Common Mistakes in Interest Rate Analysis

Confusing nominal with real, short with long, policy rate with credit cost: three analytical shortcuts that systematically distort the diagnosis of actual monetary conditions in economic commentary.

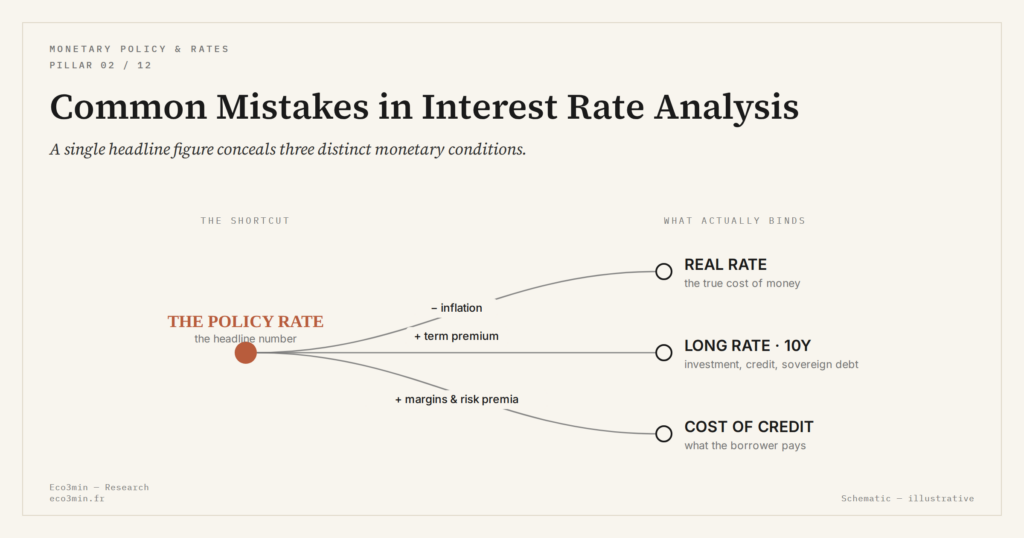

Confusing nominal and real rates is the most widespread mistake, yet it coexists with other analytical shortcuts that systematically distort economic diagnosis.

TL;DR

Three analytical shortcuts — reading nominal for real, short rates for long, the policy rate for credit cost — reinforce each other and systematically distort how monetary conditions are diagnosed.

- The same 2.75% policy rate means a ≈0.35% real rate against 2.4% inflation (Eurostat, January 2026) but 1.75% against 1% inflation — identical headline, opposite restrictiveness.

- The 10-year OAT yield sat near 3.2% in January 2026 (Banque de France), barely reflecting the four policy cuts since June 2024; long rates carry their own inflation and risk expectations.

- Despite those cuts, eurozone banks kept relatively strict lending standards (ECB Bank Lending Survey, Q4 2025) — margins, risk premia and standards sit between the policy rate and the cost a borrower actually pays.

Mapping these errors enables a more rigorous reading of rate signals, distinguishing what they actually convey from what they are made to convey.

Confusing nominal with real, short with long, policy rate with credit cost: the most common interest-rate analysis errors decoded. For context: comparing short rates and long rates across regimes.

In January 2026, the ECB cut its deposit rate by 25 basis points to 2.75%. Headlines unanimously framed the decision as “another cut to support the economy.” At the same time, the average rate on French mortgage loans remained stable at ≈3.4% according to the Observatoire Crédit Logement (Q4 2025), and the real yield on the 10-year OAT slightly increased. This gap between announcement and concrete effects illustrates a recurring problem: economic commentary relies on analytical shortcuts that distort the understanding of actual monetary conditions. Worth reading alongside: the transmission of monetary policy to company profits.

Conflating the Headline Rate With the Real Economic Cost

This confusion, the most fundamental, consists in interpreting a nominal rate without anchoring it to inflation. A policy rate at 2.75% with inflation at 2.4% (Eurostat, January 2026) corresponds to a real rate of ≈0.35% — slightly positive. The same policy rate with inflation at 1% would produce a real rate of 1.75% — meaningfully more restrictive. Yet the conventional diagnosis treats both situations as identical because the nominal rate is the same.

The practical consequences are substantial. In 2022, while the ECB raised nominal rates aggressively, real financing conditions remained accommodative because inflation exceeded policy rates by a wide margin. Forecasts of severe eurozone recession, anchored on the nominal move, overstated the effective tightening. To avoid this trap, an accurate reading starts from real rates and systematically adjusts the diagnosis to the inflation context.

Reasoning on Short Rates When the Economy Responds to Long Rates

The central bank’s policy rate is a very short-term rate — overnight for the ECB. But structurally important economic decisions — productive investment, mortgage credit, sovereign financing — depend on medium- and long-term rates. The thread is followed through in the comparative chronology of inversions and bull phases. These two segments of the yield curve do not always move in the same direction.

According to Banque de France data (January 2026), the 10-year OAT yield stands near 3.2% — a level that has only marginally reflected the four successive policy rate cuts since June 2024. The bond market embeds its own expectations on inflation, growth, and risk, which can diverge from the short-rate trajectory. Equating monetary policy with the policy rate alone amounts to reading only a fraction of the signal. The same logic is developed in the time lags between rates and profits.

Equating the Policy Rate With the Real Cost of Credit

The policy rate influences credit cost but does not determine it alone. Bank margins, risk premia, competitive conditions, and lending standards stand between the central bank’s decision and the rate effectively paid by the borrower. According to the ECB’s Bank Lending Survey (Q4 2025), eurozone banks maintained relatively strict lending standards despite policy rate cuts — a pattern consistent with risk perception that does not reduce to the level of the short rate.

This distinction explains why these confusions persist in public debate: the policy rate is a simple number, clearly communicated, while the real cost of credit results from a combination of factors hard to summarize in a single figure.

- The nominal rate does not measure the real economic cost of money — only the real rate, adjusted for inflation, allows accurate diagnosis of monetary conditions.

- Structurally important economic decisions respond to long rates, not the short policy rate — both segments can move in opposite directions.

- The real cost of credit incorporates bank margins, risk premia, and lending standards, which filter and at times contradict the policy rate signal.

These three shortcuts — nominal for real, short for long, policy rate for credit — reinforce each other and produce a systematically distorted diagnosis of monetary conditions. Reading rates through these filters supports a more accurate understanding of financial conditions beyond the usual shortcuts.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…