Five Reading Traps That Distort the Economic Cycle

Five recurring errors corrupt the reading of the economic cycle: reacting to isolated figures, conflating correlation and causation, extrapolating from two points, ignoring revisions, and treating lagging indicators as leading signals. They rely on real data interpreted out of context — and trip up professionals as routinely as amateurs.

Five reading errors systematically distort the diagnosis of the economic cycle: isolated figures, false causation, linear extrapolation, ignored revisions, and confused timing of indicators.

TL;DR

Five recurring traps turn accurate, freely available data into wrong cycle calls when they stack: an isolated print, extrapolated into a trend, then sealed by a lagging indicator.

- The BLS revises its non-farm payroll figure three times after the first release, with an average revision range near ±30,000 jobs, so a diagnosis built on the initial estimate is built on a draft.

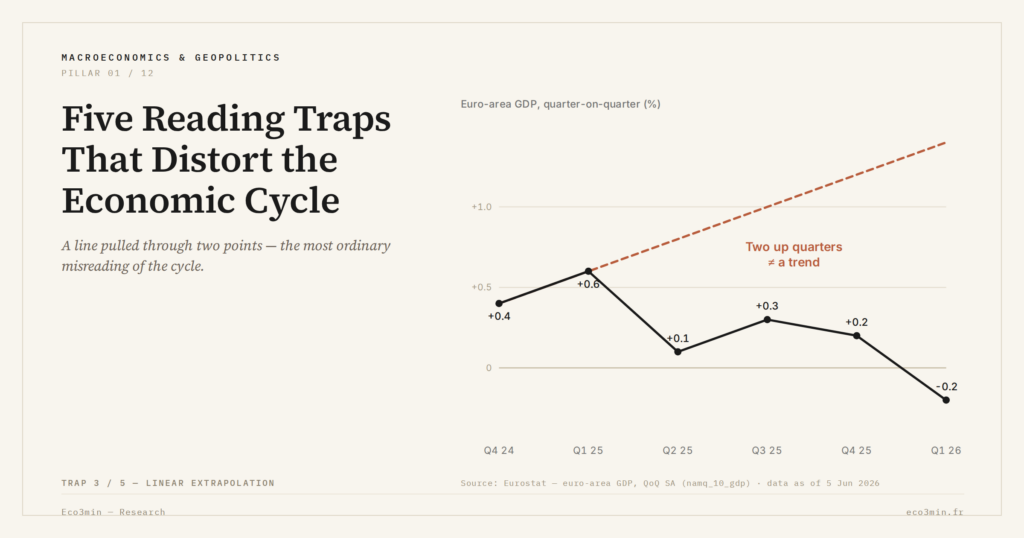

- Euro-area quarterly growth ranged between -0.1% and +0.4% over the four quarters to November 2025 (OECD), a sequence where drawing a straight line is as tempting as it is misleading.

The most common failure in cycle reading is not the absence of data. It is the misuse of data that is accurate, recent, and freely available. Five errors recur with striking regularity: reacting to a single monthly release, confusing correlation with causation, extending a trend from two data points, ignoring statistical revisions, and treating a lagging indicator as a leading one. Each of these traps rests on real numbers interpreted out of context — which makes them harder to detect than outright misinformation.

These mistakes do not single out novices. Professional investors, specialised commentators, and at times the central banks themselves stack them in the same reasoning. The pattern suggests less a competence gap than a set of cognitive shortcuts embedded in how the brain processes a noisy environment. Naming them is the first defence.

Trap 1 and Trap 2 — the isolated point and the false cause

The first trap is anchoring a diagnosis on a single release. A weak employment print, an upside surprise on inflation, a one-off industrial production drop: each publication can trigger a reaction disproportionate to its signal value. The structural volatility of monthly data and the bias introduced by serial revisions make individual prints unreliable for cyclical judgement. The BLS revises its non-farm payroll figure three times after the initial release, with an average revision range close to ±30,000 jobs. A diagnosis built on the first estimate is a diagnosis built on a draft.

The second trap is confusing correlation with causation. Two series moving together do not establish that one drives the other. The textbook case: public expenditure rises with growth, which is often read as fiscal stimulus pulling activity. The reverse causality is at least as plausible — automatic stabilisers expand mechanically when the cycle weakens. The real cycle runs through transmission chains that simple correlations cannot disentangle, particularly when several variables respond to a common underlying shock.

Trap 3 to Trap 5 — extrapolating, ignoring revisions, mistiming indicators

The third trap is linear extrapolation. Two quarters of growth do not establish a trend; two quarters of contraction do not define a recession. The OECD noted in November 2025 that euro-area quarterly growth had ranged between −0.1% and +0.4% over the previous four quarters — a sequence in which drawing a straight line is tempting and misleading in equal measure. The choice of observation horizon shapes what becomes visible in the cycle, and two data points never define a reliable trajectory.

The fourth trap is treating first releases as final. Initial estimates of GDP, employment, or industrial production are approximations, sometimes revised by several tenths of a point over the following quarters. The gap between what markets price in and what the productive economy delivers is partly explained by this revision process. A cycle that looks robust on first prints can read differently once the third revision lands.

The fifth trap is conflating lagging and leading indicators. The unemployment rate, by construction, is a lagging variable: by the time it rises, the slowdown is already several quarters old. The work of separating useful information from cyclical noise requires knowing the specific timing of each indicator before incorporating it into a diagnosis. Confusing the order of arrival of signals is enough to misdate a turning point by several quarters.

Stacking these traps in the same reasoning. A diagnosis built on an isolated monthly print (trap 1), extrapolated into a trend (trap 3), and concluded by reference to a lagging indicator (trap 5) chains three errors into one apparently coherent conclusion. The output looks like analysis. It is the residue of three biases compounded.

Recognising these traps does not mean suspending judgement until the data become flawless — they never do. Economic analysis operates under irreducible uncertainty. The structural reading frames that classify cycle phases and their market implications provide a way to formulate hypotheses that are testable against contradictory evidence, and that get revised when convergent signals — not isolated prints — justify the move.

Last updated — 14 June 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Monetary Tightening: How Central Banks Are Reshaping Financial Markets

After more than a decade of ultra-accommodative policy, monetary tightening has reintroduced the real cost of capital as…

Hidden Unemployment: Reading the Real Labor Market in 2026

Headline unemployment is stabilizing while broad underemployment still runs above pre-2020 levels. Reading the gap between official rates…

2026 Economic Outlook: Key Trade-Offs After the End of Cheap Money

2026 ushers in a more constrained macro regime where real rates stay positive, fiscal space narrows and geoeconomic…