How Monetary Policy Transmits Through Real Rates

Central banks set nominal rates, but the economy responds to real rates. This gap explains why identical policy moves produce divergent effects across inflation contexts, with transmission lags of 12 to 24 months.

Central banks set nominal rates, but the economy responds to real rates. This fundamental gap explains why a single policy decision can produce very different effects depending on the inflation context.

TL;DR

Monetary policy reaches the economy through the real rate agents perceive, on lags of 12 to 24 months: markets react at once, bank credit several quarters later.

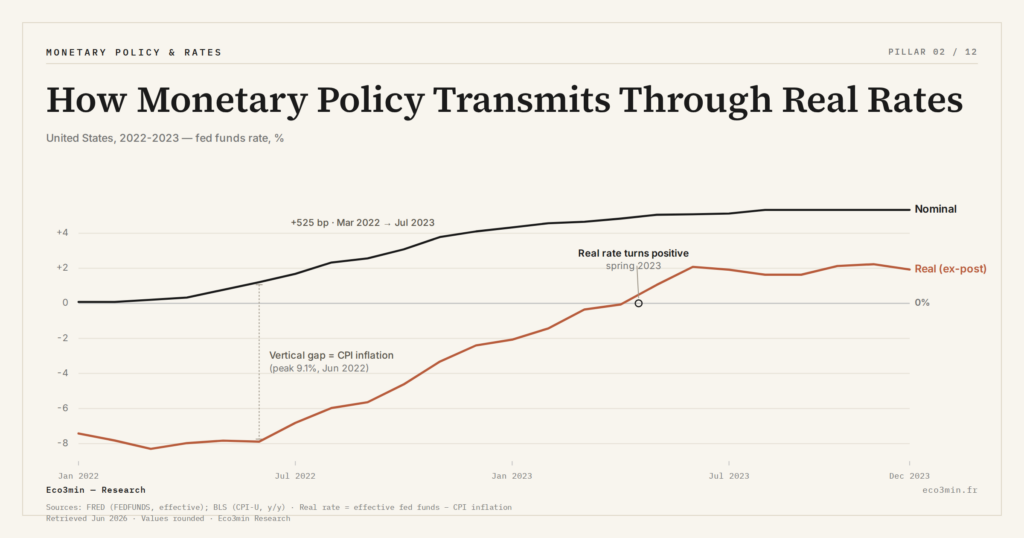

- The Fed raised its policy rate by 525 basis points between March 2022 and July 2023, yet with inflation at 9.1% in June 2022 (BLS) the real fed funds rate stayed negative until spring 2023, over a year into the cycle.

- Credit, exchange-rate and valuation channels all converge on the real rate; the ECB Bank Lending Survey (Q4 2025) shows euro-area credit standards peaked in mid-2023, roughly 12 months after the policy-rate hikes.

- Friedman's 'long and variable lags', put at 12 to 24 months in the 1960s and confirmed by the BIS (Annual Report 2024), now diverge by channel: asset valuations react faster than bank credit, leaving windows of contradictory signals.

The lags in monetary transmission and the multiplicity of channels make steering the economy through policy rates more uncertain than common commentary suggests.

Monetary policy acts on the economy through real rates, not nominal rates. Analysis of the transmission channels and their lags. This point is examined further in the time lags between tightening and earnings.

The dominant view holds that a policy rate hike ’tightens’ monetary conditions and a cut ’eases’ them. This shorthand, ubiquitous in economic commentary, obscures a decisive link: it is not the nominal rate set by the central bank that drives agents’ decisions, but the real rate they perceive — that is, the nominal rate minus expected inflation. A 50-basis-point hike can be restrictive if inflation is falling, or neutral if it accelerates. Ignoring this intermediate variable leads to systematic diagnostic errors about the actual stance of monetary policy. For the broader picture: the Eco3min frame for policy-to-earnings transmission.

Inflation as a Transmission Filter

Between March 2022 and July 2023, the Federal Reserve raised its policy rate by 525 basis points. Consensus read this move as the most aggressive tightening since the 1980s. In real terms, the trajectory is more nuanced. With inflation reaching 9.1% in June 2022 according to the Bureau of Labor Statistics, the real fed funds rate remained negative until spring 2023 — more than a year after the hiking cycle began.

This gap between nominal intent and real effect has concrete consequences. The resilience of the US economy in 2023 partly reflects the fact that real financing conditions remained accommodative far longer than nominal rates suggested. Understanding real rates as the pivot of macro analysis helps avoid this recurring confusion between nominal moves and real economic effects.

Multiple Channels, One Common Variable

Monetary policy transmits to the economy through several simultaneous channels. The credit channel affects the volume and cost of bank lending. The exchange-rate channel alters the competitiveness of exports. The valuation channel shapes the perceived wealth of households and firms through asset prices. Each of these channels converges on the same intermediate variable: the real rate perceived by economic agents.

According to the ECB Bank Lending Survey (Q4 2025), the tightening of credit standards in the euro area peaked in mid-2023, lagging the peak of policy-rate hikes by roughly 12 months. This delay illustrates the sluggishness of transmission, which operates through the gradual rollover of outstanding credit at new terms. Real credit, exchange-rate and valuation conditions together feed the cyclical dynamic emerging from real conditions, shaping the phases of expansion and contraction.

Long and Variable Lags

Milton Friedman identified as early as the 1960s the ’long and variable lags’ of monetary transmission, estimated at 12 to 24 months. Recent work by the BIS (Annual Report 2024) confirms this range while noting that transmission has grown more complex as economies have financialized. The asset-valuation channel, almost nonexistent in the 1960s, now plays a major role — and reacts faster than the traditional bank-credit channel.

This heterogeneity of lags creates windows where signals are contradictory: financial markets can react immediately to a shift in expected real rates, while bank credit adjusts only with a delay of several quarters. These transition phases explain cases where rate cuts fail to revive activity — because the various channels are not synchronized. This gap is examined in the decomposition of equity-index drivers under an inverted yield curve.

- The real rate — not the nominal rate — is the intermediate variable through which monetary policy transmits to the real economy.

- Transmission lags, estimated at 12 to 24 months, vary across channels: financial markets react immediately, bank credit with several quarters of delay.

- The real fed funds rate remained negative for more than a year after the start of the 2022 hiking cycle, materially softening the perceived tightening.

The complexity of monetary transmission — its lags, its multiple channels, its dependence on the inflation context — argues for reading policy decisions not as levers with immediate effects, but as impulses whose real trajectory depends on the liquidity and financial conditions that filter and amplify them.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…