Why Reading Business Cycles Without Real Rates Produces Diagnostic Failures

The 2023 US recession that never arrived was forecast by every model anchored on the nominal policy rate. It was correctly priced by the small minority that worked in real rates. The variable that links credit, investment and asset valuations into a coherent cyclical signal is also the one most analytical frameworks leave out — and the omission shows up at every turning point.

Standard cycle frameworks track the policy rate, GDP and the labour market — and miss the variable that ties those three together. The real rate is what synchronises credit, investment and asset valuations into the patterns we recognise as a cycle.

TL;DR

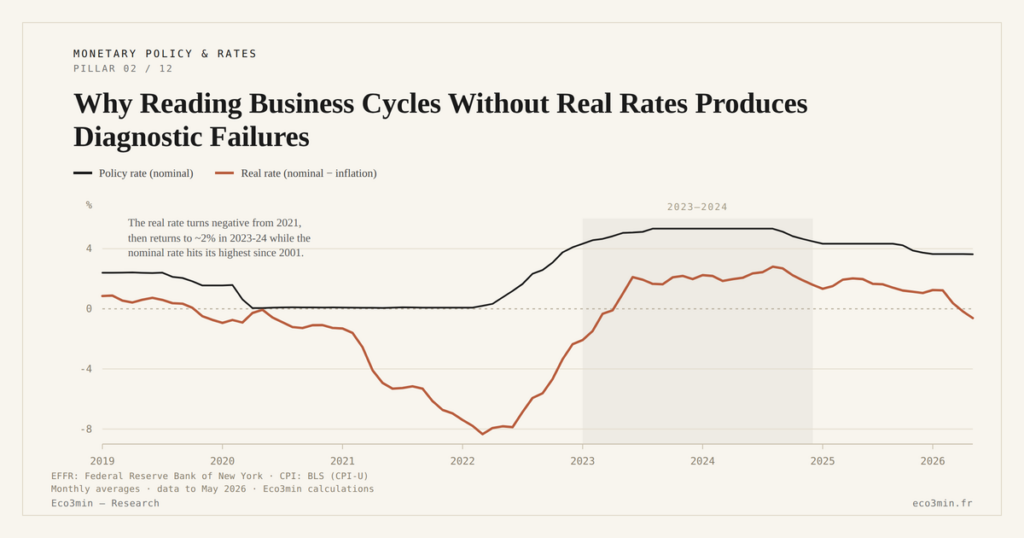

Most 2023 cyclical models forecast a US recession from a 5.25-5.50% policy rate. None arrived: with inflation near 3-4%, the real rate sat around 1.5-2.5%, far below recession-trigger levels.

- The real rate moves three channels at once: a low real rate cuts the real cost of leverage so credit expands, lets more projects clear the profitability threshold so capex rises, and compresses the discount rate on future cash flows so asset prices firm. The channels reinforce one another.

- The Eurozone 2014-2019 episode is the mirror image: despite zero or negative policy rates, growth averaged about 1.6% (Eurostat), because mildly negative real rates failed to offset fragmented banking, demographic drag and fiscal restraint.

An expansion that persists despite “high” nominal rates is not an anomaly. It is the signal that the nominal framework has stopped tracking the real one.

Ignoring real rates leads to a flawed reading of business cycles. Analysis of their cross-cutting role in credit, investment and asset markets. the distinction between credit and business cycles sets out the mechanism in detail.

Standard textbook cycles run the same sequence: the central bank cuts, credit picks up, investment recovers, growth accelerates; overheating triggers a hike, and the cycle turns. The schema works under one rarely stated condition — that the nominal move corresponds to a real move of comparable size. The link is developed in our mapping of equity-market upswings observed under an inverted yield curve. The condition is not always met. Without a real-rate reference, an expansion can persist while nominal rates look restrictive, and a recession can land while monetary policy looks accommodative. Both have happened in the last decade. Related work: our walkthrough of why margins react to monetary policy with a lag.

The real rate as the cycle’s synchroniser

The real rate operates on three cyclical channels simultaneously. When it is low, the real cost of leverage falls and credit expands. More investment projects clear the profitability threshold and capex rises. The discount rate on future cash flows compresses and asset prices firm. The three channels reinforce one another; the cycle gains momentum because its drivers are pulling in the same direction at the same time.

The reverse holds when real rates rise. Credit slows, investment retreats, valuations compress — together. The full analytical case built around real rates explains why turning points show up across the whole economy rather than in isolated sectors. Frameworks limited to the nominal policy rate cannot deliver that coherence: they capture the input, not the variable that synchronises the response.

Two episodes that put the omission on display

The 2023-2024 US expansion is the textbook counter-case. The Fed Funds rate at 5.25-5.50% — the highest level since 2001 — drove most cyclical models to forecast a recession. None materialised. The explanation runs through real rates. With CPI inflation between 3% and 4% (Bureau of Labor Statistics), the effective real rate sat between 1.5% and 2.5% — a moderate level by historical standards, insufficient to break credit and investment dynamics still benefiting from low fixed-rate debt locked in during the 2020-2021 window. Models calibrated on the nominal stance produced a confident, wrong call.

The Eurozone 2014-2019 episode is the symmetric trap. Despite zero or negative policy rates, growth averaged ≈1.6% (Eurostat). The negative nominal stance translated into mildly negative real rates that did not offset the structural constraints — fragmented banking, demographic drag, fiscal restraint — weighing on credit demand. In both cases, the real-rate reading reconciles the policy stance with the cyclical outcome. The mechanics behind that reconciliation appear in our analysis of real rates and financial cycles.

- The real rate is what aligns credit, investment and asset valuations into the synchronised pattern that defines a cycle — the nominal rate is only one of its inputs.

- The 2023 US recession forecasts failed because they anchored on a 5.25-5.50% policy rate without translating it into a real stance of 1.5-2.5%, well below historical recession-trigger levels.

- Any cyclical framework that does not distinguish nominal from real produces diagnostics that are systematically out of step with the economy in the regimes where inflation and nominal rates move together.

Reintegrating real rates into cycle analysis is not an academic refinement. It is the condition for avoiding recurring diagnostic errors at turning points. The trajectory of the cycles ahead will depend less on what central banks announce in nominal terms than on what economic agents perceive in real terms — itself a function of inflation, expectations and the credibility of the policy stance. That reading sits inside the broader question of liquidity conditions and their cyclical role as structural determinants of expansion and contraction.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…