Compound Interest and Inflation: The Nominal Illusion

Analysis of the gap between nominal accumulation and real return when inflation compounds over time. Why long-horizon projections often overstate purchasing-power gains.

Analysis of the gap between nominal accumulation and real return when inflation compounds over time.

TL;DR

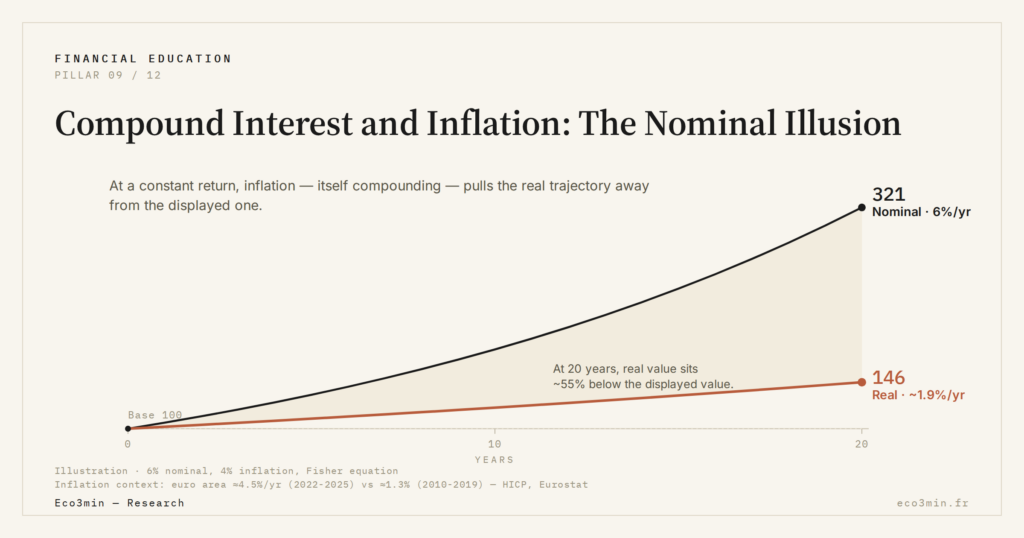

Compound interest accumulates nominally while inflation erodes purchasing power, so a 6% nominal return under 4% inflation leaves roughly 2% real, a gap that itself compounds over decades. The wider context: Eco3min’s financial tools and simulators.

- Between 2022 and 2025, inflation across developed economies ran around ≈4 to 5% depending on the aggregate, versus ≈1.5% the prior decade, while many projections still reasoned in nominal returns.

- Persistent inflation acts like an implicit negative rate applied each year to accumulated capital, so a gap that looks marginal over one year becomes structural over twenty.

- The divergence between nominal and real trajectories is non-linear: because inflation also compounds, the gap accelerates the longer the horizon.

A quiet mechanism is enough to distort the reading of many financial projections: compound interest always accumulates in nominal terms, while purchasing power erodes under the effect of inflation. As long as this distinction remains abstract, trajectories appear consistent. As soon as it is built into the calculation, part of the results changes in nature. This confusion between displayed value and real value belongs to a broader set of reading biases, detailed on the pillar page Financial Education.

When Compounding Masks Monetary Erosion

Compound interest calculations rest on a mechanical logic: each period capitalizes on the previous one. Within this logic, capital showing steady growth seems to translate into gradual enrichment. This reading dominates because it matches what most projection tools display.

Part of the implicit consensus holds that, over the long run, compounding eventually “offsets” inflation. This assumption presumes that inflation remains moderate and stable, and above all that it does not interact with the dynamics of the nominal rate. Yet, as soon as inflation settles above a few percent for several consecutive years, the real trajectory diverges noticeably from the displayed trajectory.

Between 2022 and 2025, average inflation observed across developed economies hovered around ≈4 to 5% depending on the aggregate used, against ≈1.5% over the previous decade. Over the same period, many projections still reasoned in nominal returns, without explicit purchasing-power adjustment.

Nominal vs Real: A Cumulative Gap, Not a One-Off

The error does not stem from a miscalculation but from a variable shift. Compound interest mechanically amplifies gaps, including those tied to inflation. Persistent inflation acts like an implicit negative rate applied each year to the accumulated stock.

A nominal return of 6% in an environment of 4% inflation does not correspond to “weak performance” but to a real return close to 2%. Over one year, the gap looks marginal. Over twenty years, it becomes structural. The issue is not the initial level but its repetition.

Dominant projections tend to smooth this reality by focusing on the final nominal capital. The analysis here diverges by showing that inflation does not only reduce the final outcome: it modifies the real slope of the trajectory, period after period.

What Projection Tools Reveal — and What They Don’t

Simulation tools, such as a compound interest calculator, perform their arithmetic function correctly: they show nominal compounding. Without critical reading, however, they can reinforce an illusion of real growth.

The tool is not “wrong.” It answers a precise question: how capital evolves at a given rate. The problem appears when this result is interpreted as a net economic gain, without rebasing in purchasing power. In a context of persistent inflation, this omission becomes non-marginal.

The gap between nominal and real trajectories is not linear. The longer the horizon, the faster the divergence accelerates, because inflation also operates in compounded fashion. To read that trajectory in current units rather than in purchasing power is the elementary error behind the persistence of money illusion.

Why This Illusion Is More Visible Now

Since 2024, the stabilization of policy rates at higher levels has not made inflation disappear, but has made it more heterogeneous. Dominant macro projections expect gradual disinflation, without a rapid return to the levels of the 2010s.

In this framework, the difference between displayed nominal return and perceived real return becomes more visible. Trajectories that looked robust under low-inflation assumptions appear noticeably more fragile once the monetary factor is reintegrated.

What the Consensus Underweights in This Reading

Central scenarios often assume that inflation is transient noise around a low average. This assumption allows reasoning to proceed primarily in nominal terms. The analysis here diverges not on the figures, but on the structuring variable: the duration over which inflation remains significant.

If this duration lengthens, even without further acceleration, the cumulative effect is enough to erode a substantial share of the real value accumulated. It is not a shock, but a permanent friction.

What Could Invalidate This Reading

Faster-than-expected disinflation, combined with real productivity gains, would sharply reduce the gap between nominal and real. Likewise, an environment of high real growth would more easily absorb monetary erosion. Conversely, more volatile or asymmetric inflation would further widen the observed gaps.

Observable Economic Implications

For households, reading in nominal terms can overstate real accumulation capacity. For companies, it can distort the assessment of long-term returns on financed projects. For markets, it helps sustain valuations built on future flows that are insufficiently deflated.

Treating steady nominal growth as real enrichment. This reading is misleading because it ignores the cumulative effect of inflation on the purchasing power of capital.

Last updated — 28 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Where the Livret A’s Money Goes: The Caisse des Dépôts Circuit and Social-Housing Finance

The savings held on Livret A accounts do not sit idle. A regulation-set share is centralised at the…

France’s LEP vs the Livret A: A Means-Tested Higher Rate, Explained

France’s Livret d’épargne populaire is often described as "the Livret A, only better". The description misleads: the LEP…

France’s Livret A Ceiling: What Happens Mechanically When a Capped Savings Account Is Full

France’s Livret A ceiling, €22,950, is one of the best-known figures in French saving and one of the…