Why an Interest Rate Only Matters When Adjusted for Inflation

An interest rate displayed at 5% can look high — but if inflation runs at 6%, savers lose purchasing power each year despite the apparent yield. This piece distinguishes nominal from real rates and shows how money illusion distorts the diagnosis of monetary conditions.

Money illusion — judging an interest rate without accounting for inflation — distorts the economic diagnosis of households, commentators, and at times policymakers.

TL;DR

France's Livret A pays 2.4% against euro-area inflation near 2.4%, a real return close to zero that captures why a nominal rate means little until adjusted for inflation.

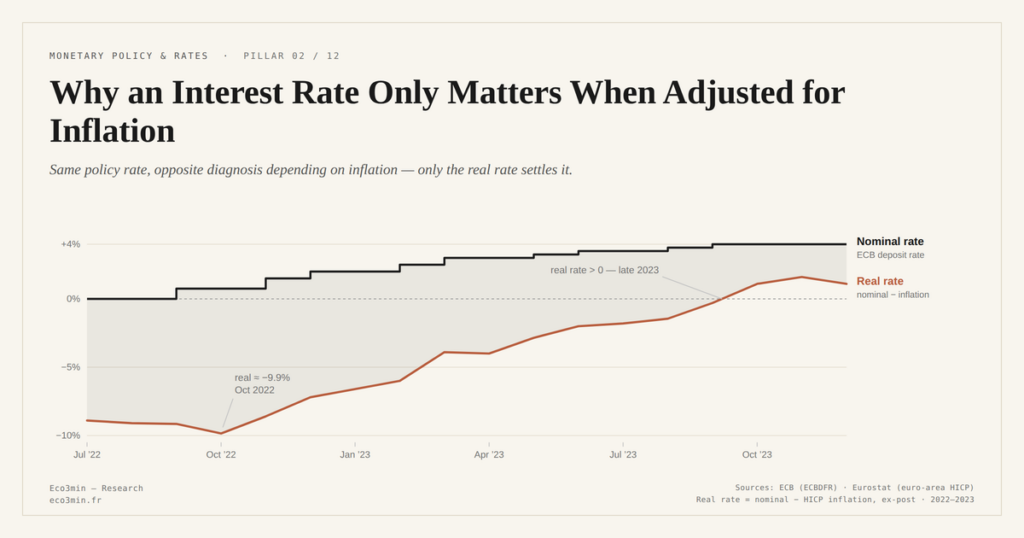

- The ECB raised its policy rates from 0% to 4% between July 2022 and September 2023, read as unprecedented tightening; with euro-area inflation above 8% at the summer 2022 peak (Eurostat), real rates stayed deeply negative through much of the cycle.

- The asymmetry runs in reverse: Japan's policy rate moved from −0.1% to 0.5% in early 2026, yet with inflation of 2.5–3.5% since 2023 (Statistics Bureau of Japan), real rates remain deeply negative despite an accommodative-looking nominal level.

- A 3.5% mortgage costs 0.5% in real terms under 3% inflation and 2.5% if inflation falls to 1% — the same nominal figure, opposite economic realities.

Distinguishing nominal from real rates is not an academic exercise: it is the prerequisite for any coherent reading of monetary conditions.

An interest rate only matters once adjusted for inflation. Understanding the nominal/real distinction and the money illusion that distorts economic analysis. Also relevant: where rate shifts land on corporate balance sheets.

An interest rate displayed at 5% may look high. But if inflation reaches 6%, the saver loses purchasing power every year despite the apparent yield. The wider pattern is charted in this dedicated note on inflation retirement purchasing power. The analysis is carried further in the comparative analysis of inversions with and without an equity correction. This gap between perception and reality has a name: money illusion. It leads households and commentators to draw mistaken conclusions about whether financial conditions are restrictive or accommodative. The variable that matters — the real rate — remains absent from most everyday reasoning.

Money illusion, a persistent bias

The nominal rate — the one displayed by the bank or the central bank — does not measure the real economic cost of money. Only the real rate, obtained by subtracting inflation from the nominal rate, reflects the actual gain or loss of purchasing power. According to Eurostat data (January 2026), euro-area inflation stands around 2.4%. The Livret A rate in France, fixed at 2.4% since February 2025 (Banque de France), thus offers a real return close to zero — a reality few savers spontaneously perceive. This mistaken perception illustrates the reasoning errors on rates and inflation that run through public debate.

Why this bias distorts the macro diagnosis

When the ECB raised its policy rates from 0% to 4% between July 2022 and September 2023, the consensus read this move as an unprecedented tightening. Yet with inflation above 8% at the summer 2022 peak (Eurostat), real rates remained deeply negative for much of the cycle. The real tightening was significantly more gradual than the nominal move suggested.

Mainstream forecasts anticipated a euro-area recession that did not materialize on the expected scale — partly because real financing conditions remained less restrictive than nominal rates suggested. This reading places the structuring role of real rates at the center of any reliable macroeconomic diagnosis.

The reverse asymmetry: when low rates are restrictive

The bias also runs in reverse. In Japan, the policy rate moved from −0.1% to 0.5% in early 2026. These nominal levels look accommodative. But with Japanese inflation between 2.5% and 3.5% since 2023 (Statistics Bureau of Japan), real rates remain deeply negative — a configuration that alters the analytical biases applied to interest rates in the Japanese case. By contrast, Switzerland with a policy rate at 0.5% and inflation near 1% at end-2025 (SNB) offers a slightly negative real rate, even though perception classifies its monetary stance as conservative. Directly related: how rate cycles reach corporate margins.

Calling a policy rate of 4% “restrictive” without knowing the inflation level is like assessing a speed without knowing the direction. A nominal rate of 4% with inflation at 5% is accommodative in real terms. The diagnosis only makes sense once the nominal rate is benchmarked against inflation to obtain the effective real rate.

What thinking in real rates changes

A mortgage at a nominal 3.5% in an environment of 3% inflation costs 0.5% in real terms. The same mortgage at 3.5% with inflation falling to 1% really weighs 2.5%. The same nominal numbers, opposite economic realities. For bond markets, it is the real rate that determines the relative attractiveness of asset classes. For sovereigns, it is the gap between the real rate and real growth that drives debt dynamics. Integrating this distinction leads to a more faithful understanding of the global liquidity environment in which economic agents operate.

What this distinction changes in macro reading

- An identical nominal rate can be accommodative or restrictive depending on the inflation regime — only the real rate settles the question.

- Money illusion led many to overstate the ECB tightening of 2022-2023 and to understate the persistence of still-binding real conditions in early 2026.

- Any analysis of financing conditions or asset valuations loses its relevance once it relies on raw nominal rates.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…