Fed Funds and the Taylor Rule: Calibrating the Fed Reaction Function and the Gap to Prescription

The Taylor Rule, formulated in 1993 by John Taylor, is not a mechanical monetary policy recipe: it is a normative reaction function expressing what the nominal Fed Funds rate would be if the Fed minimized a quadratic loss function.

TL;DR

Whether the Fed at 4.25-4.50% is very restrictive or only modestly so depends on the r-star value plugged into the Taylor Rule, a benchmark the FOMC has never formally adopted.

- Four variants (Taylor 1993, Taylor 1999, balanced approach, first-difference) diverge by 100 to 200 basis points at any moment, making any single 'true' prescription untenable.

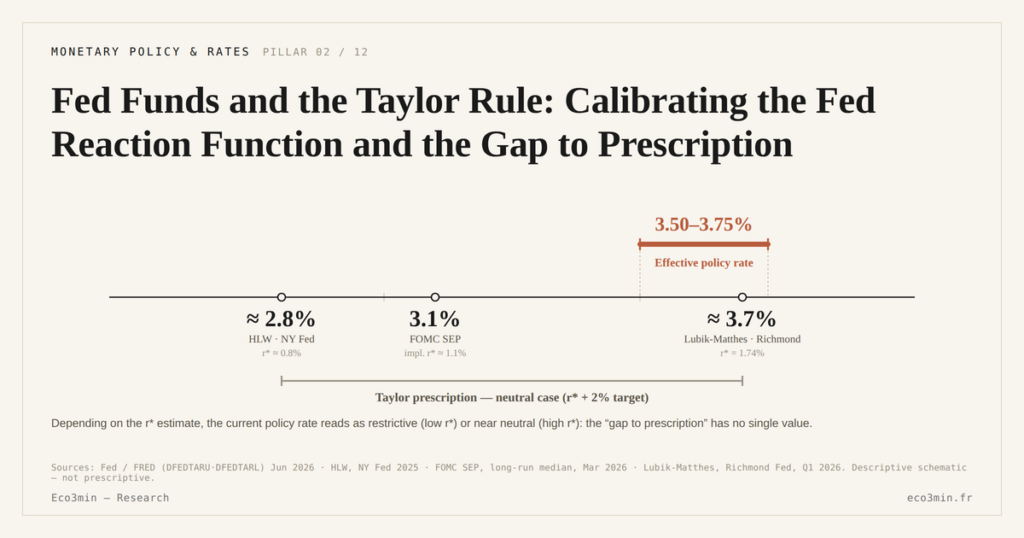

- Central r-star estimates span 0.7% (Holston-Laubach-Williams) to 1.5% (Lubik-Matthes); at inflation on target the prescription becomes r* + 2%, i.e. 2.7% to 3.5%.

- Across 1990-2026, observed Fed Funds tracked Taylor under Greenspan 1987-1995, ran well below it in 2001-2005, and started over 500 bp behind in 2022 under Powell.

Four main variants coexist in the literature; their prescriptions can diverge by 200 basis points at a given moment. Rigorous reading requires naming the variant and the retained parameters.

1. The Canonical Taylor 1993 Formulation and Its Economic Intuition

The Taylor Rule was formulated by economist John B. Taylor in his article “Discretion versus policy rules in practice” published in Carnegie-Rochester Conference Series on Public Policy in 1993. The article initially aimed to propose a simple benchmark for empirically evaluating FOMC decisions over the 1987-1992 period — not to impose a mechanical rule on monetary policy. But its formal simplicity and retrospective explanatory power quickly established it as the dominant reference for any analysis of the Fed reaction function. Related framing: the Eco3min frame for central-bank action.

The canonical form: i = r* + π + 0.5 × (π − π*) + 0.5 × output_gap, where i is the optimal nominal Fed Funds (prescription), r* the real natural rate (r-star), π observed inflation, π* the inflation target (2% for the Fed since formal adoption in 2012), and output_gap the deviation of observed GDP from potential GDP expressed as a percentage of potential GDP.

The economic intuition is simple. When observed inflation exceeds the target (π > π*), the (π − π*) term raises the prescription beyond the neutral Fed Funds (r* + π*), pushing toward restrictive policy. When the output gap is negative (economy in under-employment), the output_gap term reduces the prescription, pushing toward accommodative policy. The 0.5 coefficients assigned to each term reflect the weighting Taylor initially proposed, derived empirically from the 1987-1992 calibration. The rule therefore implicitly assumes that the Fed gives equivalent weight to price stability and activity stabilization — a normative hypothesis that can be contested depending on the period and monetary regime.

An often-neglected point: the Taylor prescription is not a target the Fed must reach, it is a normative benchmark against which to measure effective decisions. The FOMC has never formally adopted the Taylor Rule as a monetary policy constraint. Several reasons explain this: the r* and π* parameters are not precisely observable; the 0.5 coefficient on output_gap rests on a calibration specific to 1987-1992 that can be contested in other eras; the rule ignores by construction the financial stability and international transmission considerations that weigh in modern FOMC deliberations. A parallel read: FEDFUNDS Meaning and Computation.

This article details the formulation, its main variants, its numerical sensitivity to parameter choices, and its diagnostic use in practice. For the definition of the effective Federal Funds Rate on which the prescription applies, see the cluster’s foundational article; for the integrated framework within which the Taylor Rule sits, see the full FEDFUNDS reading framework, the cluster’s hub article.

2. The Rule’s Variants: Taylor 1999, Balanced Approach, First-Difference, Bullard

Monetary literature has produced several variants of the Taylor Rule, differing by the coefficients assigned to inflation and output gap terms, by the introduction of inertia, or by the explicit consideration of additional variables. Four variants structure the contemporary academic and institutional debate.

Taylor 1993, already described, remains the historical reference. Coefficients (0.5; 0.5) on (π − π*) and output_gap, no inertial term. It assumes a symmetric response to both objectives and immediate reaction without smoothing.

Taylor 1999, proposed by Taylor himself in a revision published by the Brookings Institution, doubles the output gap coefficient to 1.0 — coefficients (0.5; 1.0). This variant assigns relatively greater weight to activity stabilization. Its prescription is generally more accommodative in phases of negative output gap (recession or slowdown) and more restrictive in overheating phases. Several Fed board economists, notably Janet Yellen before her chairmanship, publicly preferred this variant to the original 1993 formulation.

The balanced approach rule is related to Taylor 1999 but with a generalization of coefficients. The semi-annual Federal Reserve Monetary Policy Report systematically compares the Taylor 1993, balanced approach, first-difference, and inertial Taylor prescriptions. The balanced approach generally uses coefficients (0.5; 1.0) with an additional smoothing term — amounting to a smoothed Taylor 1999, better aligned with the FOMC’s empirically observed behavior, which rarely practices abrupt jumps between two meetings. Read alongside: how the ECB-Fed spread drives EUR/USD.

The first-difference rule, also called “speed-limit policy”, abandons the level target and steers the change: i_t − i_{t-1} = α × (π − π*) + β × Δoutput_gap. This variant avoids the critical dependence on r*, an unobservable parameter. Its prescription specifies by how much the Fed should adjust its policy rate, not where it should land. Several monetary economists (notably Orphanides and Williams, 2002, 2007) have defended this variant as more robust to r* estimation errors. But it suffers from another limitation: it depends on the past trajectory, which complicates its interpretation as a timeless benchmark.

The Bullard non-linear rule, proposed by James Bullard (St Louis Fed) in his 2018-2022 speech series, introduces asymmetry in the loss function: the cost of a positive inflation deviation (above target) is weighted more heavily than the cost of a symmetric negative deviation below. This asymmetry produces a Taylor prescription that reacts more aggressively to inflation overshoot than to undershoot — which empirically comes closer to Fed behavior over the 2022-2023 cycle than symmetric variants.

Finally, several authors have proposed inertial Taylor rules integrating inertia i_t = ρ × i_{t-1} + (1-ρ) × Taylor_prescription_t, where ρ falls between 0.5 and 0.8 depending on estimates. This inertia empirically reflects the FOMC’s observed practice, which rarely adjusts by more than 25 or 50 basis points between two meetings, whereas a pure Taylor would prescribe larger jumps in cycle periods.

None of these variants is officially adopted by the FOMC. But their dispersion informs the debate: at any given moment, competing prescriptions can diverge by 100 to 200 basis points, which makes a mechanical reading of the “true” Taylor prescription impossible.

3. Numerical Sensitivity to r*, π*, and Coefficients

The numerical sensitivity of the Taylor prescription to parameter choices deserves detailed examination, as it determines the interpretation margin monetary economists exploit in their analyses. Three parameters dominate the prescription: r*, π*, and the coefficients on (π − π*) and output_gap.

r* — the real natural rate — has been the subject of an open debate since 2020, treated in the r-star parameter in the Taylor Rule. Contemporary central estimates range from 0.7% (Holston-Laubach-Williams) to 1.5% (Lubik-Matthes), with Fed staff at 1.0-1.2%. The practical gap on the Taylor prescription is immediate: with π* = 2% and inflation at mandate (π = 2%, so (π − π*) term = 0 and output_gap = 0), the prescription reduces to i = r* + π. With r* = 0.7%, prescription = 2.7%. With r* = 1.5%, prescription = 3.5%. An 80-basis-point gap on the r* choice alone, which can reach 100 bp in the high vs low ranges of available estimates.

π* — the inflation target — is officially set at 2% by the Fed since formal adoption of flexible average inflation targeting in 2012, confirmed and reinforced by the 2020 pivot. Before 2012, the Fed had no explicit target but operated implicitly around 2% per several estimates (Bernanke-Mishkin, 2003). The 2020-2025 academic debate saw several economists propose raising π* to 3% or 4% to provide more margin against the zero lower bound (Blanchard, 2010; Krugman, 2014-2015; post-COVID debates 2022-2024). The Fed has not adopted such a raise as of this writing. On the Taylor prescription, a π* of 3% instead of 2% reduces the prescription by 0.5 point when inflation is at target: a symmetric effect to a change in r*.

The coefficients on (π − π*) and output_gap determine the response aggressiveness. With inflation at 4% (π − π* = 2%) and output gap zero, the Taylor 1993 formulation (coefficient 0.5) prescribes i = r* + 2 + 0.5 × 2 + 0 = r* + 3%. Taylor 1999 (output coefficient 1.0) with the same inflation prescribes the same in this case, but with output gap = −2% (recession), Taylor 1993 removes 0.5 × 2 = 1% from the prescription, while Taylor 1999 removes 1.0 × 2 = 2%.

The 2022-2023 cycle illustration is striking. With core PCE inflation at 5.2% in June 2022, output gap near zero, and r* at 0.5% (the dominant pre-revision estimate at the time), the Taylor 1993 formulation prescribed i = 0.5 + 5.2 + 0.5 × 3.2 = 7.3% in June 2022 — while the observed Fed Funds was at 1.5-1.75% on the same date. A 550-basis-point gap, a massive signal of behind-the-curve policy. With r* revised to 1.2% (contemporary estimate), the prescription rises to 8.0% — an even larger gap. This episode is regularly cited in post-2022 literature as illustration of the cost of a delayed response to an inflationary shock, a reading that fits within the post-mortem debate on the 2021-2022 transition (Summers, Blanchard, Bauer-Rudebusch, 2022-2024).

4. Practical Reading: Behind/Ahead the Curve and the Dispersion of Prescriptions

The practical use of the Taylor Rule by monetary economists and market participants flows through two continuous tools published in real time by regional Federal Reserve Banks: the Cleveland Fed Taylor Rule utility and the Atlanta Fed Taylor Rule monitor.

The Cleveland Fed publishes a monthly update of several Taylor variants (1993, balanced approach, first-difference, inertial) with their current prescriptions and history from 1990-present. The utility allows users to specify their own r*, π*, and coefficient choices to explore sensitivity. It is the reference tool for any comparative analysis of competing prescriptions.

The Atlanta Fed publishes a Taylor Rule monitor with a more narrative reading, regularly integrating analyses of the FOMC position relative to competing prescriptions. The monitor was particularly active over the 2022-2023 cycle, continuously documenting the gap between observed Fed Funds and Taylor prescription under different r* assumptions.

The standard diagnostic distinguishes three FOMC position situations. Ahead of the curve: observed Fed Funds exceeds the Taylor prescription, policy more restrictive than theoretically required. Behind the curve: observed Fed Funds is below the prescription, policy more accommodative than required. On the curve: the gap is within a narrow neighborhood, generally plus or minus 50 bp from the prescription.

Empirical application over 1990-2026 reveals several canonical phases. Greenspan 1987-1995 broadly tracked Taylor 1993 prescriptions, which contributed to the rule’s initial empirical legitimacy. Greenspan 2001-2005 maintained Fed Funds significantly below Taylor for several years, an episode retroactively identified by Taylor himself (2007, Jackson Hole Symposium) as a contributor to the housing bubble. Bernanke-Yellen 2008-2015 (ZIRP) operated under a zero lower bound constraint that made any negative Taylor prescription unimplementable. Powell 2022-2023 began with a massive Taylor gap (500+ bp behind), progressively reduced with the aggressive hikes but never fully converging on the more demanding variants — the episode remains under-tightened on certain variants even at the July 2023 cycle peak.

The Taylor Rule sits itself within the corridor framing the Taylor prescription and more broadly within monetary policy rules whose architecture is described in the parent sub-pillar.

- The Taylor Rule (1993) expresses what the optimal nominal Fed Funds would be if the Fed minimized a quadratic loss function weighting inflation-target deviation and output gap. Canonical form: i = r* + π + 0.5 × (π − π*) + 0.5 × output_gap.

- Four main variants coexist: original Taylor 1993, Taylor 1999 (output gap coefficient at 1.0), balanced approach (with smoothing), first-difference (steering the change). Their prescriptions can diverge by 100 to 200 basis points at a given moment.

- Sensitivity to r* is massive: with π* = 2% and inflation at mandate, prescription = r* + 2%. So 2.7% (HLW r* = 0.7%) or 3.5% (Lubik-Matthes r* = 1.5%). The r* choice determines whether the current Fed at 4.25-4.50% is very restrictive or only modestly restrictive.

- Practical use of the rule flows through the Cleveland Fed Taylor Rule utility and Atlanta Fed monitor, published continuously with different variants. Standard diagnostic distinguishes three Fed positions: ahead of the curve, on the curve, behind the curve.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…