Industrial Cycles and Long-Term Economic Trajectories

Long-term industrial cycles shape the real economy through productive capacity, infrastructure and the deep inertias they generate. Operating across decades, they define potential growth far beyond quarterly fluctuations.

Long-term industrial cycles shape the real economy through productive capacity, infrastructure, and the deep inertias they generate.

TL;DR

Industrial cycles run on a clock of 7 to 60 years, the Juglar, Kuznets and Kondratiev waves, and set growth potential long before any quarterly print registers it.

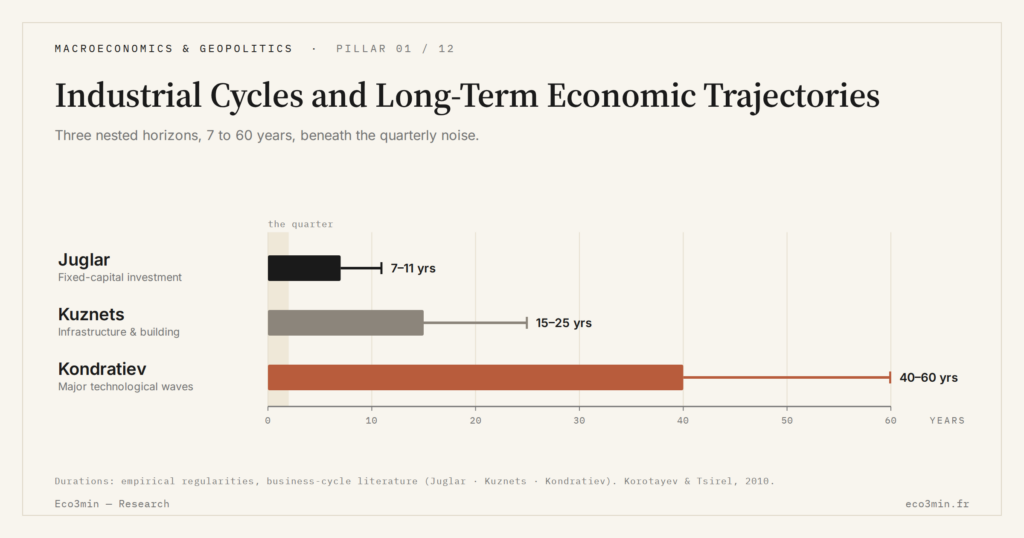

- Three nested horizons structure them: Juglar at 7 to 11 years (fixed capital), Kuznets at 15 to 25 (real estate and infrastructure), Kondratiev at 40 to 60 (technological waves).

- Clean-energy investment reached roughly $2 trillion a year in 2025, double its 2020 level (IEA, October 2025), reshaping productive capacity over decades rather than quarters.

- Digital-sector investment cycles are estimated at 5 to 7 years against 10 to 15 in traditional industry, compressing renewal, though physical infrastructure keeps its own inertia.

Economic fluctuations are usually read at the rhythm of quarterly releases. Industrial cycles operate on a different clock, sometimes several decades. They emerge from waves of investment in productive capacity, infrastructure choices and technological commitments. The inertias they generate define growth potential well before any quarterly print catches up with them. Ignoring them turns cyclical noise into a substitute for trend analysis.

What makes the topic more strategic than it looks today is the convergence of several industrial cycles approaching their end at the same time: the exhaustion of the housing cycle in several advanced economies, an energy transition challenging decades of fossil-fuel infrastructure, and the possible beginning of a new technology cycle driven by AI. These overlapping dynamics produce tensions that conventional cyclical indicators capture only imperfectly. This articulation points directly to the copper-to-gold ratio as a growth-versus-safe-haven gauge.

Horizons that outlast the business cycle

Industrial cycles differ from short-term fluctuations in both duration and drivers. The Juglar cycle, centred on fixed capital investment, spans 7 to 11 years. The Kuznets cycle, tied to real estate and infrastructure, covers 15 to 25 years. The Kondratiev cycle, associated with major technological waves, unfolds over 40 to 60 years. These horizons describe observed regularities, not mechanical laws.

The investment cycle and its proper temporality sits at the heart of these long-term dynamics. The real economic cycle and its capital-allocation mechanisms operate on these extended horizons. A factory commissioned today commits productive capacity for twenty or thirty years. An infrastructure network (rail, energy, digital) locks in technological trajectories for longer still. These inertias shape growth potential well beyond the quarterly arbitrages of financial markets.

Energy transition: an industrial cycle in motion

The transition toward decarbonised energy follows the logic of a large-scale industrial cycle. The International Energy Agency estimated in October 2025 that global investment in clean energy reached approximately $2 trillion per year, double the 2020 level. This flow reshapes productive capacity, builds new value chains and renders existing infrastructure obsolescent. The process unfolds over decades and modifies the real cycle in its productive foundations, not at its surface.

Mainstream projections point to an acceleration of the transition, but its trajectory depends on political, technological and financial variables that resist tidy modelling. The inertia of the existing capital stock (gas plants, distribution networks, internal-combustion vehicle fleets) mechanically slows the pace of substitution. Productivity dynamics and their link to the cycle will be decisive: if new energy technologies fail to generate sufficient efficiency gains, the ongoing industrial cycle could weigh on potential growth rather than lift it.

- Industrial cycles operate over 10- to 60-year horizons and shape growth potential well beyond quarterly fluctuations.

- The energy transition is a major industrial cycle in motion, with approximately $2 trillion in annual investment reshaping global productive capacity.

- The inertia of the existing capital stock slows the pace of these transitions and creates structural tensions invisible to short-term indicators.

The pace of technological change could nevertheless compress the duration of these cycles. The diffusion of AI across design, production and logistics processes potentially shortens the rate at which productive capacity renews itself. Some estimates put the investment cycle in digital sectors at 5 to 7 years, against 10 to 15 in traditional industry. The structural mechanisms governing the cycle may evolve accordingly. Physical infrastructure, however, keeps its own inertias regardless of what software innovation manages to deliver upstream.

Last updated — 14 June 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Monetary Tightening: How Central Banks Are Reshaping Financial Markets

After more than a decade of ultra-accommodative policy, monetary tightening has reintroduced the real cost of capital as…

Hidden Unemployment: Reading the Real Labor Market in 2026

Headline unemployment is stabilizing while broad underemployment still runs above pre-2020 levels. Reading the gap between official rates…

2026 Economic Outlook: Key Trade-Offs After the End of Cheap Money

2026 ushers in a more constrained macro regime where real rates stay positive, fiscal space narrows and geoeconomic…