Why Real Interest Rates Stay Out of the Public Economic Debate

Central banks act on real rates internally — and communicate in nominal rates externally. That asymmetry is not an accident: it stems from three converging barriers (pedagogical, editorial, political) that keep the variable most consequential for the economy almost invisible in mainstream coverage. The consequences register in household and credit decisions.

Central banks model their stance through real rates. They communicate in nominal ones. That asymmetry is not an oversight — it is the structural shape of how monetary policy reaches the public.

TL;DR

The variable that most determines monetary policy's real effect is also the most absent from coverage of it: 'real rate' appeared in no headline across the ECB's four 2025 decisions.

- A review of the ECB's four 2025 decisions across Reuters, AFP and Bloomberg found the term 'real rate' in no headline and in under 5% of lead-level articles.

- Three converging barriers sustain the gap: the real rate must be computed (nominal minus a chosen inflation measure), newsroom formats reward clean announcements over decompositions, and central banks anchor communication on the nominal rate they actually set.

The variable most consequential for the economy is also the one most absent from the debate that concerns it. Three converging barriers — pedagogical, editorial, political — sustain that gap.

Real interest rates are rarely discussed in public debate despite their importance. Analysis of the media, political and educational barriers. The breakdown is provided in our reading of equity drivers under an inverted yield curve.

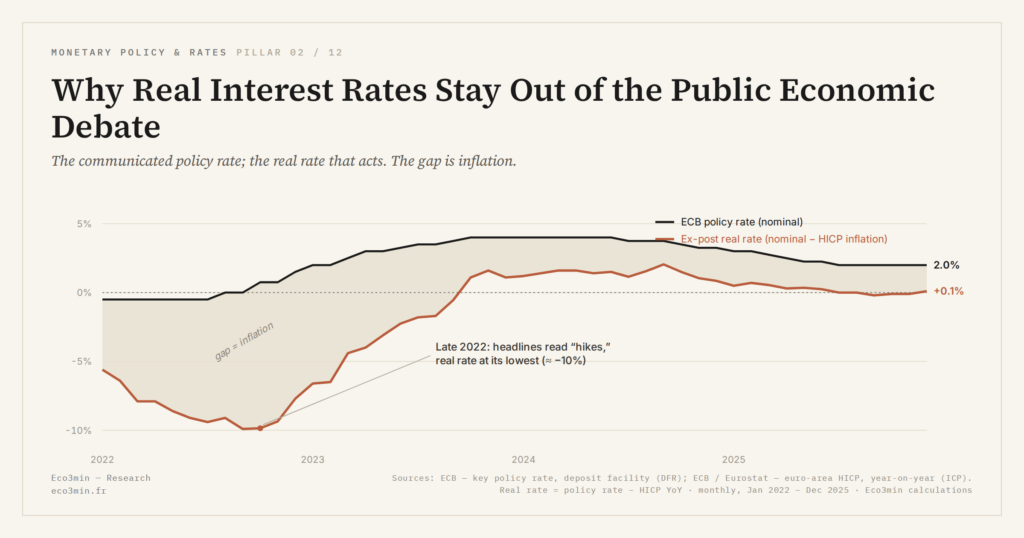

When the ECB cuts its policy rate by 25 basis points, the headline runs the nominal figure. No major generalist outlet simultaneously prints the resulting real rate — the one that actually governs the economic effect of the decision. A review of coverage on the ECB’s four 2025 decisions (Reuters, AFP, Bloomberg) shows the term “real rate” appearing in no headline and in fewer than 5% of lead-level articles. That invisibility is not a stylistic detail. It shapes how the public, commentators and at times policymakers themselves read why real rates anchor economic analysis.

Three barriers that converge on the same outcome

The first barrier is pedagogical. A real rate is not directly observable. It requires a calculation — nominal minus inflation — and a choice of inflation measure (realised, expected, underlying). The extra step is trivial for an economist and disqualifying for mass communication. A nominal rate is a raw figure, available in real time, comparable across periods. Further detail: the Eco3min dossier on the transmission from rates to company results.

The second barrier is editorial. Newsroom incentives favour announcements over decompositions. “ECB cuts to 2.75%” works as a headline. “ECB’s real rate moves from 0.6% to 0.35% adjusting for one-year inflation expectations” does not. Format constraints structurally promote the nominal shortcut over the real-rate translation.

The third barrier is political. Central banks set nominal rates; they do not set real rates. Communicating in nominal terms keeps the institutional message tethered to a variable they control. Acknowledging publicly that the actual stance of policy depends on inflation — a variable they only imperfectly steer — would surface ambiguity in the transmission story. Few central banks have found it useful to volunteer that.

The downstream cost of the gap

The absence of real rates from public coverage sustains the interpretive errors that follow from it: a high nominal rate is read as restrictive, a low one as accommodative, with no inflation context in the frame. That distorted reading enters household savings decisions — which underestimate wealth erosion in moderate inflation — and credit decisions, which overstate the real cost of borrowing when nominal rates look elevated.

The cost extends to macro debate. Conversations about debt sustainability, the attractiveness of savings or the stance of monetary policy proceed with a partial measurement instrument. Reading the cycle without real rates is itself a defective exercise — the case is laid out in our analysis of cyclical diagnosis through a real-rate lens.

- The absence of real rates from public debate stems from three converging barriers: the complexity of the calculation, the editorial preference for clean figures, and institutional communication anchored on the nominal — the variable central banks actually control.

- The gap sustains the confusion between headline rate level and the actual stance of monetary policy, with measurable consequences for savings and credit decisions.

- Reintroducing real rates into routine analysis materially changes the reading of monetary conditions — a practice that remains marginal in mainstream economic commentary.

The paradox is built into the system rather than added on top of it. The variable that determines the real impact of monetary policy is the one least visible in the debate about that policy. The gap is not a pedagogical inevitability but an implicit choice of simplification, and its costs register in the quality of economic diagnostics. Reading beyond the nominal headline toward actual financial conditions is the minimum requirement for anyone trying to understand — rather than merely react to — the monetary environment.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…