Money Illusion: How Inflation Reframes Three Common Rate Errors

An interest rate cannot be called 'high' or 'low' without the inflation context. The Eco3min framework on money illusion and the three reasoning biases — nominal reading, direction confusion, historical comparison — that recur in nearly every commentary on rates.

Calling an interest rate “high” or “low” without the inflation context has no economic meaning. Money illusion — reasoning in nominal euros rather than purchasing power — distorts the analysis of households and commentators alike.

TL;DR

A Livret A paying 2.4% against 2.4% euro-area inflation (Eurostat, January 2026) returns exactly zero in real terms, leaving the saver who feels remunerated merely treading water.

- Money illusion, reasoning in current euros rather than purchasing power, turns a 3% pay rise under 4% inflation into a real pay cut; Fisher first described it, Shafir, Diamond and Tversky revisited it in the 1990s.

- From mid-2024 to early 2025 the ECB cut 75 basis points while euro-area core inflation fell about 100bp, so the real rate edged up even as the nominal rate dropped, a divergence a nominal-only reading cannot see.

- Calling current rates 'historically high' ignores that 1980s real rates ran near 5% (15% nominal, 10% inflation), against about 0.5% real in the euro area today.

- Banque de France data put non-remunerated French current-account balances at about EUR 510 billion at end-2025; at 2.4% inflation that is roughly EUR 12 billion of purchasing power lost a year, invisible on the nominal screen.

Three reasoning biases recur in nearly every commentary on rates: nominal reading, direction confusion, and historical comparison in nominal terms. Each one survives because it is anchored in a number that looks self-explanatory.

Inflation reframes how interest rates should be read. The Eco3min framework on money illusion and the biases that distort economic analysis.

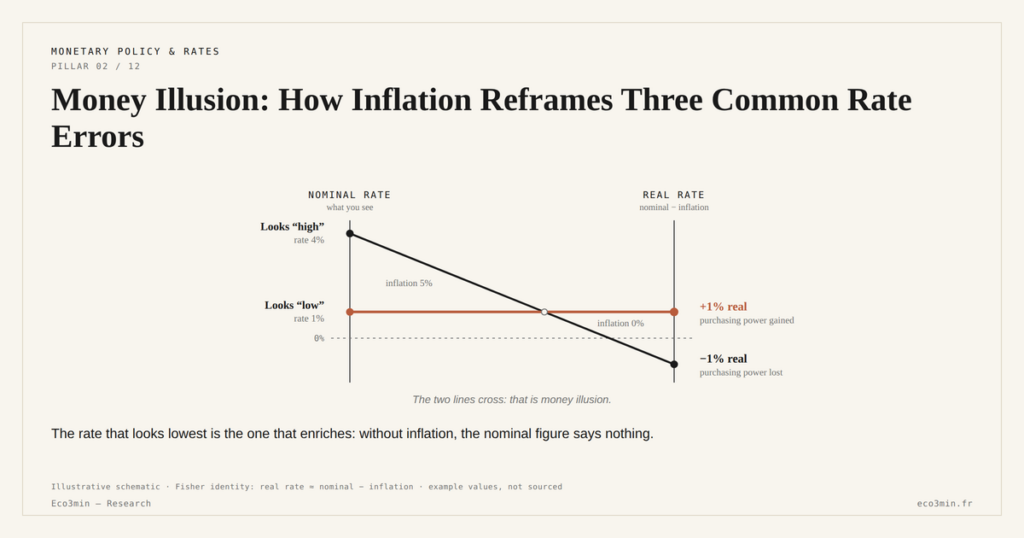

At 4% interest and 5% inflation, a saver loses 1% of purchasing power per year. At 1% interest and 0% inflation, the same saver gains 1%. The first rate looks “high”, the second “low” — yet only the second enriches. According to Eurostat (January 2026), euro area inflation stands at 2.4%. The French Livret A rate, set at 2.4%, delivers a real return of zero. The saver who feels remunerated is in fact treading water — a diagnosis the nominal figure alone cannot deliver. Further reading: our reference page on how monetary policy reaches corporate earnings.

The three biases that distort the reading

The first bias — money illusion — consists in reasoning in current euros rather than in purchasing power. A 3% nominal wage rise when inflation runs at 4% is a real pay cut. A loan repaid in inflation-eroded euros costs less than its nominal amount. The mechanism, described by Irving Fisher and revisited by Shafir, Diamond and Tversky in the 1990s, systematically distorts consumption, saving and investment decisions. Only the real-rate framework as a compass corrects the bias. It rests on the foundational nominal-versus-real distinction that any rigorous monetary reading takes as a starting point.

The second bias concerns the direction of the move. A cut in nominal rates is automatically read as easing. The same reading appears in the analysis of episodes where markets and recession signals diverge. Yet if inflation falls at the same time — and faster — the real rate can rise. That is exactly what happened in the euro area between mid-2024 and early 2025: the ECB cut by 75 basis points, while core inflation receded by ≈100 basis points over the same window (Eurostat). The real rate edged up despite the nominal easing. Only the real-rate framework picks up that kind of divergence; a purely nominal grid is structurally blind to it. That blindness is not a national quirk: it recurs wherever prices are quoted in current units, and that recurrence is the subject of money illusion as a cross-cultural regularity.

The third bias concerns historical comparison. Calling current rates “historically high” by reference to the nominal level alone ignores that real rates in the 1980s — with nominal rates at 15% and inflation at 10% — were around 5%. Current real rates, around 0.5% in the euro area, remain historically moderate. The “historically high” claim collapses the moment inflation re-enters the equation.

Reading a policy-rate cut as easing without checking whether inflation is falling faster is the most widespread reasoning error in monetary commentary. The relevant diagnosis never bears on the isolated nominal move — it bears on the gap between that move and the path of expected inflation. Nominal easing can mask real tightening.

What these biases cost in practice

For households, money illusion masks the erosion of purchasing power on cash balances during moderate inflation episodes. According to Banque de France data, French household balances on non-remunerated current accounts amounted to ≈€510 billion at end-2025. With inflation at 2.4%, the annual purchasing-power loss on those balances reaches ≈€12 billion — an invisible drag that the nominal-only reading prevents from being perceived as such. For context, see the catalogue of common money and market misconceptions.

For public decision-makers, the same biases distort the assessment of financing conditions. Budget projections built on nominal rates overstate debt-service costs when inflation runs high, and understate them when it is low. The real cost of debt service — adjusted for inflation — is the only measure relevant to fiscal sustainability over the medium term. Correcting these biases yields a more faithful reading of the real financial conditions economic agents actually face.

Last updated — 28 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…