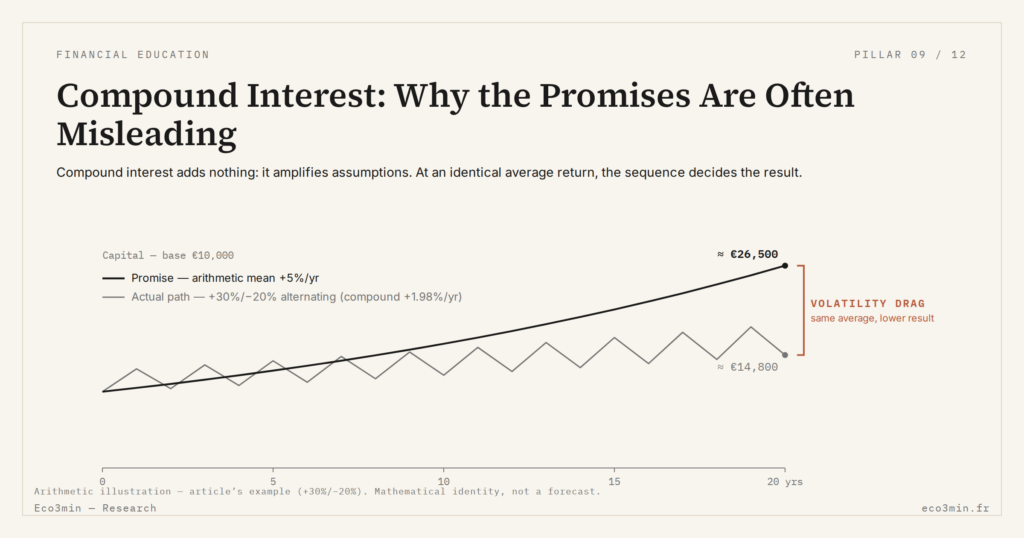

Compound Interest: Why the Promises Are Often Misleading

An examination of the unrealistic assumptions and marketing shortcuts often associated with narratives on compound interest and long-horizon projections.

An examination of the unrealistic assumptions and marketing shortcuts often associated with discourses on compound interest.

TL;DR

A constant annualized return applied over twenty or thirty years is the most fragile assumption beneath compound-interest projections, which also presume neutral time and frictionless conditions.

- Appealing projections apply one constant annualized return over twenty or thirty years, but real returns arrive sequentially; the contained volatility of 2010–2020 fed the illusion, and the higher-rate, more disrupted cycles since 2022 expose it.

- A long horizon does not generate performance; it works as a filter, selecting the trajectories that stay continuous and magnifying whatever gap the starting assumptions contain.

Compound interest is frequently presented as a near-automatic mechanism: a simple formula, a long horizon, and supposedly inevitable accumulation. This narrative rests on a series of implicit assumptions that are rarely made explicit, yet decisive for the real economic reading of projections. It is precisely in this gap between the theoretical mechanism and the concrete conditions of its implementation that most misleading promises take root. A complementary angle: the Eco3min framework on how households weigh financial decisions through the cycle.

The Quiet Mechanism Oversimplified by Common Narratives

Compounded capitalization operates on a strict rule: each period fully extends the previous one. This continuity assumes a stability of parameters — rate, flows, duration — that the most optimistic presentations take for granted. Yet in economic reality, these parameters are rarely constant over long horizons.

Part of the implicit consensus treats regularity as an operational detail, when in fact the heart of the mechanism depends precisely on this continuity. The slightest interruption, rate variation or change in pace alters the cumulative trajectory, without this appearing immediately in simplified scenarios.

Assumption #1: The Unrealistic Constancy of Returns

Appealing projections almost always rest on a constant annualized return, applied mechanically over twenty or thirty years. This assumption eases comprehension but masks a key reality: observed returns are sequential, not homogeneous.

Between 2010 and 2020, annual volatility on many financial assets remained contained, reinforcing the illusion of smooth trajectories. Since 2022, with the return of higher rate regimes and more disrupted cycles, this assumption of constancy looks markedly more fragile. This fragility of the constancy assumption is one of the points discussed in our analysis of the temporal structuring of financial decisions. The mechanism of compound interest amplifies these discontinuities; it does not correct them.

Assumption #2: Time Treated as a Neutral Variable

Promotional discourses give long horizons a central role but often treat them as an abstraction. Time is presented as an automatic multiplier, when it acts mainly as a filter: it selects the trajectories able to remain continuous.

This reading is precisely what a compound interest calculator can make visible when used as a trajectory tool, not as a final-result generator. The tool highlights that time does not create performance; it amplifies the gaps stemming from initial assumptions.

Assumption #3: Ignoring Real Economic Frictions

Taxation, inflation, flow interruptions, monetary regime shifts: these frictions are rarely integrated into the promises associated with compound interest. Yet each acts as a force of progressive degradation against the theoretical trajectory.

Aggregate estimates used in projections often assume moderate and stable inflation, around 1 to 2%. Between 2022 and 2025, average inflation observed in developed economies sat closer to ≈4%, materially altering the real reading of nominal accumulations. The gap is not a one-off shock but a repeated friction.

What the Consensus Assumes — and What This Reading Overlooks

The central scenario adopted by many actors assumes that these frictions cancel out over time: smoothed volatility, transient inflation, stable taxation. This assumption is not absurd, but it is never neutral. It fully conditions the validity of the promises being made.

The analysis here diverges not by rejecting this scenario, but by underlining that the mechanism of compound interest does not correct these gaps: it accumulates them. What is negligible over one year becomes structural over twenty.

What Readers Are Really Trying to Understand

Behind the promises associated with compound interest lies a simpler question: why do projected outcomes look so robust on paper, yet so sensitive to the assumptions retained? The point is not to challenge the mechanism, but to understand what can quietly weaken it.

What Could Invalidate This Reading

A long phase of stable real growth, combined with durably low inflation and unchanged taxation, would reinforce the consistency of theoretical trajectories. Likewise, a structural reduction in volatility would bring projections closer to simplified scenarios. Conversely, repeated regime breaks would further widen the gap between promise and reality.

Treating a compound interest projection as a likely outcome, without questioning the stability of the underlying assumptions. This reading is misleading because the mechanism amplifies gaps rather than correcting them.

Observable Economic Implications

For households, these promises can lead to overstating real long-term enrichment. For companies, they sometimes bias the evaluation of projects built on overly smoothed future flows. For markets, they sustain valuations grounded in lightly stressed theoretical trajectories.

This is not the central scenario today, but the main risk lies less in a calculation error than in a reading error. As long as assumptions remain implicit, the promises associated with compound interest will continue to look obvious — until the actual trajectory exposes their limits.

What This Mechanism Truly Reveals

- Compound interest guarantees nothing: it amplifies initial assumptions.

- The constancy of parameters is the most fragile condition of long-horizon projections.

- Repeated economic frictions matter more than one-off shocks.

To place this reading within a broader framework for understanding financial biases, the pillar page Financial Education offers a synthesis of recurring blind spots related to projections, delays and cumulative effects.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

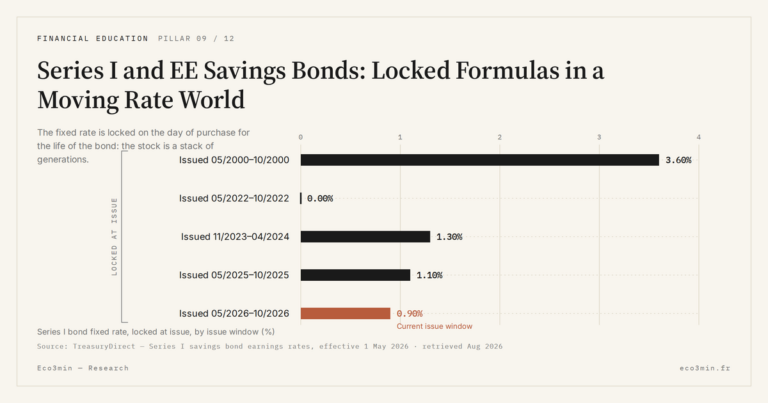

Full pillar →Series I and EE Savings Bonds: Locked Formulas in a Moving Rate World

US savings bonds lock a rate formula at the moment you buy them, for the life of the…

Where the Livret A’s Money Goes: The Caisse des Dépôts Circuit and Social-Housing Finance

The savings held on Livret A accounts do not sit idle. A regulation-set share is centralised at the…

France’s LEP vs the Livret A: A Means-Tested Higher Rate, Explained

France’s Livret d’épargne populaire is often described as "the Livret A, only better". The description misleads: the LEP…