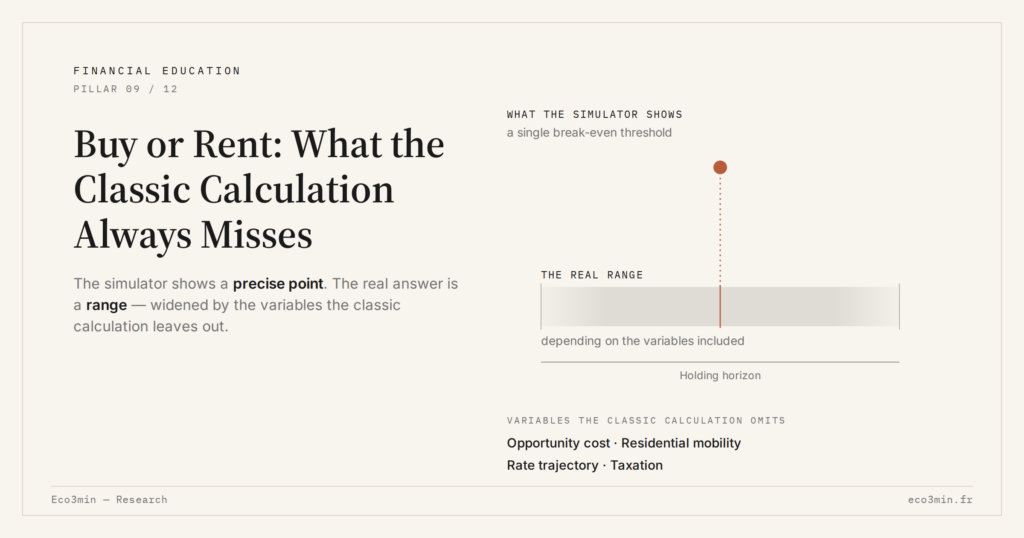

Buy or Rent: What the Classic Calculation Always Misses

The buy-or-rent decision is not simply about monthly payment versus rent. The classic calculation overlooks opportunity cost, mobility, taxation and rate dynamics — variables that can shift the patrimonial balance by tens of thousands of euros.

Comparing buying and renting looks simple: just put a mortgage payment up against a rent. In practice, that comparison ignores several decisive variables — the opportunity cost of capital, residential mobility and rate evolution — that can profoundly reshape the economic balance of the decision.

TL;DR

Buy-or-rent simulators compress the decision into one break-even number that leaves out opportunity cost, residential mobility and rate evolution, enough to shift the result by tens of thousands of euros.

- An 80,000€ down payment placed in a global equity ETF (about 8% gross annualised over 1988-2023, MSCI) would have grown to roughly 173,000€ in ten years before tax, the foregone return no standard simulator shows.

- The average French holding period is about eight years (FNAIM, 2025), far below the twenty simulators assume; each sale-and-rebuy round adds 10-15% of the transaction price in fees, undoing a break-even built on continuous ownership.

- Simulators freeze the rate: between mid-2022 and end-2024 mortgage rates moved from about 1.5% to over 4% (Observatoire Crédit Logement), driving a 22% drop in transaction volume and a 5-15% price decline (Notaires-INSEE, Q4 2024) that voids any break-even set on 2022 rates.

The classic buy-or-rent calculation omits opportunity cost, mobility and rate evolution. An incomplete framework biases the patrimonial arbitrage.

Buy-or-rent simulators produce a single number — a break-even point in years — that condenses the essence of the decision into one parameter. The problem is what that number leaves out: the opportunity cost of locked-up capital, residential and professional mobility, the future evolution of rates and taxation. By neglecting these variables, the classic calculation overstates the advantage of buying in some contexts and understates it in others — not least because it ignores the mechanisms of real estate price formation. The result is not wrong — it is incomplete. And a patrimonial decision based on an incomplete framework does not become more reliable simply because it relies on a spreadsheet. The evidence is brought together in how the price-to-rent ratio reads housing.

Opportunity cost: the variable nobody puts a number on

The down payment is the first blind spot of simulators. A household putting up 80,000 euros to buy a property gives up the return that capital would have produced elsewhere. Had that capital been placed in a diversified global equity ETF portfolio — historical annualised return of about 8% gross over 1988–2023 according to MSCI data — the sum would have grown to roughly 173,000 euros in ten years, before tax.

This calculation is not a recommendation. It illustrates that capital tied up in property carries an invisible cost — the foregone return. Simulators generally compare mortgage payment and rent, without factoring in what the down payment would have earned elsewhere. Yet over ten to twenty years, the difference can represent tens of thousands of euros, substantially altering the balance of the comparison.

On top of that come acquisition costs — between 7% and 8% of the purchase price for an existing home, according to the notary fee schedules in force in 2026. For a property worth 300,000 euros, those fees amount to about 22,000 euros that are immediately committed and non-recoverable. A renter who invests that same sum starts with an advantage rarely visible in standard comparators.

Mobility: a structural cost the calculation ignores

The break-even point calculated by simulators rests on an implicit assumption: that the owner stays in the home for the entire term of the loan, or at least until the equilibrium point. In practice, the average holding period for a property in France is roughly eight years, according to FNAIM data (2025). That figure includes moves linked to professional, family and personal change.

Each sale-and-rebuy cycle generates a round of fees — notary fees, agency commissions, early-repayment penalties, mandatory diagnostics — that add up to 10% to 15% of the transaction price in total. A household that moves three times in twenty years bears a cumulative additional cost considerable enough to invalidate a simulator calibrated on continuous holding.

For an early-career professional likely to be relocated within five to seven years, the mobility constraint weighs more heavily than a few tens of euros of difference between mortgage payment and rent. The classic calculation treats the home as a static asset in a life that is anything but.

- Using the break-even point displayed by a simulator without checking that the intended holding period matches the reality of one’s residential trajectory.

- Comparing mortgage payment and rent without integrating the opportunity cost of the down payment, transaction costs and differentiated taxation.

Rate evolution: a fixed parameter in a moving world

Simulators use a fixed mortgage rate — the one prevailing at the moment of the simulation — and project the monthly payments over twenty or twenty-five years. They do not model the impact of rate changes on the real estate market itself. Yet the correlation between mortgage rates and property prices is strong: when rates rise, real estate purchasing power falls and prices adjust downward, with a lag averaging twelve to eighteen months.

Between mid-2022 and end-2024, mortgage rates moved from around 1.5% to more than 4% according to Observatoire Crédit Logement data, triggering a 22% contraction in transaction volume and a 5% to 15% price decline depending on the market, according to Notaires-INSEE indices (Q4 2024). A buyer who used a simulator calibrated on early-2022 rates would have obtained a very favourable break-even point — rendered obsolete a few months later by the rate surge and price correction.

It is within this dynamic that the mechanism of long-term fixed-rate debt takes on its full meaning: the rate locked in at origination says nothing about the future rate environment, which nevertheless conditions the property’s value and resale capacity.

Taxation: a structural differential absent from simulators

The tax treatment of ownership and renting differs profoundly, and that difference is rarely integrated in mainstream simulators. The owner-occupier benefits from an exemption on capital gains when selling their primary residence, and from an untaxed implicit rent. In return, they bear the property tax — whose amount rose on average 4.7% in 2024 according to UNPI data — and homeowners’ association charges.

The renter who invests the capital they have not tied up faces taxation that varies by wrapper: 30% flat tax on a brokerage account, reduced taxation on a PEA after five years, an allowance on life insurance after eight years. The net tax balance — the one that compares the total tax cost of each option over twenty years — produces results very different from the simple mortgage-versus-rent calculation. And it depends on personal variables that standardised simulators cannot integrate.

What the calculation should include — and why it doesn’t

A complete buy-or-rent calculation would, at minimum, integrate: the opportunity cost of the down payment, transaction fees on purchase and sale, differentiated taxation, the probability of moving before the break-even point, and an assumption about the evolution of prices and rates over the holding horizon.

The reason simulators do not do this is simple: each variable added introduces uncertainty and makes the result less marketable. A clean break-even point of six years is a sales argument. A range of four to fourteen years depending on assumptions is much less so. The very format of the simulator — a single number displayed in large type — creates an illusion of precision that masks the scale of real uncertainty.

Before using such a tool, it is necessary first to distinguish the logics before comparing: the primary residence, savings and investment do not obey the same criteria, and reducing them to a comparative yield calculation necessarily produces a biased result.

A buy-or-rent simulator is not a decision tool — it is a starting point. The patrimonial decision requires integrating the variables the simulator excludes by construction.

This observation does not mean buying is less attractive than renting — nor the reverse. It means the comparison produces different results depending on the number of variables integrated, the horizon retained and the assumptions used. A calculation resting solely on the monthly payment and the rent ignores most of what determines the real patrimonial balance at ten or twenty years. These decisions commit household wealth over the long term and fit within the broader frame of financial choices that engage long-term wealth. Related coverage: our walkthrough of the simulation toolkit.

- The opportunity cost of the down payment — the foregone return on an alternative investment — can represent tens of thousands of euros over ten to twenty years and does not appear in any standard simulator.

- The average holding period in France is around eight years — well below the twenty years assumed by simulators, which invalidates their break-even point for many households.

- A complete calculation would integrate transaction costs, differentiated taxation, mobility probability and the evolution of credit conditions — not just monthly payment versus rent.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Series I and EE Savings Bonds: Locked Formulas in a Moving Rate World

US savings bonds lock a rate formula at the moment you buy them, for the life of the…

Where the Livret A’s Money Goes: The Caisse des Dépôts Circuit and Social-Housing Finance

The savings held on Livret A accounts do not sit idle. A regulation-set share is centralised at the…

France’s LEP vs the Livret A: A Means-Tested Higher Rate, Explained

France’s Livret d’épargne populaire is often described as "the Livret A, only better". The description misleads: the LEP…