Why Monetary Policy Acts with Long, Variable Lags

Monetary policy effects diffuse with long, heterogeneous and unpredictable lags shaped by banks, credit cycles and expectations. Understanding why these delays are neither constant nor symmetric is key to reading cyclical signals.

Monetary policy rarely produces immediate effects. Between a central bank decision and its observable impact on the real economy, lags are long, heterogeneous and often unpredictable, sharply complicating the reading of cyclical conditions.

TL;DR

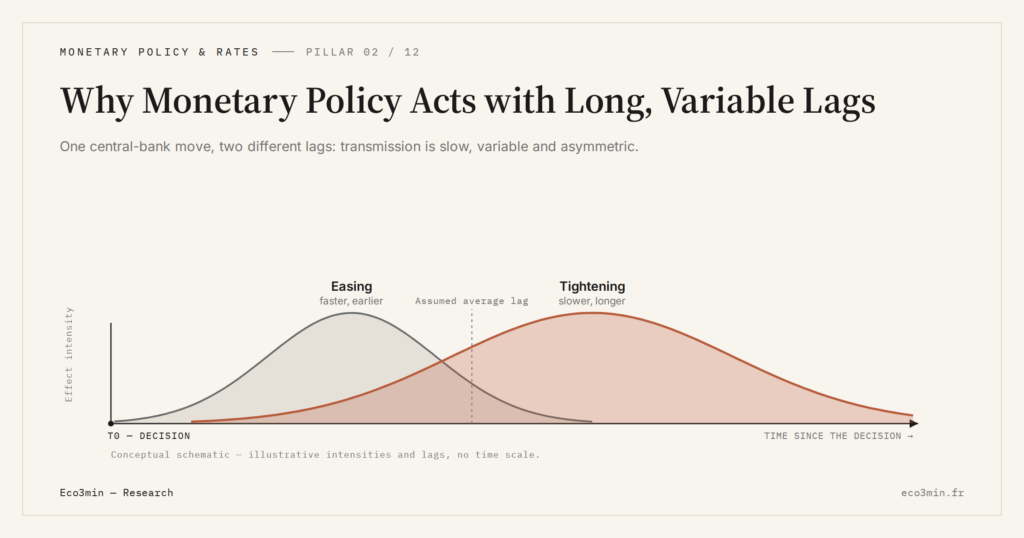

Models often assume monetary policy works with a stable 12-to-18-month lag, yet that delay stretches and compresses with the financial cycle, confidence and expectations.

- The common estimate of a 12-to-18-month average lag eases modeling but treats as fixed a delay that is actually endogenous to the financial context.

- In late 2025 a large share of corporate and household loans still carried conditions set years earlier, so credit volumes kept slowing even as rates stopped rising.

- Lags lengthen when the financial system is fragile or confidence is weak, and shorten in phases of euphoria or strong credibility, with 2025 surveys reporting investments deferred despite stable nominal rates.

The starting point is institutional. When a central bank shifts policy, it does not act directly on consumption, investment or employment. It first acts on the cost of bank liquidity, on refinancing conditions and on expectations. These intermediate channels are what introduce lags, sometimes longer than several quarters.

This general mechanism is detailed in our reference analysis on how monetary policy transmits to the real economy. The angle here is narrower: understanding why these lags are neither constant, nor symmetric, nor reliable from one cycle to the next.

The first filter: the banking system

Between the monetary decision and the real economy, the banking system acts as a shock absorber. A rate hike or cut immediately changes the marginal cost of refinancing, but does not instantly affect existing credit balances. In late 2025, a significant share of corporate and household loans remained indexed to conditions set several years earlier.

This gap explains why credit volumes can keep slowing while rates stop rising, or conversely remain dynamic after an initial easing. Transmission depends on the pace of loan turnover, the structure of bank balance sheets and risk appetite, all of which evolve slowly.

Dominant consensus and alternative reading

The central scenario adopted by many participants assumes monetary policy operates with a relatively stable average lag, often estimated between 12 and 18 months. This reading facilitates macroeconomic modeling and cycle projection.

Our analysis diverges on this point. Lags are not only long: they are variable. They lengthen when the financial system is fragile, when confidence is weak or when agents anticipate a rapid reversal. Conversely, they can shorten in phases of euphoria or strong monetary credibility. The lag is therefore not a fixed parameter, but an endogenous outcome of context.

A mechanism amplified by expectations

This variability in lags is largely explained by the role of monetary expectations in the transmission of monetary policy, which alter agent behavior well before accounting or statistical adjustments become visible.

Expectations play a central role in this variability. When firms anticipate durably restrictive financial conditions, they adjust investment decisions even before effective rates weigh on cash flow. In 2025, several surveys reported deferred investments despite stabilized nominal rates, a sign that the psychological effect preceded the accounting one.

Conversely, expectations of easing can delay the impact of tightening, prompting some actors to wait rather than adjust their behavior immediately.

Why this issue matters more now

After a prolonged tightening phase, advanced economies sit in a zone of uncertainty. Past decisions continue to diffuse while the macro context evolves. This gap between past action and current effects makes reading cyclical signals more complex than in more linear cycles.

What readers are really looking for

Behind the question of lags, the central concern is identifying whether the economy is still reacting to old decisions or already to a new monetary regime. The real question is not the next decision, but the stock of effects still in transmission. In depth: our breakdown of the delayed margin response to rate hikes.

Concrete observable impacts

For corporates, these lags translate into reduced visibility on the cost of capital. Hiring and investment decisions are made in an environment where the monetary signal is partly blurred. For households, the impact often appears later, through mortgage credit or durable consumption.

In financial markets, this timing explains phases of disconnect between immediate macro data and valuations, as participants try to anticipate where the economy stands in the transmission chain.

Useful indicators for reading lags

- Pace of credit balance turnover, an indicator of propagation time.

- Credit conditions reported by banks, often ahead of aggregated statistics.

- Gap between monetary decisions and volume reactions, revealing lengthening or shortening lags.

Alternative scenarios and limits

This reading assumes relative stability of the institutional framework. A major exogenous shock, a financial crisis or a regulatory rupture could abruptly accelerate transmission. Conversely, a highly expansionary fiscal policy could partly neutralize the monetary effect, further extending observed lags.

Reading perspective

The long and variable lags of monetary policy are not an anomaly but a structural feature. It is not the most discussed scenario, but it is a key factor in understanding why decisions sometimes appear ineffective or, conversely, excessive when they finally produce their effects.

To place this analysis in a broader frame, the pillar page on monetary policy and rates situates these lags among the other transmission channels.

3 takeaways

- Monetary policy acts first on intermediaries, which creates incompressible lags.

- These lags vary with the financial context, confidence and expectations.

- A large share of effects observed today still reflects past decisions.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…