Negative Real Rates: How They Distort Economic Behavior

A decade of negative real rates after 2012 distorted capital allocation, encouraged debt accumulation and compressed risk premia. The exit from this regime is now revealing the cost of those distortions.

When real rates remain negative for several years, the price signals that guide capital allocation become distorted. The consequences only fully surface during normalization.

TL;DR

A decade of negative real rates in advanced economies penalized savers and subsidized borrowers, and the accumulated distortions in capital allocation only surface as rates normalize.

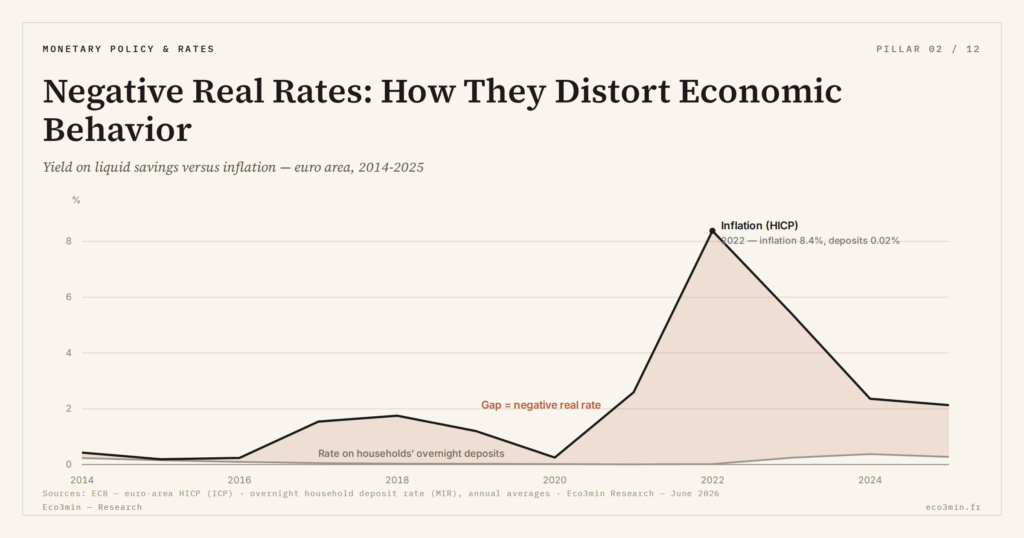

- The inversion is measurable: ECB data put the real return on eurozone household deposits near -2% between 2020 and 2022, an invisible tax on liquid wealth that mechanically rewards borrowing over accumulation.

- Cheap real capital sustained unproductive firms: the OECD estimated in 2021 that "zombie" firms, whose operating profits fail to cover interest, reached ≈12% of listed firms in advanced economies.

- The search for yield compressed risk premia: European high-yield spreads fell to ≈250bp in 2021 (ICE BofA) as record flows moved into high-yield credit, private equity and commercial real estate (BIS, 2023).

- Normalization is the revealer: eurozone corporate insolvencies ran ≈18% above their pre-pandemic level by Q3 2025 (Eurostat), consistent with the return of a real-profitability filter.

The decade of negative real rates in advanced economies after 2012 produced distortions whose economic cost continues to materialize.

Negative real rates distort capital allocation, encourage excessive borrowing and mask risk. Analysis of the systemic distortions. the limits of negative interest rates sets out the mechanism in detail. A broader view: our mapping of financial repression dynamics.

Between 2014 and 2022, the real return on bank deposits in the eurozone remained negative — a setup in which every euro saved lost purchasing power year after year. The point is set out at length in this question on cost of capital wacc. This systematic penalty on savers and implicit subsidy to borrowers did not go without consequence. The price signals that normally guide capital allocation gradually distorted: projects unviable under normal conditions found financing, the search for yield pushed toward increasingly risky assets, and debt accumulated without the apparent cost triggering any warning. Understanding the directing role of real rates in the economy clarifies why these distortions were predictable — and why their correction is unavoidable.

The Inversion of Fundamental Incentives

Negative real rates invert basic economic logic. Savers are penalized: according to ECB data, the average real return on eurozone household deposits stood at ≈-2% between 2020 and 2022 — an invisible tax on liquid wealth. Borrowers, in contrast, are subsidized: borrowing costs less in purchasing power terms than the nominal amount repaid. This sequence is documented in the mechanism of divergence between recession signals and equity performance. This asymmetry mechanically pushes toward debt and immediate spending at the expense of prudent accumulation.

For companies, the signal is just as distorted. Projects whose expected profitability is 1% in real terms become viable when the real cost of financing is -1%. The OECD estimated in 2021 that the share of “zombie” firms — companies whose operating profits do not cover interest expense — reached ≈12% of listed firms in advanced economies. This proliferation of low-productivity projects raises directly the question of the real effect of low rates on long-run growth.

The Search for Yield as a Systemic Effect

When safe instruments offer a negative real return, investors shift toward riskier assets to preserve purchasing power. According to BIS data (Annual Report 2023), flows into high-yield credit, private equity and commercial real estate reached record levels between 2019 and 2021 — precisely the period of the most negative real rates. Related framing: our note on the time lags between rate cycles and profit margins.

This compression of risk premia reduces the financial system’s capacity to discriminate between solvent and fragile borrowers. Eurozone credit spreads fell to ≈250 basis points for European high yield in 2021 (ICE BofA indices), before resetting during normalization. This mechanism directly links negative real rate distortions to the connection between distortions and cyclical turning points that characterizes late-cycle phases.

- Negative real rates penalize savers and subsidize borrowers, inverting fundamental economic incentives and favoring debt accumulation.

- The proliferation of “zombie” firms is a direct consequence of an artificially low real cost of capital sustained for a decade.

- The search for yield compresses risk premia and masks financial fragility — distortions that only surface when real rates normalize.

What Exiting the Negative Regime Reveals

The shift from negative to positive real rates acts as a revealer. According to Eurostat data (Q3 2025), corporate insolvencies in the eurozone rose by ≈18% relative to their pre-pandemic level — an adjustment consistent with the restoration of the real-profitability filter. This normalization process, painful in the short term, restores the capital allocation function that negative real rates had impaired. The current configuration sits within the liquidity environment at the origin of these distortions and their gradual unwinding. A related answer: the term premium and why it has been negative.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…