Why a Single ECB Rate Produces Three Different Monetary Stances Across the Eurozone

The ECB sets one policy rate for twenty economies. In January 2026, that rate translates into a +1% real stance in Germany, ≈+0.5% in France and ≈-0.6% in Spain. The single-currency framework hides three distinct monetary regimes coexisting under one nominal headline — a heterogeneity that drives divergent national outcomes and that aggregate analysis cannot capture.

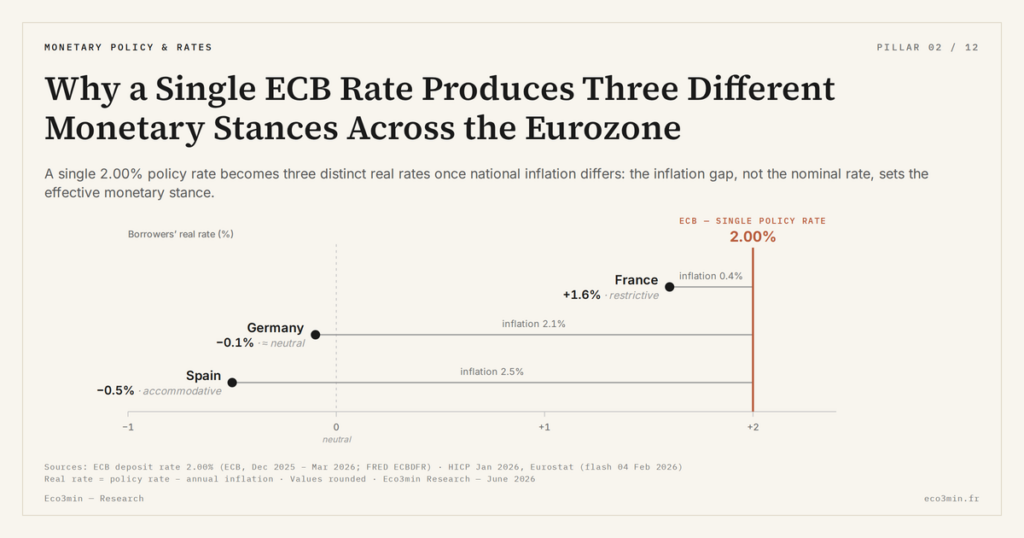

The ECB applies one policy rate to twenty economies whose inflation, debt profiles and credit structures diverge. The same nominal rate translates into restrictive, neutral and accommodative monetary stances depending on where you stand in the zone.

TL;DR

The ECB's single 2.75% deposit rate is restrictive in Germany, neutral in France and accommodative in Spain: inflation gaps and credit structure split one nominal rate into three real regimes.

- With headline CPI near 1.8% in Germany, 2.3% in France and 3.4% in Spain (Eurostat, January 2026), the real rate a borrower faces runs at roughly +0.95%, +0.45% and -0.65% respectively.

- Transmission speed diverges with mortgage structure: about 70% of Spanish mortgages are variable-rate (Banco de España) and reprice within months, against more than 95% fixed-rate in France (Banque de France), where existing borrowers feel almost no direct effect from ECB moves.

- Sovereign spreads feed the gap too: with the BTP-Bund spread near 130 basis points, the ECB Bank Lending Survey (Q4 2025) shows Italian SMEs facing tighter credit access than Dutch peers.

That observation is obvious to specialists and largely missing from mainstream coverage, which still reasons as though a single nominal rate produced uniform conditions.

A single rate level produces different effects across countries because of inflation gaps and financial structure differences. Comparative analysis.

The ECB’s deposit rate sits uniformly at 2.75% across the twenty Eurozone members at the start of 2026. Inflation does not. According to Eurostat (January 2026), headline CPI runs at ≈1.8% in Germany, ≈2.3% in France and ≈3.4% in Spain. The real rate perceived by a German borrower therefore stands at ≈+0.95%, against ≈+0.45% in France and ≈-0.65% in Spain. One policy rate, three distinct real monetary regimes. That divergence reframes the application of the real-rate analytical lens: the ECB’s monetary policy is single only on the nominal axis.

Financial structure as a transmission amplifier

Beyond inflation, the structure of national credit markets determines how quickly — and how violently — the policy rate reaches end borrowers. In Spain, ≈70% of mortgages are variable-rate according to the Banco de España. Every move in the policy rate feeds through to monthly payments within months. In France, more than 95% of mortgages are fixed-rate (Banque de France); existing borrowers feel no direct effect from ECB decisions, and even new originations route through a banking system where the term structure of funding insulates households. The same nominal cut delivers an immediate impulse in Spain and almost zero pass-through to the existing French stock.

The asymmetry extends to corporate credit. The ECB Bank Lending Survey (Q4 2025) shows Italian SMEs facing a sharper tightening in credit access than their Dutch counterparts — not because Italian banks are more conservative, but because the BTP-Bund spread at ≈130 basis points feeds the sovereign risk premium into private borrowing costs. These are the deeper drivers of cross-zone divergence — inflation differentials, sovereign spreads, credit structures — that keep the single-rate framework asymmetric in practice.

Reading Eurozone monetary policy as producing uniform effects. A 2.75% policy rate is restrictive in Germany (real rate ≈+1%), neutral in France (≈+0.5%) and accommodative in Spain (≈-0.6%). Analyses that fail to distinguish these three stances produce diagnostics that are wrong for at least two of the three economies, regardless of how precisely they describe the ECB’s announcement. Related material: The framework on how rate cycles filter into profits.

What the heterogeneity implies for analysis

The immediate consequence is that Eurozone aggregates bundle realities that are not comparable. Eco3min’s ECB macro data breaks down these national divergences series by series. Average GDP growth of ≈0.8% in Q3 2025 (Eurostat) combines German stagnation with Spanish expansion — and part of the gap traces back to the fact that real monetary conditions were accommodative in the south and restrictive in the north under the same policy rate. That structural paradox is the foundational challenge of single monetary policy under heterogeneous inflation, and it does not resolve itself through averaging.

For observers, investors and multinational businesses, the analytical implication is that the relevant input is the local real rate, not the headline policy rate. The broader picture is laid out in our analysis of equity-market persistence under an inverted yield curve. Capital allocation patterns, industrial location decisions and corporate financing strategies observed across the Eurozone since 2022 are more coherent with a country-specific real-rate map than with the single ECB headline. That country-specific reading sits within the broader question of local financial conditions, which vary considerably within a single monetary zone and make aggregate analysis insufficient on its own.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…