Why Investment Drives the Economic Cycle

Investment is the main engine of the economic cycle owing to its volatility and its amplifying effect on activity. Its variations precede and magnify the inflections of overall output through the accelerator mechanism.

Investment is the main engine of the economic cycle owing to its volatility and its amplifying effect on activity.

TL;DR

Investment is demand's most volatile component, swinging three to four times as hard as GDP, and the accelerator effect makes it amplify every shift in final demand.

- Euro-area business investment rose 4.2% in 2024 then slowed to 0.6% in 2025 (Eurostat), a 3.6-point deceleration that weighed on GDP well beyond investment's roughly 22% share.

- The 2022 to 2024 tightening lifted corporate financing rates by 200 to 350 basis points by region, and euro-area loans to non-financial firms fell 0.4% year-on-year (ECB, December 2025).

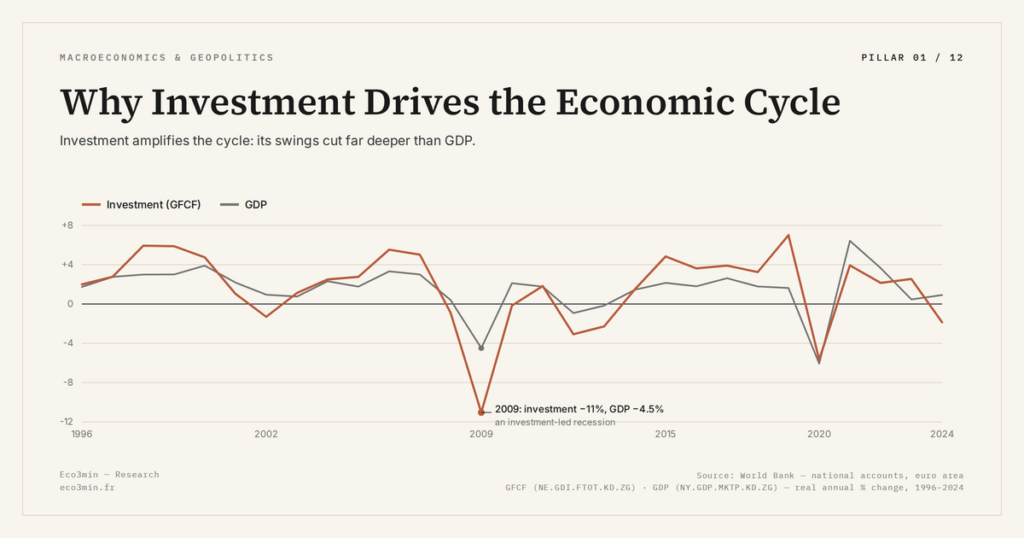

Investment is the most volatile component of demand and the primary driver of cyclical fluctuations. Its swings amplify expansionary and contractionary phases well beyond its share of GDP. Investment decisions depend on profitability expectations, financing conditions and the utilisation rate of existing capacity. These determinants generate threshold effects and self-reinforcing dynamics. Reading the real cycle without placing investment at the centre yields a partial, and often misleading, picture.

Household consumption captures most of the media’s attention, yet it is investment that tips the phases of the cycle. The full Eco3min framework on cycle phases is set out in the analysis of business-cycle phases. Investment’s volatility is three to four times that of GDP, which means turns in investment systematically precede and amplify inflections in overall activity.

The accelerator effect: why investment amplifies the cycle

The accelerator mechanism links variations in demand to investment decisions. When final demand rises, firms must expand productive capacity, generating an investment flow proportionally larger than the increase in demand itself. Conversely, a mere slowdown in demand growth can trigger an absolute fall in investment. The real economic cycle finds in this mechanism one of its primary drivers.

Eurostat reported that in the euro area business investment rose 4.2% in 2024 before slowing to 0.6% in 2025, a 3.6-point deceleration that weighed on GDP growth far more than the share of investment in final demand and its reading of the cycle (around 22% of GDP) would have suggested. This leverage explains why turns in investment constitute the most reliable signal of a phase change.

Three determinants of the investment cycle

The first determinant is the cost of capital. The monetary tightening of 2022 to 2024 raised corporate financing rates by 200 to 350 basis points depending on the region, rendering many investment projects unprofitable in the short term. The effect does not materialise immediately: ongoing projects continue, but new ones are postponed or cancelled. The ECB estimated in its December 2025 bulletin that the stock of loans to non-financial corporations in the euro area had fallen 0.4% year-on-year, the first signal of an effective adjustment.

The second determinant is the utilisation rate of existing capacity. As long as firms have unused production margins, they do not invest in new capacity. The link between capacity utilisation and the economy’s potential growth is direct: a negative output gap compresses the incentive to invest and prolongs the slowdown. The third determinant, profitability expectations, depends on both the current cycle and the long-term industrial transformations that redraw the leading sectors.

Reading investment by its annual flow without relating it to the existing capital stock. A rising gross investment figure can mask falling net investment after depreciation, meaning that the productive capital stock is contracting despite apparently sustained spending. It is net investment that determines the trajectory of capacity and, by extension, of the cycle.

The driving role of investment may need qualification in service economies, where physical capital weighs less. Intangible investment (R&D, software, data) obeys a different logic: shorter cycles, faster depreciation, lower interest-rate sensitivity. Fiscal policy and its interactions with the cycle can also alter the timing of public investment, creating impulses out of phase with the private cycle. The structural drivers of the cycle incorporate these developments, but the accelerator mechanism remains, for now, the dominant transmission channel in advanced economies.

Last updated — 16 June 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Monetary Tightening: How Central Banks Are Reshaping Financial Markets

After more than a decade of ultra-accommodative policy, monetary tightening has reintroduced the real cost of capital as…

Hidden Unemployment: Reading the Real Labor Market in 2026

Headline unemployment is stabilizing while broad underemployment still runs above pre-2020 levels. Reading the gap between official rates…

2026 Economic Outlook: Key Trade-Offs After the End of Cheap Money

2026 ushers in a more constrained macro regime where real rates stay positive, fiscal space narrows and geoeconomic…