Why AI Drives Concentration Among Financial Players

AI reinforces financial concentration by favoring players able to invest massively in data and infrastructure, lifting fixed costs and entrenching dominant institutions.

AI reinforces financial concentration by favoring players able to invest massively in data and infrastructure — a dynamic that fits within the concentration and dispersion mechanisms examined in this dedicated analysis.

TL;DR

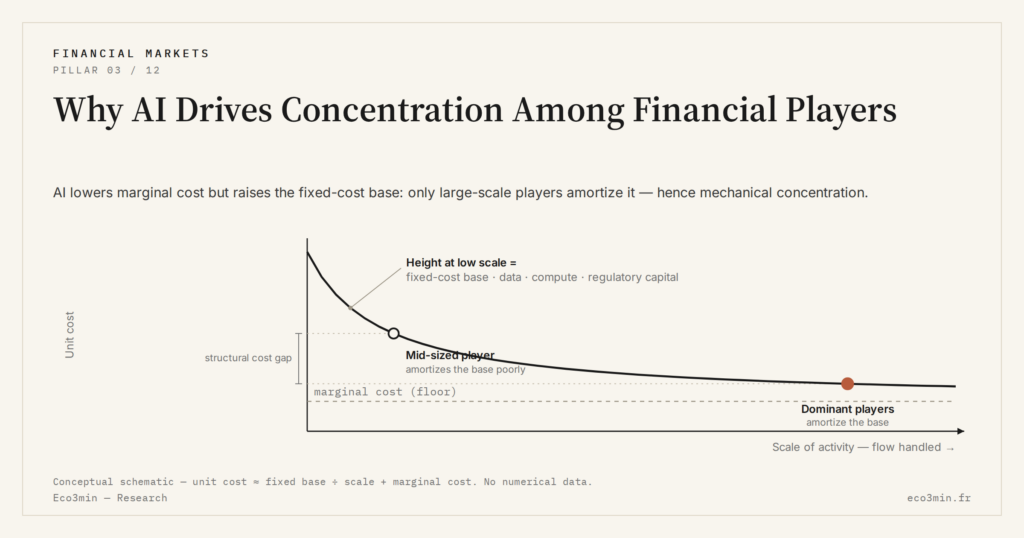

AI lowers marginal costs while sharply raising fixed ones, so firms able to amortise data, compliance and regulatory capital at scale widen their lead as the technology spreads.

- The advantage compounds across three reinforcing dimensions, proprietary data, computing power and regulatory capital: more order flow improves a player's models, and better models attract more flow.

- Between 2022 and 2025, financial-AI infrastructure spending concentrated on the few players able to mobilise several hundred million euros a year, a fixed-cost base mid-sized firms struggle to amortise.

AI requires substantial volumes of data, infrastructure and capital. These constraints mechanically favor players that already dominate. As the technology advances, capability gaps widen. A common misconception is to view AI as a force for democratization. Examining its competitive effects helps explain why it deepens financial concentration instead. For the full picture: how to map AI investment exposure.

A cumulative advantage that goes beyond technological performance

In automated finance, advantage is not limited to model quality. It rests on the joint accumulation of proprietary data, computing power and regulatory capital. These three dimensions reinforce one another. The more flow a player handles, the more its models improve; the better its models perform, the more flow it attracts. What that loop rewards is scale rather than insight, and it runs directly through the way artificial intelligence reshapes analysis and asset management.

Between 2022 and 2025, annual investments in financial AI infrastructure concentrated on a small number of players capable of mobilizing several hundred million euros per year. This dynamic creates a barrier to entry that mid-sized players, even innovative ones, struggle to overcome.

The implicit consensus: AI intensifies competition

Part of the consensus expects AI to lower access costs and intensify competition, allowing new entrants to rival established structures. The central scenario assumes that the diffusion of tools offsets size differentials.

The analysis diverges on a key mechanism: the nature of fixed costs. Marginal costs decline, but fixed costs rise sharply. Historical data, specialized teams, regulatory compliance and IT security form a base that only dominant players can amortize. Competition intensifies locally, but the overall market structure becomes more concentrated.

This asymmetry explains why efficiency gains captured by a few players can come with diffuse systemic costs, borne collectively without being directly internalized.

This reading fits within the broader framework developed in the analysis of structural risk linked to AI’s transformation of finance, where the technology reinforces dynamics already in place rather than reversing them.

The decisive role of data and compliance

Financial data usable at scale is rarely public. It comes from order flows, client behavior or internal databases accumulated over several cycles. To this is added rising compliance requirements, which increase the cost of deploying models.

Since the prudential tightening observed between 2023 and 2025, capital and risk-control requirements have reinforced the advantage of players able to absorb these constraints. AI then becomes a selection factor, not through its sophistication but through its compatibility with heavy structures.

Why this concentration is becoming more visible now

The current environment combines durably elevated rates and increased pressure on profitability. In this setting, only players able to spread technology investments at scale maintain their margins. Concentration effects become more apparent as the monetary cycle remains restrictive.

What readers really want to understand

The real question is not whether AI improves efficiency, but whether it durably alters the competitive equilibrium. Behind this question lies a simple concern: seeing the financial ecosystem organize around a limited number of dominant players that are harder to challenge.

Counter-arguments and tipping variables

Some argue that the standardization of tools and the rise of mutualized solutions will limit this concentration. That scenario rests on the assumption of homogeneous data access and a more flexible regulatory framework. A regulatory shift, broader data openness or a profitability shock could bend the current trajectory.

Indicators to watch for reading concentration

One relevant KPI is the share of volumes handled by the top five players in each automated segment. The trend in technology spending relative to revenue is also a key signal of players’ capacity to keep pace with the investment rhythm.

- AI lowers marginal costs but sharply raises fixed costs, favoring dominant players.

- Concentration stems less from algorithms than from access to data and regulatory capital.

- This is not the central scenario across all segments, but the risk is underestimated.

This dynamic does not foreshadow the disappearance of innovation, but rather a recomposition of the financial landscape. Placing these mechanisms within the broader frame of financial innovation helps explain why concentration progresses without making noise. The market has yet to settle this trajectory, which makes it easier to overlook.

Last updated — 30 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Euro Below Parity in 2022: What Parity Means

In September 2022, the euro fell below parity with the dollar, to around 0.95, a low not seen…

Eurozone Fragmentation: Sovereign Spreads and the Euro

The euro is issued by a monetary union without a complete fiscal union: nineteen sovereign debts coexist under…

The Euro’s Energy Import Bill: the Gas Shock and the Currency

In 2022, the surge in gas prices turned the euro area's historic current-account surplus into a deficit and…