Low Rates and Growth: The Gap Between Intent and Outcome

Low rates were meant to expand credit, lift investment and re-anchor growth. The eurozone decade of 2012-2022 shows what the channels actually delivered — and why the gap between intent and outcome matters more than the rate level itself.

The case for low rates rests on a set of intended channels — cheaper credit, more investment, more activity. The case against rests on a different question: what did those channels actually deliver once they ran for a decade?

TL;DR

Accommodative policy promised cheaper capital, easier credit and asset-price support, but across the eurozone's 2012-2022 decade those three intended channels delivered something measurably different from their design.

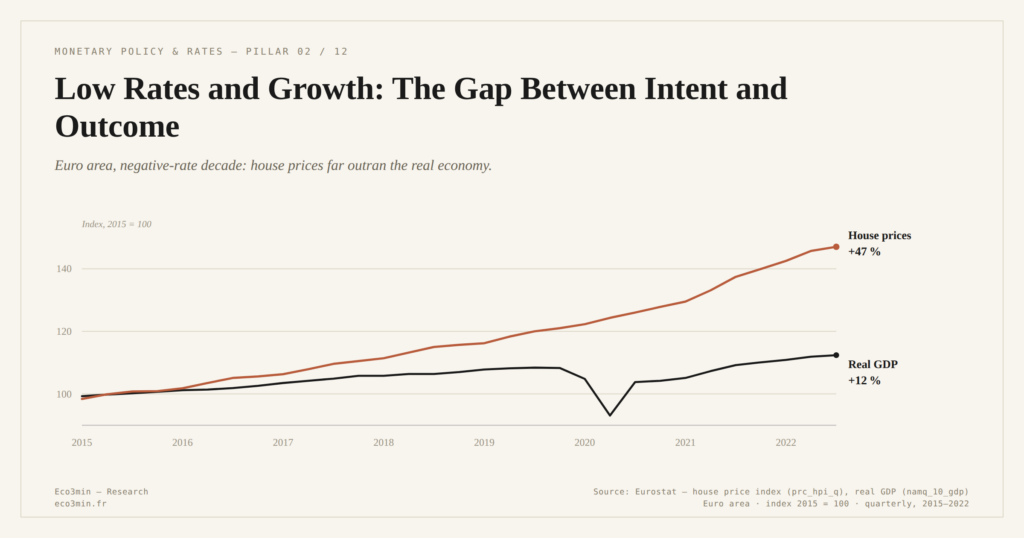

- Real rates stayed negative throughout 2012-2022, yet eurozone growth averaged only about 1.4% a year (Eurostat), with productivity slowing and R&D capex failing to scale.

- BIS data (2024 Annual Report) show the credit concentrated in real estate and share buybacks rather than industrial capex, with eurozone house prices up about 35% from 2015 to 2022 (Eurostat), reaching balance sheets rather than the productive base.

The eurozone’s experience between 2012 and 2022 turns this from a theoretical debate into an empirical one. The data show a wedge between what monetary easing was designed to produce and what materialized.

Cheap money was meant to expand credit, lift investment and re-anchor growth. Analysis of what the intended channels actually delivered.

The case for accommodative monetary policy is built on three intended channels: a lower cost of capital lifts business investment, eased credit conditions support consumption, and asset price effects reinforce both. Run for a few quarters, the model performs as advertised. Run for a decade, the gap between intent and outcome opens up. Between 2012 and 2022 the eurozone held real rates negative throughout, and average real GDP growth came in at ≈1.4% per year (Eurostat). Productivity slowed, R&D capex did not scale, and the share of fragile firms increased. The mismatch invites a closer look at how the real rate shapes economic decisions over horizons longer than a single cycle.

What the textbook channel actually transmitted

Lower financing costs do bring marginal projects into scope. That part of the textbook is intact, and it is visible in the cross-asset behavior described in the Eco3min analysis of post-inversion equity rallies. What gets transmitted with prolonged negative rates, however, includes a second layer the textbook glosses over: firms whose business model cannot cover the normal cost of capital stop being filtered out. The OECD put the share of “zombie” companies among listed firms in advanced economies at ≈12% in 2021 — a record, directly tied to a real cost of financing that no longer disciplined survival.

The transmission is also asymmetric in where it lands. BIS data (2024 Annual Report) show that credit flows in advanced economies during the negative-rate period concentrated in real estate and share buybacks, not in industrial capex. Eurozone residential prices rose ≈35% between 2015 and 2022 (Eurostat). The cheap money got transmitted — to balance sheets, to financial assets, to existing housing stock — without reaching the productive investment the policy was built to support. That asymmetry sits at the core of what the perverse effects of negative real rates reveal about who actually receives the credit.

The channel that quietly closed

The least intuitive part of the gap concerns bank intermediation itself. Persistent low rates compress the margin banks earn on lending, and the eurozone net interest margin fell to ≈1.1% in 2020, from ≈1.6% in 2010 (ECB data). Below a certain margin, banks restrict credit to riskier borrowers rather than expand it — which is the opposite of what the easing was meant to achieve.

The ECB itself put a label on the phenomenon in its 2023 Working Paper output: the “reversal interest rate”, the level beyond which further easing tightens credit conditions instead of loosening them. That recognition matters because it acknowledges, in central bank language, that the transmission mechanism is not monotone — and that running it past a certain point closes the channel rather than widening it.

Reading the rate–growth link as a constant function — as if “lower rates” always produced “more growth” by the same amount. The intended effects are present at the start of an easing cycle and decay, or reverse, with duration. Compressed bank margins, misrouted credit and the survival of unviable firms are the structural reasons the gap between intent and outcome widens the longer the regime persists. On the same theme: our deep dive into how monetary policy reaches corporate earnings.

What this implies for reading 2026

The return to mildly positive real rates in early 2026 is not, by this logic, the source of weaker growth — it is the closure of a gap. Restoring a profitability filter on investment, rebuilding bank intermediation margins and unwinding the misrouted credit of the prior decade are slow processes that look like drag in the short run and like repair over the medium term. What matters analytically is less the absolute rate level than the duration of any given regime, and the distortions it has time to accumulate inside the financial conditions that fuel those distortions.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…