Can Leading Indicators Really Anticipate the Business Cycle?

Leading indicators flag changes in conditions, not turning-point dates. The 22-month US yield curve inversion since 2022 shows how the same signal can fire for two different macroeconomic stories — and why directional convergence matters more than any single component.

TL;DR

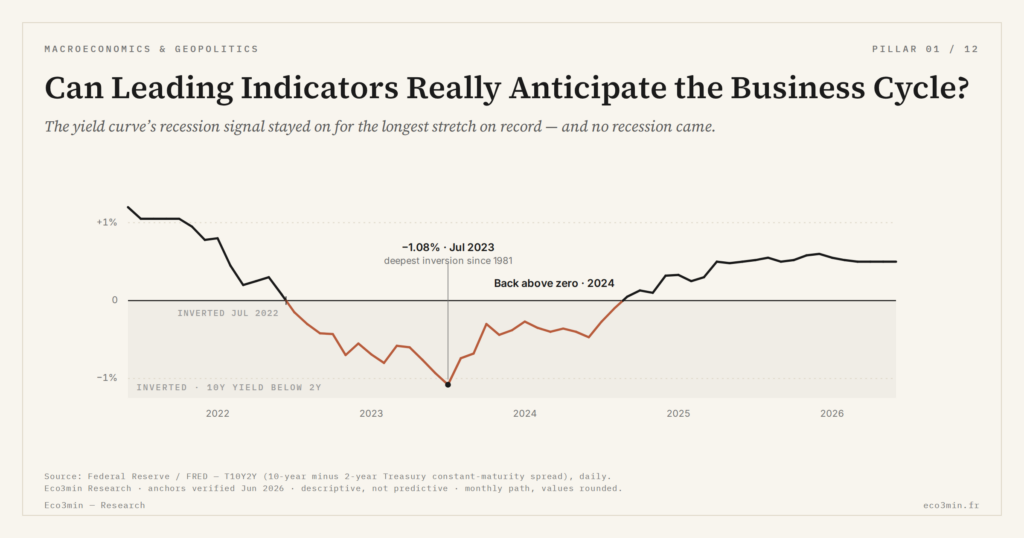

The yield-curve inversion ran 22 straight months into mid-2024 with no recession, showing that a leading indicator's reliability lasts only as long as the monetary regime that calibrated it.

- Across all seven US recessions since 1970 the curve inverted first, within 12 to 18 months before 1990; the post-2022 episode is the first to break that near-mechanical record.

- The Conference Board's Leading Economic Index fell for 24 straight months in 2022 to 2024, its longest contraction outside a recession, then stabilised with no structural reassessment.

- Inversion blends two forces, policy rates pinned high against inflation and growth expectations, so the same curve shape can carry either story, which is what makes the signal regime-conditional.

- By December 2025 the 10Y-2Y spread had normalised to +35 basis points (Cleveland Fed), a level that has historically coincided with the onset of recession rather than its avoidance.

The yield curve, a regime-conditional signal

The 10Y-2Y Treasury spread is the textbook leading indicator. Its track record before 1990 was nearly mechanical: inversion, then recession within 12 to 18 months. The 2022-2024 episode breaks that template. The Cleveland Fed reported in December 2025 that the spread had finally normalised to +35 basis points, a configuration that has historically coincided with the onset of recession rather than its avoidance — a footnote that reverses the usual reading direction. The reason the signal weakened is mechanical, not anecdotal. Curve inversion reflects two distinct forces: monetary policy expectations and growth expectations. When the Fed maintains policy rates above neutral to compress inflation while activity holds up, the curve inverts because short rates are anchored high — not because long-end growth is collapsing. The same shape, two different macroeconomic stories. Reading inversion as an unconditional recession signal ignores which of those two stories is dominant in any given cycle. Investment and productivity dynamics shape the real cycle at horizons the bond market cannot price by itself.Composite indicators face the same regime sensitivity

The Conference Board’s Leading Economic Index aggregates ten components: building permits, ISM new orders, the term spread, average weekly hours in manufacturing, jobless claims, consumer expectations and four others. The LEI declined for 24 consecutive months between 2022 and 2024 — its longest contraction outside an actual recession. The recession never materialised. In 2025 the index stabilised and rebounded marginally, without the Conference Board issuing a structural reassessment of the diagnostic. Two factors degraded the signal. The first is composition: components weighted on manufacturing and housing pick up the duration shock of a rate-hiking cycle, while services — now over 70% of US GDP — barely register. The second is the indicator’s calibration period, which spans cycles dominated by demand shocks, not the supply-and-policy shocks of the post-pandemic regime. Confidence surveys feed into the LEI with the same regime fragility: their correlation with subsequent activity has weakened markedly since 2020, a degradation also visible in the recurrent errors of economic forecasting models over the past five years.Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Monetary Tightening: How Central Banks Are Reshaping Financial Markets

After more than a decade of ultra-accommodative policy, monetary tightening has reintroduced the real cost of capital as…

Hidden Unemployment: Reading the Real Labor Market in 2026

Headline unemployment is stabilizing while broad underemployment still runs above pre-2020 levels. Reading the gap between official rates…

2026 Economic Outlook: Key Trade-Offs After the End of Cheap Money

2026 ushers in a more constrained macro regime where real rates stay positive, fiscal space narrows and geoeconomic…