When Rates Become a Real Drag on Investment: The Threshold Effect

The drag of rates on investment is not linear. It depends on where the real cost of financing sits inside the distribution of expected project returns — and uncertainty about future rates amplifies the threshold sharply.

Not every rate level weighs on investment the same way. The drag depends on the gap between the real cost of financing and expected project returns — a non-linear threshold that uncertainty about future rates amplifies.

TL;DR

A project clears the investment test only when its expected real return beats the real cost of capital; around that cutoff, small moves in real rates trigger disproportionate effects.

- ECB SAFE data (Q3 2025) show ≈23% of eurozone SMEs now cite the rate level as an investment obstacle, up from ≈8% at end-2021 — a near-tripling while the cost of capital itself did not triple.

- Banque de France's January 2026 business survey shows the sorting: projects with expected real returns above 5% (modernization, energy transition) stay financed, while 2-3% capacity-expansion projects are broadly postponed.

- The eurozone Economic Policy Uncertainty index runs ≈30% above its 2015-2019 average in early 2026; that premium stacks onto the observable real rate, pushing the perceived cost of capital above the printed one.

This reasoning becomes central the moment real rates turn positive again and firms reopen long-horizon capex decisions that had been parked during the negative-rate decade.

The drag of rates on investment depends on expected returns, horizon and uncertainty. Mechanics of the threshold effect.

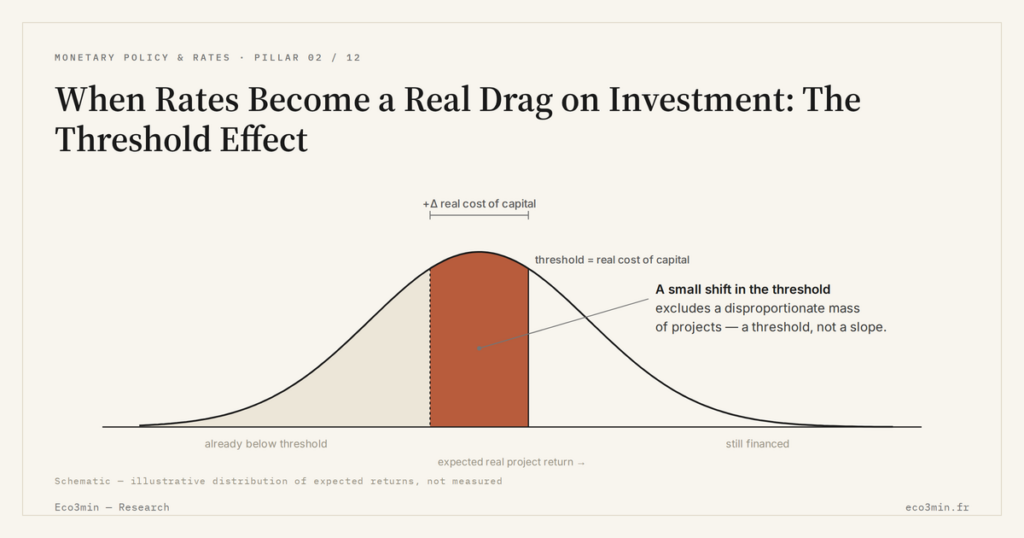

Inside investment committees, the test is binary: a project clears if its expected return exceeds the real cost of capital, otherwise it does not. The behavior of risk assets around shifts in that threshold is the subject of the Eco3min reading of inversion-rally cycles. The test itself is well known. What is less well understood is that it does not operate as a continuous function. According to the ECB Survey on the Access to Finance of Enterprises (SAFE, Q3 2025), ≈23% of eurozone SMEs cite the level of rates as an obstacle to investment, against ≈8% at the end of 2021 when real rates were negative. The reading roughly tripled over four years — but the underlying cost of capital did not. The asymmetry is the signature of a threshold, not a slope: small variations in real rates produce disproportionate effects on investment decisions, once one of those variations is enough to cross the profitability test for a large block of projects. The phenomenon sits squarely within the analytical role of the real cost of capital as a structuring variable.

The threshold mechanism: where the non-linearity comes from

When real rates move from -1% to 0%, the impact on investment is moderate — most projects remain viable, only the most marginal drop out. When they move from 0% to +2%, the effect accelerates: a growing share of projects falls below the profitability threshold. The non-linearity comes from the distribution of expected returns in the economy. That distribution is concentrated around the median, which means a small shift in the cutoff rate excludes a large number of projects sitting in the dense middle of the curve, not a constant fraction along its tail. A closer look: our study on the transmission of monetary policy to company results.

Banque de France data (business survey, January 2026) confirm the sorting. Investment intentions in French industry remain positive for modernization and energy transition projects, whose expected real returns exceed 5%. Capacity expansion projects with moderate expected returns (2-3% in real terms) are being broadly postponed. That selection process traces directly back to the structural link between real rates and the profitability filter on productive investment.

Uncertainty amplifies the threshold

The level of real rates alone does not explain the freeze. Uncertainty about future real rates does most of the amplification. A long-lived industrial project does not test its profitability against today’s real rate but against a path of real rates over the entire horizon. If that path is uncertain, the required risk premium rises, and the effective threshold sits higher than the observable rate suggests.

The Economic Policy Uncertainty (EPU) index for the eurozone is running ≈30% above its 2015-2019 average in early 2026. That uncertainty premium stacks on top of the observable real rate to form a “perceived” cost of capital that exceeds the printed one. The combination — positive real rates plus elevated uncertainty about their path — is what explains the freeze of many investment projects more than the rate level taken in isolation.

Reading the effect of rates on investment as a linear relationship — “rates rise by X, investment falls by Y” — ignores the threshold mechanism. The impact depends on where the real rate sits relative to the distribution of expected returns. Around the critical threshold, small variations in rates produce disproportionate effects, which is why surveys can show a tripling of “rate obstacle” responses without a tripling of the actual cost of capital.

What the current configuration implies

Mildly positive real rates plus elevated path uncertainty place eurozone productive investment in a threshold zone — neither a complete freeze nor a clean recovery. High-return projects still get financed, moderate-return capacity expansion stays parked. In the long run, that sorting is not necessarily a negative outcome: it concentrates capital on the most productive uses, which is exactly what the previous decade failed to do. In the short run, it slows gross fixed capital formation and weighs on potential growth — a dynamic that takes shape inside the broader financing and investment conditions of the current cycle.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…