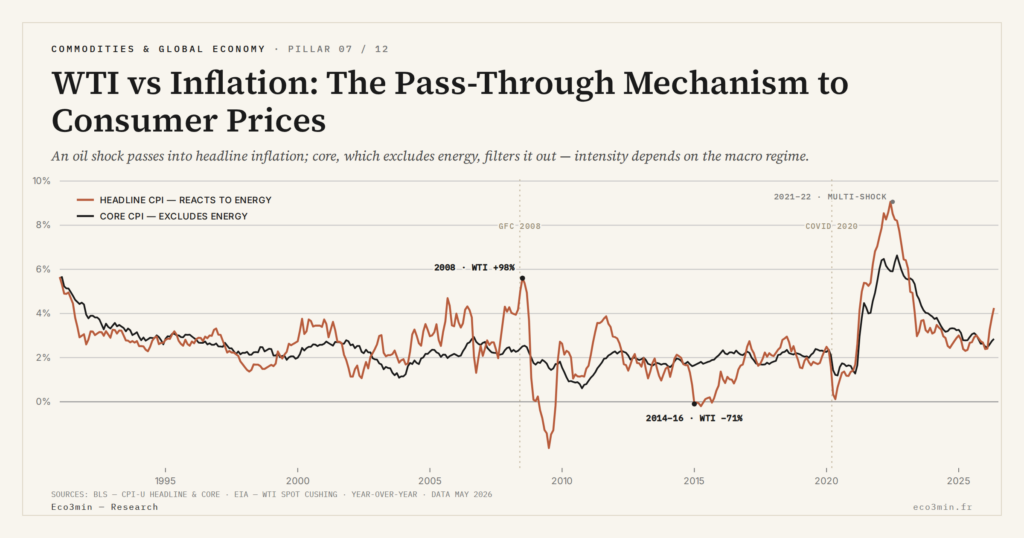

WTI vs Inflation: The Pass-Through Mechanism to Consumer Prices

When WTI rises 30%, how much CPI inflation results? Estimated pass-through transmits 0.2 to 0.4 of the shock to headline CPI over six months, weaker on core, with intensity varying by macro regime — pre-GFC, post-GFC, post-COVID.

TL;DR

Eco3min calculations put oil's pass-through to headline CPI at about 0.32 in 1990-2007 and 0.19 in 2010-2019: the crude channel has weakened markedly from one macro regime to the next.

- Three references (Hamilton 2009, Kilian 2014, BIS Working Paper 906 in 2020) bracket headline pass-through at 0.2-0.4 over six months, against just 0.05-0.10 on core, which excludes energy.

- The weakening tracks better-anchored expectations around the Fed's 2% target, formally adopted in 2012, and a roughly 35% drop in U.S. GDP energy intensity between 1980 and 2020 (EIA, BEA).

- The 2014-2016 slide shows the asymmetry: WTI fell from $105 to $26 (over 75%), yet core CPI held at 1.7-2.0% with no de-anchoring, an outcome pre-GFC models would have read as durable deflation.

- Post-2020 estimates stay wide: the 2022-2023 Ukraine shock landed with U.S. unemployment at 3.5%, its lowest in five decades, leaving oil's specific contribution to inflation an unsettled counterfactual.

This piece exposes direct WTI → CPI pass-through mechanics by regime. It does not address the special case of shocks amplifying already-installed inflation — Eco3min covers that angle in a separate piece. How the euro feeds imported inflation picks up this point on the FX side.

1. Pass-Through: Definition and Literature Estimates

Pass-through refers to the proportion of an oil price shock that ends up, after a lag, in consumer prices. The standard measure uses elasticity: if WTI rises 30% and headline CPI increases by 1.5 points over six months, the pass-through estimated over that period is 0.05 (1.5 / 30). Empirically, pass-through elasticity is not a constant: it depends on the macro regime, the composition of the consumption basket, and the nature of the shock itself (supply vs demand). Also relevant: natural gas pass-through to European inflation.

Three academic references converge on an order of magnitude for the U.S. economy. Hamilton (2009) estimates total six-month pass-through at 0.3-0.4 of the shock on headline CPI. Kilian (2014) refines this by distinguishing supply shocks (pass-through 0.2-0.3) from demand shocks (pass-through 0.3-0.5), because demand shocks typically accompany expansive economic activity that amplifies transmission. BIS Working Paper 906 (2020) confirms the order of magnitude across an expanded sample of developed countries: average pass-through 0.25-0.35 on headline CPI, but with notable dispersion depending on the energy composition of the basket.

For core CPI, which excludes energy and food, elasticity falls to 0.05-0.10 over six months. This difference is not anecdotal: headline CPI reacts mechanically to gasoline and heating oil prices, while core CPI captures only indirect effects through upstream production costs that transmit with longer lags (typically 12-24 months). When central banks anchor their monetary policy on core CPI (the Fed’s case with core PCE), it is precisely to avoid reacting to transitory crude moves that do not reflect underlying inflation. The price-formation chain linking copper to inflation extends this reading on a historical basis.

To understand the historical context of the shocks that fed these estimates, the cluster addresses the grid of seven major episodes in the historical shocks and pass-through. For the broader macro relationship between pass-through and oil-burden mechanics, the cluster details it in oil burden and macro transmission. The CPI-adjusted real WTI series is tracked daily on the CPI-adjusted WTI series on Eco3min.

2. Pre-GFC Regime (1990-2007): Strong Pass-Through

Over the 1990-2007 period, average pass-through elasticity per Eco3min calculations (FRED DCOILWTICO, CPIAUCSL for headline, CPILFESL for core) comes out at 0.32 over six months for headline CPI. This is a level consistent with Hamilton and Kilian estimates on similar samples. Average core pass-through is 0.08 over the same period — fairly stable and well-anchored. Directly related: the headline-minus-core commodity link.

Three structural characteristics explain this regime of relatively strong pass-through. First, U.S. economic energy intensity remains high in the early period: per EIA data, a dollar of U.S. GDP consumed about 0.75 energy units in 1990 (base 1 = 1980) versus 0.55 in 2010. The empirical detail is laid out in how physical barrels and tonnes shape the cycle. The more energy-intensive an economy, the more directly a change in crude prices transmits to production costs across the industrial fabric. For the broader picture: uranium against fossil energy.

Second, inflation expectations are in the process of anchoring but not yet perfectly stabilized. Post-Volcker, the Fed has established its anti-inflation credibility, but Michigan surveys and professional forecasters show that 5-10 year expectations remain around 2.5-3% in the early 1990s, versus 2.0-2.2% stabilized post-2000. This residual of unanchored expectations leaves room for energy shocks to translate into second-round propagation via wage negotiations and pricing margins.

Third, the energy share in the U.S. CPI basket went from 7.3% in 1990 to 8.4% in 2007 per BLS — significant weighting that translates mechanically into headline CPI when energy rises. The observed pass-through is therefore not just a deep inflationary transmission effect; it is also simply the arithmetic composition of the index.

The 2007-2008 episode is emblematic of this regime. From June 2007 to June 2008, WTI goes from $67 to $134 (FRED), or +100%. U.S. headline CPI goes from 2.7% year-over-year to 5.0% over the same period — a transmission of about 2.3 inflation points for a 100% WTI shock, consistent with pass-through around 0.02-0.03 per WTI percentage point over six months. Core CPI, meanwhile, stays below 2.5% throughout the period, illustrating the analytical separation between headline and core. Companion analysis: WTI 2024-2026: The $70-85 Stabilization Regime and Volatility Compression.

3. Post-GFC Regime (2010-2019): Weakened Pass-Through

Over the 2010-2019 period, average headline pass-through falls to 0.19 per Eco3min calculations — about a 40% reduction compared with the pre-GFC period. Core pass-through remains comparable at 0.07-0.09, suggesting that the weakening is concentrated on the direct component (pure energy) rather than on second-round effects.

Three candidate explanations structure the literature for this weakening. First, better anchoring of inflation expectations post-2000. The monetary regime having become fully credible and the explicit 2% target formally adopted by the Fed in 2012 have anchored 5-10 year expectations around 2.0-2.2%, a stable level despite energy shocks. This anchoring prevents price shocks from generating second-round wage-price spirals that historically amplified total pass-through.

Second, declining energy intensity. Per EIA and BEA data, U.S. GDP energy intensity (BTU per dollar of GDP) fell by about 35% between 1980 and 2020 thanks to energy productivity gains, partial relocation of heavy industry, and structural shift toward services and tech. A dollar of U.S. GDP in 2019 consumes less oil than a dollar of U.S. GDP in 1990 — so a change in crude prices transmits less directly to aggregate production costs. Related coverage: the gold-versus-oil yardstick applied to macro cycles.

Third, partial electric substitution. Growing electric vehicle penetration (1% of U.S. new car sales in 2017 per BloombergNEF), progressive electrification of residential heating, and the development of renewable energies in the electricity mix have reduced the share of oil in U.S. household energy baskets. WTI shocks therefore have a less direct impact on total household energy bills — attenuating the channel 3 purchasing power transfer addressed in the cluster.

The 2014-2016 episode negatively illustrates this regime. WTI goes from $105 in June 2014 to $26 in February 2016 — a fall of more than 75%. But U.S. core CPI remains stable around 1.7-2.0% throughout the period, and headline CPI briefly falls below 0% in early 2015 without triggering de-anchoring of expectations. Pre-GFC pass-through models would have predicted durable core deflation; it did not occur. It is this asymmetric robustness that characterizes the post-GFC regime.

4. Post-COVID Regime (2020-2026): Superposition Makes Estimation Unstable

The post-2020 period is harder to interpret because the COVID and then Ukraine shocks overlaid already-elevated non-oil inflation dynamics (supply chain disruptions, massive 2020-2021 fiscal expansion, labor market tensions post-Great Resignation). Pass-through regressions over this period become unstable and their confidence intervals widen considerably.

For the special case of WTI shocks that amplify already-installed inflation rather than create it, Eco3min has published a dedicated piece — WTI amplification of existing inflation — which isolates the 2021-2023 episodes where WTI contributed to extending already-elevated inflation. The present article limits itself to direct pass-through in “normal” inflationary regimes; the cyclical amplification case belongs to another analytical framework.

The methodological lesson of the post-2020 period is that pass-through is not only variable by regime — it is also conditional on the absence of other major shocks. In the presence of competing shocks (supply chain disruptions, fiscal shock, etc.), the statistical decomposition of observed inflation between “oil” and “non-oil” components becomes a difficult identification problem that simple pass-through models cannot resolve. Recent research uses structural models (DSGE, identified VARs) to disentangle contributions, with results sensitive to identification choices. For the underlying history, see our US retail diesel (ULSD) price record.

A second methodological caveat applies specifically to the 2022-2023 episode. The Ukraine invasion WTI shock coincided with a U.S. labor market running at maximum tightness (unemployment rate at 3.5%, the lowest in five decades) and with fiscal transfers from 2020-2021 still circulating through household balance sheets. Under such conditions, the marginal propensity to absorb a price shock without second-round effects may be lower than in benign regimes. Estimating the WTI-specific contribution to 2022 inflation requires identifying which fraction of headline CPI would have materialized without the Ukraine shock — a counterfactual exercise that the academic literature has not yet converged on. Eco3min therefore treats post-2020 pass-through estimates as range estimates with wide confidence intervals, not as point estimates comparable to the pre-GFC or post-GFC regimes.

For the macro reading 2026, the current WTI level around $70-85 mechanically implies a limited marginal pass-through (the cumulative dynamic since late 2023 is flat). The oil channel contributes neither to amplifying nor to attenuating current inflation — it is essentially neutral in the inflation transmission basket.

For the broader role of WTI as a macro barometer, the reference is the cluster’s WTI as inflation transmitter, which covers the three analytical functions (recession, inflation, geopolitics) of the U.S. barrel. Beyond the cluster, the pass-through reading fits within commodity regimes and macro cycles and within physical markets of energy resources which structures the Eco3min analysis of physical markets.

- WTI → headline CPI pass-through = 0.2 to 0.4 of the shock over 6 months (Hamilton 2009, Kilian 2014, BIS WP 906); core pass-through 0.05-0.10 — much weaker because core excludes energy

- Pre-GFC regime (1990-2007): strong pass-through (~0.32 headline) — expectations not yet perfectly anchored, high energy intensity, significant energy weighting in the basket

- Post-GFC regime (2010-2019): weakened pass-through (~0.19 headline) — Fed 2% target anchoring, declining energy intensity (-35% between 1980 and 2020), partial electric substitution

- Post-2020 regime: superposition makes statistical estimation unstable — for the specific case of shocks amplifying existing inflation, see separate dedicated piece

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Reading the refinery utilisation rate: the threshold, the season, the turnarounds

A refinery runs full near ninety percent, not a hundred: the last slice of nameplate capacity is a…

IMO 2020: the regulatory shock that rewrote product spreads

An environmental rule on marine sulfur can move a refining spread more than a swing in crude. IMO…

The 2022–2023 refining golden age: anatomy of an episode

In 2022, refined fuel prices climbed faster than crude. That gap, measured by the 3-2-1 crack spread, reached…