisely this uncertainty that keeps central banks focused on their nominal target.

Concrete indicators to watch

- 5-year inflation expectations, as measured by rates markets;

- the gap between core and headline inflation;

- nominal wage growth, notably in the euro area and the United States.

When these indicators converge toward levels compatible with the target, the monetary constraint can ease without undermining institutional credibility.

Common reading errors

Confusing indifference to growth with a hierarchy of objectives. Central banks do not neglect activity; they simply recognize the limits of their action.

Interpreting a cyclical slowdown as a policy error. Part of the adjustment is deliberate, in order to prevent more lasting imbalances.

Conclusion: a constrained choice more than a dogma

This is not the base-case scenario today, but a sharp weakening in growth could reshuffle the hierarchy of priorities. As long as inflation is perceived as the main macroeconomic risk, it will remain the compass of central banks.

Markets do not always fully price this asymmetry. Yet it is what structures contemporary monetary policy, far more than debates over the short-term level of growth.

- Key points: targeting inflation amounts to acting on the most controllable variable.

- In three sentences: growth depends on factors outside the monetary sphere; inflation conditions credibility; the hierarchy follows from available instruments.

- Three key takeaways: price stability, expectations, institutional constraints.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…