Effective Fed Funds vs Target Rate Corridor: The IORB / ON RRP Band Mechanics and FOMC

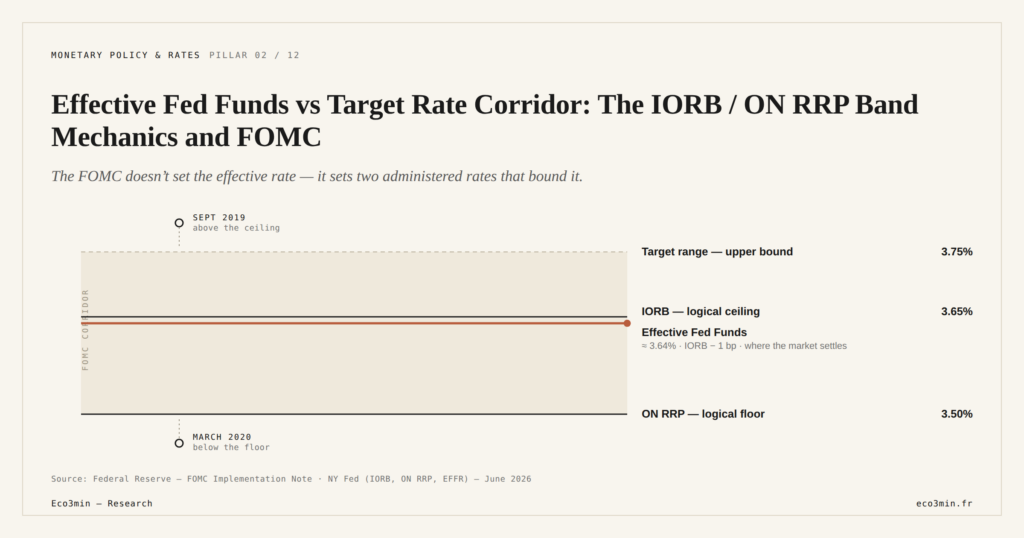

When the FOMC announces a target range, it does not directly steer the effective Federal Funds Rate: it sets two administered rates — IORB and ON RRP — that bound a corridor within which the market settles.

TL;DR

Two stress episodes mapped the post-2008 floor system's limits: September 2019 breached the IORB ceiling, March 2020 the ON RRP floor, prompting the 2021 Standing Repo Facility. A broader view: the upcoming FOMC sessions.

- Before October 2008 the NY Fed desk steered via open-market operations on scarce reserves; IORB plus QE imposed the floor system, with reserves climbing from under $50 billion in 2007 to $3.2 trillion in 2026.

- IORB is the logical ceiling and ON RRP the floor, a 25-bp gap held broadly constant since 2015; May 2026 sits at target 4.25-4.50%, IORB around 4.40%, ON RRP around 4.25%, effective around 4.33%.

- The plumbing that broke it was specific: September 2019 saw reserves fall to roughly $1.4 trillion with SLR-constrained arbitrage and SOFR at 10%, while March 2020 saw the $30-billion-per-fund ON RRP cap saturate and push the effective rate below its floor.

This post-2008 architecture replaced the open-market operations regime that prevailed before the financial crisis. Two stress episodes — September 2019, March 2020 — empirically tested its limits.

1. The Post-2008 Corridor Architecture: From Symmetric Regime to Floor System

Before October 2008, the Federal Reserve’s steering of the effective Federal Funds Rate rested on a fundamentally different mechanism from the current system. The Fed maintained a relative scarcity of bank reserves as a functional prerequisite, and the open market operations desk at the Federal Reserve Bank of New York intervened daily through Treasury purchases and sales to adjust available reserve quantities, and thereby the equilibrium price of the interbank market. If the effective rate threatened to deviate from the FOMC target, the desk injected or drained reserves until convergence. The corridor was symmetric: the discount window (the rate at which banks could borrow directly from the Fed as last resort) served as the logical ceiling, and the deposit facility rate — then unremunerated — served as an implicit floor at zero.

This regime assumed that banks actively sought to minimize their excess reserves, since those reserves earned no return. This constraint made the Fed Funds market highly active and sensitive to desk operations. In October 2008, the situation changed radically. The Federal Reserve began paying interest on bank reserves (Interest on Reserve Balances, IORB) at an administered rate. Simultaneously, the Quantitative Easing program flooded the system with reserves: the total stock exploded from less than $50 billion in 2007 to several hundred billion by end-2008, then $3.2 trillion in 2026 per Federal Reserve H.4.1.

With this new structural overliquidity context, steering through open market operations became inoperable: relative scarcity cannot be enforced when all banks collectively hold massive excess reserves. The Fed therefore shifted to a floor system, where monetary policy transmission flows through the administered rates bounding the corridor — and no longer through interbank arbitrage mechanically reacting to desk operations.

The current architecture, dubbed the “ample reserves regime” in Fed communications (Federal Reserve, Policy Implementation Note), thus rests on two administered rates that the FOMC sets in parallel to the target range announcement: IORB and the ON RRP rate. The open market operations desk retains a residual function for fine liquidity management (notably via the post-2021 standing facilities), but no longer steers the effective rate in the way it did before 2008.

This article describes the mechanics of this floor system, its empirical limits exposed by two stress episodes (September 2019 and March 2020), and the institutional evolution that followed. For the effective rate definition itself and its NY Fed-published computation methodology, see the cluster’s foundational article, which logically precedes this reading.

2. IORB and ON RRP: The Two Administered Rates Bounding the Corridor

The post-2008 corridor rests on two administered rates that the FOMC sets simultaneously with the target range at each monetary policy meeting. how central banks steer rate cycles retraces the successive episodes.

Interest on Reserve Balances (IORB) is the rate the Federal Reserve pays to banks on their excess reserves. No eligible commercial bank or credit union has economic reason to lend in the Fed Funds market below IORB, since the Fed itself remunerates its liquidity at that rate, without counterparty risk and without horizon constraint. IORB therefore constitutes the corridor’s logical ceiling: the effective rate should not durably exceed IORB.

At the other end, the Overnight Reverse Repo (ON RRP) rate is accessible to a set of eligible non-bank counterparties — primarily money-market funds, but also certain GSEs (government-sponsored enterprises) and foreign institutions. These counterparties place their liquidity with the Fed against Treasury collateral, at an administered rate the Fed sets. No money-market fund has interest in lending to a commercial bank below the rate at which the Fed itself borrows. The ON RRP rate therefore constitutes the corridor’s logical floor: the effective rate should not durably fall below the ON RRP rate.

Between these two bounds, the effective rate settles per the arbitrage conditions of the residual segment. In normal regime, the effective rate sits a few basis points above the middle of the target range, generally 5 to 10 bp below IORB. As of May 2026, target range 4.25-4.50%, IORB roughly 4.40%, ON RRP around 4.25%, effective rate around 4.33% — a Fed Funds vs IORB gap of roughly 7 bp typical of the contemporary regime.

This architecture presents three important properties. First, it is asymmetric in practice: stress episodes observed since 2008 generally manifest through a ceiling breach (the September 2019 case), much more rarely through a floor collapse (the isolated March 2020 case). Second, it is technically robust but empirically conditional: its functioning relies on the effective presence of arbitrageurs with sufficient balance sheets to exploit the gaps between the two administered rates and the Fed Funds market. When that condition fails (reserves too low, tight prudential constraints), the corridor briefly derails. Third, it is calibrated with a 25-basis-point gap between IORB and ON RRP — an institutional choice the Fed has maintained broadly constant since 2015, except for occasional adjustments in March 2020.

To understand how this mechanics inscribes into the broader Fed reaction function, see calibration through the Taylor Rule, treated in a dedicated cluster article.

3. The September 2019 Repo Spike: When the Corridor Breaks Through the Ceiling

On September 16 and 17, 2019, the U.S. financial system experienced the first major stress of the post-2008 corridor. The effective Federal Funds Rate, which usually floated a few basis points below the 2.10% IORB set at the time, suddenly exceeded 2.30% — above the corridor’s logical ceiling. On the adjacent collateralized repo market, SOFR temporarily spiked to 10% on September 17, a level never observed since the series’ creation (Federal Reserve Bank of New York, Operations Note September 2019).

The immediate cause was a temporary scarcity of available bank reserves. Several factors converged: simultaneous settlement of a large Treasury auction (which drained bank cash to the Treasury), quarterly corporate tax payments (again draining bank accounts to the Treasury General Account), and a total reserves level fallen to roughly $1.4 trillion — historically low for the post-QE regime. Below this threshold, certain commercial banks decided arbitraging the Fed Funds / IORB spread was no longer profitable, because their own balance sheet constraints (notably the Supplementary Leverage Ratio, SLR) made the operation costly in regulatory capital.

The Fed reacted in two phases. Immediately, the NY Fed desk launched massive overnight repo operations — several hundred billion dollars over the week — to directly inject missing reserves into the system. In the short term, the Federal Reserve restarted a T-bill purchase program of up to $60 billion per month (October 2019 – June 2020), explicitly presented as a technical balance-sheet management operation and not as a new QE round (Federal Reserve, October 11, 2019 Statement). These interventions brought the effective rate back within the corridor within weeks.

The episode revealed a structural vulnerability of the floor system: it depends on the effective presence of arbitrageurs with non-saturated regulatory balance sheets. When post-Basel III prudential constraints (SLR, LCR) make arbitrage costly for near-saturated banks, the corridor ceases to be mechanically binding — it becomes conditional on bank capital availability and on the absolute level of available reserves. This institutional lesson directly informed the creation of the Standing Repo Facility (SRF) in July 2021, addressed below (Office of Financial Research analysis 2020; Liberty Street Economics, post-mortem analysis).

4. March 2020 and the COVID Episode: Falling Below the ON RRP Floor

The second major corridor stress occurred in the opposite direction, during the COVID dash for cash of March 2020. On March 12 and 13, 2020, the effective Federal Funds Rate briefly drifted below the ON RRP floor rate, signaling a temporary corridor disconnection through excess liquidity concentrated at money-market funds.

The mechanism differed from September 2019. Facing the health and financial panic, institutional investors massively repatriated their liquidity to money-market funds — the dash for cash dynamic. These money-market funds, suddenly flush with cash, sought to place it quickly, first at the ON RRP, which constituted for them the safest facility. But the ON RRP facility capacity was at the time capped per individual counterparty ($30 billion per day per eligible fund), which quickly saturated available absorption. Excess liquidity then flowed to the uncollateralized Fed Funds market at rates below the ON RRP rate, temporarily plunging the effective rate below the corridor’s logical floor.

The Fed response combined several levers. Immediately, the FOMC convened an extraordinary session on March 15, 2020, and lowered the target range to 0.00-0.25%, effectively eliminating the need to defend a floor above zero. Simultaneously, ON RRP facility eligibility was broadened to absorb more liquidity (Federal Reserve, March 15-23, 2020 announcements). Swap lines with major foreign central banks were activated at full capacity, and massive QE began the following week (purchases exceeding $1.5 trillion of Treasuries over March-April 2020).

The episode taught a lesson symmetric to the previous one: the corridor is not mechanically binding on the lower bound either, and its functioning depends on the calibration of the ON RRP absorption capacity, on the individual constraints imposed on money-market funds, and more broadly on the robustness of arbitrageurs present in the market. Between 2020 and 2023, ON RRP balances peaked above $2.5 trillion at multiple points (historical record), reflecting both structural overliquidity and the eligibility broadening decided in 2020-2021 (Federal Reserve Bank of New York, ON RRP Operations Data).

5. The Standing Repo Facility and the Institutional Evolution Post-2021

The institutional teaching of both episodes led the Fed to formalize, in July 2021, the creation of the Standing Repo Facility (SRF) — a permanent instrument designed to place a hard ceiling on repo stress episodes and, indirectly, on the Fed Funds corridor.

The SRF operates on a simple principle: primary dealers and certain eligible banks can borrow overnight from the Fed against Treasury collateral, at a rate set by the Fed itself (typically IORB + 5 bp). The mechanism is analogous to a collateralized discount window, accessible daily and standardized. The SRF therefore creates a theoretical ceiling on repo operations: no primary dealer has interest in paying more on the private repo market than the SRF costs, which bounds SOFR spike episodes.

Indirectly, this ceiling also protects the Fed Funds corridor. Transmission is mechanical: when SOFR spikes, SOFR-Fed Funds arbitrage becomes unbalanced and the effective rate can follow upward, as in September 2019. By limiting the amplitude of SOFR spikes via the SRF, the Fed indirectly limits the probability of an IORB ceiling breach by the effective Fed Funds rate.

The post-2021 corridor architecture therefore rests on three coordinated instruments rather than the two initial administered rates. The addition of SRF as a third pillar, combined with the post-2020 ON RRP eligibility broadening, substantially strengthened the system’s robustness against future stress episodes. The Fed has not had to significantly activate the SRF since its creation — which can be interpreted either as a sign that the system is sufficiently sized to function without intervention, or as a sign that no comparable major stress has yet been observed. For the in-depth analysis of this integrated architecture and its role in the integrated reading of FEDFUNDS, see the cluster’s hub article, and for the architecture of Fed tools as a whole, the parent sub-pillar.

- The post-2008 floor system replaced the pre-2008 regime of open-market-operations steering. It rests on two administered rates bounding the effective Federal Funds Rate: IORB (ceiling) and ON RRP (floor), set by the FOMC alongside the target range.

- In normal regime, the effective rate settles 5 to 10 basis points below IORB, within the FOMC target range. May 2026 indicative: target 4.25-4.50%, IORB 4.40%, ON RRP 4.25%, effective ~4.33%.

- Two episodes empirically tested the corridor: September 2019 (upper breach, SOFR repo spike to 10%) and March 2020 (lower breach, COVID dash for cash). Both revealed the floor system’s dependence on effective arbitrageurs and facility calibration.

- The Standing Repo Facility (July 2021) adds a third institutional pillar: a hard ceiling on repo operations, which indirectly protects the Fed Funds corridor from SOFR spikes comparable to 2019.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…