Rate Cuts vs Slowdown: Why Monetary Easing Stalls

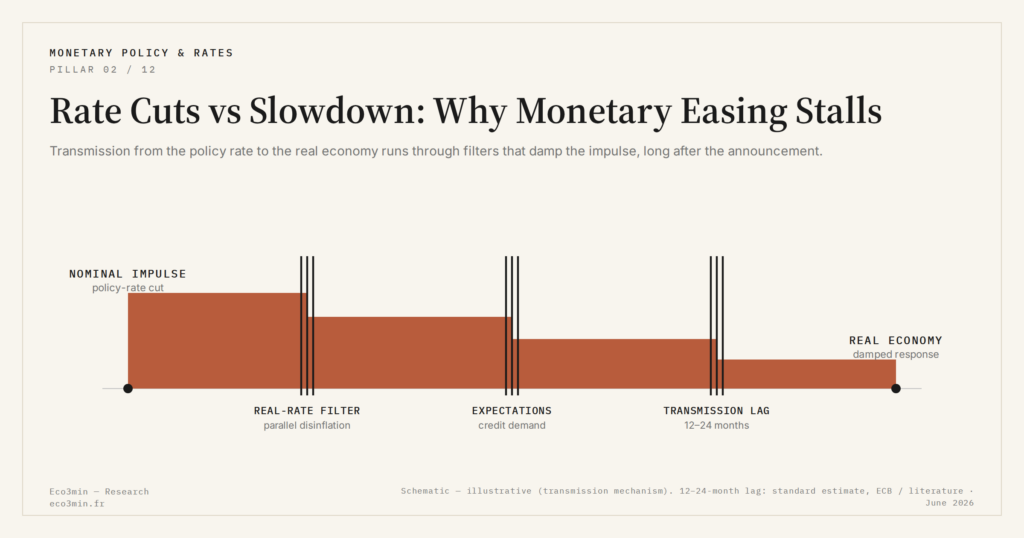

Lower nominal rates do not always revive the economy. The ECB cut by 175bp between June 2024 and January 2026 — but only ≈65bp in real terms once disinflation is factored in. The real-rate filter, expectations and structural lags all limit monetary transmission.

Cutting policy rates is the reflex move when growth slows. Yet the economy does not always respond — a paradox that dissolves once the gap between the nominal move and the effective real-rate move is taken into account.

TL;DR

The ECB cut 175 basis points between June 2024 and January 2026, yet disinflation absorbed two-thirds of the move, leaving roughly 65bp of real easing to reach the economy.

- Euro-area core inflation fell about 110bp (from roughly 3.5% to 2.4%, Eurostat) over the same window, so the 175bp nominal cut translated into only about 65bp of real easing.

- Even with banks reporting easier supply, the Fed's Q4 2025 Senior Loan Officer survey shows demand for productive-investment loans still below 2019 levels, as uncertainty compresses credit demand below the point where cuts can revive it.

- Transmission lags of 12 to 24 months mean the 2024 cuts reach full effect only in 2026, while euro-area GDP held near 0.8% annualised in Q3 2025 (Eurostat).

The friction point is not the level of rates. It is the capacity of monetary transmission to reach the real economy on a timeline compatible with the cycle that produced the cut. The core of the question is addressed in the Eco3min framework on the time lags between rate cycles and profit margins.

A rate cut does not always revive the economy. The real-rate filter, expectations and structural lags limit what nominal easing can deliver.

Between June 2024 and January 2026, the ECB cut its deposit rate by 175 basis points, from 4% to 2.75%. Over the same window, euro area GDP growth stayed modest — ≈0.8% annualised in Q3 2025 according to Eurostat. Credit to the non-financial private sector grew by only ≈1.5% year-on-year (ECB, December 2025). The gap between the size of the nominal easing and the weakness of the economic response is not an anomaly. It reveals the structural limits of monetary transmission, which everyday commentary tends to underestimate by reading the easing on its headline figure alone. Our QE-versus-rate cuts comparison reviews what the long-run data says about each.

The real-rate filter: when nominal cuts shrink in real terms

If inflation falls faster than nominal rates, the real rate can rise at the very moment the central bank announces easing. A closer look is offered in the disinflationary macro regime atlas. Between mid-2024 and end-2025, euro area core inflation moved from ≈3.5% to ≈2.4% (Eurostat) — a 110 basis-point decline. The 175 basis-point nominal cut therefore translated into roughly 65 basis points of real easing. Two-thirds of the headline gesture absorbed by the disinflation itself.

This filter explains why the real rate, not the nominal headline, drives the transmission. A diagnosis that stops at the policy-rate move misses the gap and overstates how much stimulus the economy actually receives. The same divergence shows up in the gap between curve inversion and equity performance — a reminder that the screen-level signal and the underlying real-economy variable can move in opposite directions for extended periods.

Expectations as an autonomous brake

Even when real financing conditions ease, expectations can block transmission. In periods of elevated uncertainty — geopolitical tensions, energy transition costs, supply chain reconfiguration — firms postpone investment decisions independently of credit cost. Demand for credit collapses while supply normalises. According to the channels of monetary transmission, the credit channel only operates if financing demand exists in the first place. Uncertainty compresses that demand below the point where rate cuts can revive it.

The Fed’s Senior Loan Officer Opinion Survey (Q4 2025) illustrates the pattern on the US side. Despite the Fed’s first rate cuts, demand for productive-investment loans remained below 2019 levels. Banks report easier credit supply, but demand never materialised. The block raises a broader question about the real impact of low rates on growth when uncertainty conditions dominate the firm-level decision.

- A 175 basis-point nominal cut shrinks to ≈65 basis points in real terms when inflation falls in parallel. The real-rate filter absorbs most of the visible gesture.

- Expectations act as an autonomous brake on transmission. In periods of elevated uncertainty, even favourable financing conditions fail to trigger investment because firms postpone decisions.

- Transmission lags, estimated at 12 to 24 months, imply that the 2024 cuts will reach their full effect on the real economy only in 2026.

What the gap implies for reading the cycle

The paradox of an economy that slows despite rate cuts dissolves once three elements are factored in: the real-rate filter, transmission lags, and the role of expectations. Projections that count on a mechanical rebound from nominal cuts systematically underestimate these brakes — and end up surprised when the response fails to arrive on schedule. The relevant question does not bear on the policy-rate move. It bears on the path of real financing conditions, which depend in turn on liquidity conditions during slowdowns and on the trajectory of expected inflation.

Last updated — 4 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…