Why Financial Cycles Track the Real Rate Regime

Financial cycles of credit expansion and contraction are conditioned by the real rate regime. The OECD credit-to-GDP ratio rose from ≈165% to ≈195% between 2010 and 2021 — a trajectory shaped by negative real rates, and now reversing as the regime normalises.

Financial cycles — alternating phases of credit expansion and abrupt contraction — do not unfold in a vacuum. The prevailing real rate regime structures both their amplitude and their asymmetry.

TL;DR

Across advanced economies the credit-to-GDP ratio climbed from about 165% in 2010 to nearly 195% by 2021, an expansion the real rate regime made possible and is now unwinding.

- The expansion ran on negative real cost: euro area private-sector credit grew ≈22% from 2015 to 2021 and residential prices rose ≈35% from 2015 to 2022 (ECB, Eurostat).

- The asymmetry is structural: per the IMF (October 2025), credit contractions in advanced economies last 2 to 3 years against 8 to 12 for expansions, because deleveraging is forced by debt-service pressure while leveraging up is voluntary.

- The current turn looks gradual: euro area private-credit growth slowed from ≈5% in 2022 to ≈1.5% by end-2025 (ECB) and property prices stabilized after 5 to 15% corrections, consistent with normalization rather than a banking accident.

Expansion phases run on cheap real leverage and last close to a decade. Contraction phases reprice that leverage at speed. The asymmetry is not behavioural — it is structural.

Financial cycles of credit expansion and contraction are conditioned by the real rate regime. Analysis of a central mechanism. On this point: the framework for reading financial repression regimes.

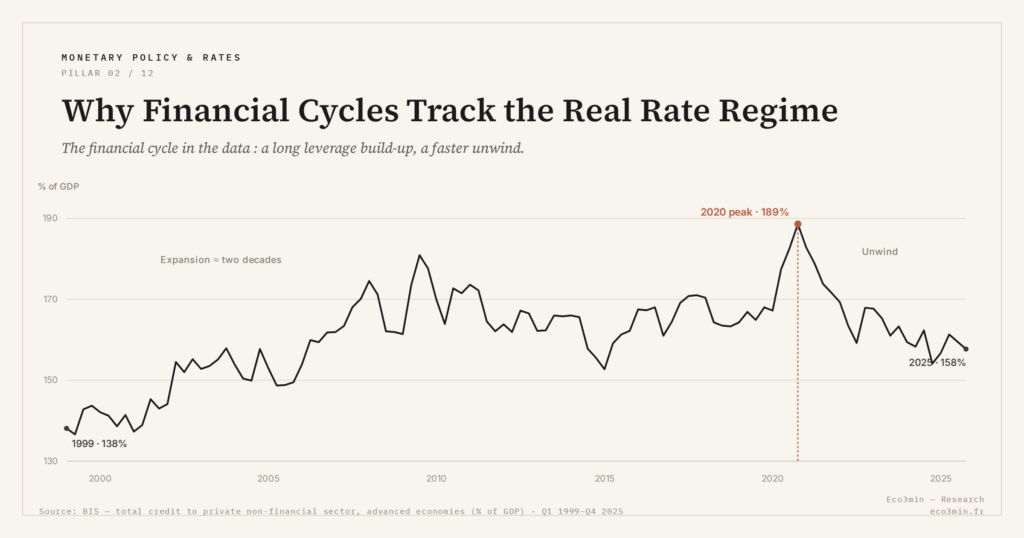

The credit-to-GDP ratio in advanced economies oscillates on a horizon — 15 to 20 years according to BIS research — that dwarfs the standard business cycle. According to Bank for International Settlements long-run series, the ratio rose from around 165% in Q1 2010 to nearly 195% by end-2021 across the OECD, before rolling over. The dynamic is not autonomous: it tracks the real rate regime. Low real rates compress the cost of leverage, risk-taking intensifies, asset prices drift from fundamentals. The reversal arrives when real rates turn restrictive — debt service becomes more expensive, collateral values weaken, the chain runs in reverse. For more detail: our study on the time lags between rate cycles and profit margins.

Expansion phase: when leverage is effectively free

In a negative real rate regime, borrowing creates value in real terms. The amount repaid weighs less in purchasing power than the amount borrowed. Standard prudential incentives invert. Borrowers raise leverage, lenders relax their criteria, competition among financial institutions compresses credit spreads — and the loop reinforces itself for as long as the rate regime holds. Related analysis: how a bond ETF reads under a given monetary regime.

Between 2015 and 2021, this mechanic fuelled the simultaneous expansion of mortgage credit, corporate credit, and high-yield bond markets across the euro area. The same dynamic is visible in the historical reading of curve-inversion and equity-strength sequences. According to ECB data, total credit to the non-financial private sector grew by ≈22% over that period. Euro area residential property prices rose by ≈35% between 2015 and 2022 (Eurostat) — a rise mostly financed at a real cost that stayed negative. The variable conditioning the entire cycle made this expansion possible: without negative real rates, leverage would not have reached these levels.

Reversal: when the real cost flips positive

Rising real rates trigger the inverse mechanism. Servicing existing debt becomes more expensive in real terms for floating-rate borrowers. New issuance prices through under tighter conditions. Asset prices, previously inflated by cheap leverage, contract — eroding collateral values and tightening credit conditions further down the chain.

This self-reinforcing loop explains why financial cycle reversals run faster than the expansions that preceded them. According to the IMF Global Financial Stability Report (October 2025), credit contraction phases in advanced economies last 2 to 3 years on average, against 8 to 12 years for expansion phases. The asymmetry is structural rather than behavioural: deleveraging is forced by debt service pressure, while leveraging up is voluntary and gradual.

Attributing financial cycles to banking excesses alone, or to investor “animal spirits”, obscures the determining role of the real rate regime. Risk-taking does not flourish in just any environment — it becomes individually rational only when the real cost of leverage is abnormally low. Correcting the rate regime corrects the cycle.

What the current cycle suggests

The shift to positive real rates since 2023 puts the euro area financial cycle in a transition phase. Private sector credit is decelerating — annual growth has fallen from ≈5% in 2022 to ≈1.5% by end-2025 according to the ECB. Residential property prices have stabilised in most markets after corrections of 5 to 15% in the most exposed segments. These adjustments are consistent with the normalisation of the real cost of leverage rather than with a banking accident.

The open question concerns the magnitude of the deleveraging still ahead. If real rates remain positive, the cycle contracts gradually. If a shock — a return of inflation pressures, a fiscal repricing — pushes real rates higher faster than expected, the adjustment can compress into a sharper window. This reading places real rates as a central variable of cyclical diagnosis, an approach that forces the question of whether one can read cycles without that variable at all. The full dynamic sits inside the broader framework of liquidity conditions and cycle formation that structures expansion and contraction phases.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…