Real Rates and Productive Investment: The Profitability Filter

Real rate levels determine which investment projects clear the viability threshold. The selection filter conditions both the volume and the quality of capital accumulation, with effects that compound over the long horizons typical of productive investment.

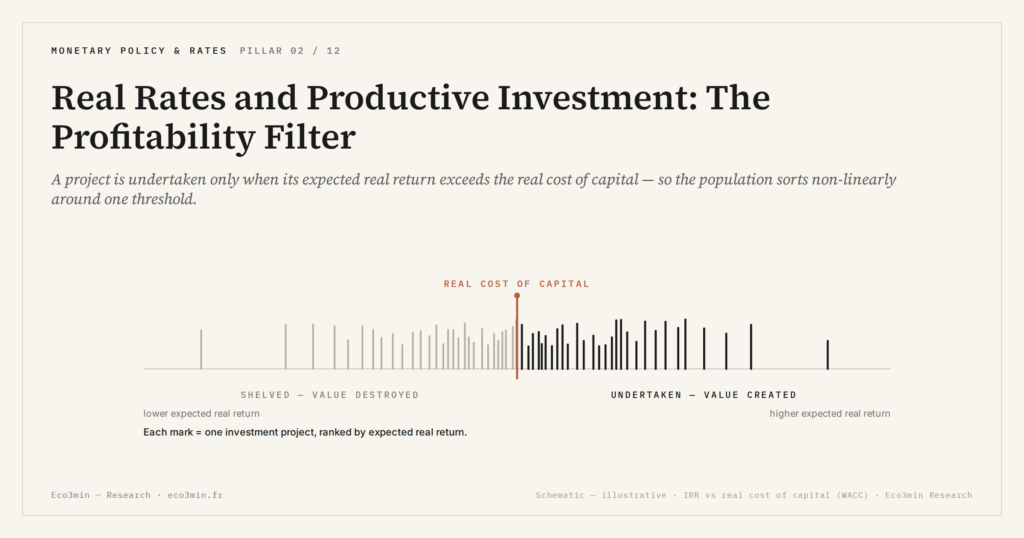

The real rate sets the threshold below which an investment project destroys value rather than creating it. This filter conditions both the volume and the quality of capital accumulation.

TL;DR

Negative real rates kept 'zombie' firms alive at roughly 12% of listed companies in 2020, and the return to positive real rates reinstates a profitability filter on new investment projects.

- A project clears only if its expected real return beats the real cost of capital: with the real cost of euro-area bank credit around 2% (ECB Survey on the Access to Finance of Enterprises, Q3 2025), any project returning less is mechanically excluded.

- Because investment is projected over 5, 10, even 20 years, expected future real rates matter more than today's level, so nominal cuts often fail to revive it: the Fed's Senior Loan Officer survey (Q4 2025) shows demand for productive-investment loans still below 2019 levels.

- The euro area's early-2026 shift sorts investment by quality, with high-productivity projects tied to the energy transition and digitalisation proceeding while marginal expansions are deferred (INSEE business surveys, January 2026).

The long horizon over which investment decisions are projected makes them especially sensitive to expected future real rates, not only to the level observed today.

Real rate levels determine which investment projects are viable. An analysis of the real profitability threshold and its macro consequences.

Inside the investment committees of major firms, the calculation has been the same for decades: a project is approved only if its internal rate of return exceeds the weighted average cost of capital — a metric that embeds, at its core, the level of real rates. This microeconomic filter, applied simultaneously by thousands of firms, produces a sizeable macroeconomic effect: the real-rate regime selects both the quality and the volume of capital accumulation across the economy. And this mechanism operates with lags. Projects launched under negative real-rate regimes only reveal their low productivity years later, once the cost of capital normalises. Related material: our breakdown of the time lags between rate cycles and profit margins.

The real profitability threshold as a selection filter

An industrial project with a 3% expected real return will be undertaken if the real cost of financing is 1%, but shelved if it reaches 4%. This basic calculation explains why changes in real rates have a non-linear impact on investment. According to the ECB Survey on the Access to Finance of Enterprises (Q3 2025), the real cost of bank credit to euro-area firms stands around 2% — a level that mechanically excludes any project whose expected return falls below that threshold.

This selection has an often-underestimated virtue. According to BIS work on prolonged low-rate episodes, periods of negative real rates coincide with a higher share of “zombie” firms — companies whose operating profits do not cover interest charges but which survive thanks to artificially cheap financing. The OECD estimated their share at ≈12% of listed firms in advanced economies in 2020. The return to positive real rates reinstates the analytical framework of real rates as a discipline mechanism in capital allocation.

Why a long horizon amplifies the effect

Productive investment decisions are projected over 5, 10, sometimes 20 years. That duration makes profitability calculations particularly sensitive to expected future real rates. A factory built over three years and operated for fifteen embeds, in its financial model, not today’s real rate but an anticipated trajectory across the entire horizon.

This sensitivity explains a recurring paradox: nominal rate cuts do not always revive investment. If firms expect real rates to remain elevated — because inflation falls faster than nominal rates — the headline easing signal is not enough to clear the tipping point for investment. The Fed’s Senior Loan Officer Opinion Survey (Q4 2025) confirms this reading: demand for productive-investment loans remains below 2019 levels, despite several cuts in policy rates.

Assuming that low rates automatically stimulate investment ignores the threshold mechanism. The breakdown is provided in our review of the inversion-rally paradox in equity indices. The effect depends on the gap between the real cost of financing and the expected return on projects. If uncertainty compresses return expectations, even moderate real rates can act as an effective brake. Investment volumes are not a linear function of rate levels.

What the current regime implies for the productive base

The transition from a negative to a mildly positive real-rate regime — the early-2026 configuration in the euro area — produces a gradual sorting effect. Maintenance and replacement investment carries on, but expansion projects with marginal profitability are deferred or shelved. According to INSEE business surveys (January 2026), French manufacturing investment intentions remain positive for projects tied to the energy transition and digitalisation, whose expected returns exceed the current real-rate threshold.

This reconfiguration shifts the sectoral composition of investment without aggregate figures reflecting it immediately. Capital accumulation refocuses on segments with high marginal productivity, at the expense of the extensive expansions that characterised the previous decade. Reading this dynamic correctly requires placing investment flows within the liquidity and financing context that conditions them.

Three observations on the real-rate-investment link

- The real rate acts as a selection filter whose effect is non-linear: beyond a threshold, investment deferrals accelerate sharply.

- The long horizon of productive investment decisions makes expected future real rates more decisive than the level observed today.

- The return to positive real rates in the euro area reinstates a discipline mechanism in capital allocation, at the cost of a temporary slowdown in invested volumes.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…