How Real Rates Shape Long-Term Growth

Beyond cyclical fluctuations, real rates condition the pace of capital accumulation and the quality of investment — two direct determinants of potential growth in advanced economies.

Beyond cyclical fluctuations, real rates condition the pace of capital accumulation and the quality of investment — two direct determinants of potential growth.

TL;DR

Low real rates raise the volume of investment while lowering its quality; the marginal projects they make viable add little to productivity, weighing on potential growth even as capital accumulates.

- OECD multifactor productivity growth in the OECD area fell from ≈1.2% (2000–2007) to ≈0.5% (2010–2019), coinciding with the durably low-then-negative real-rate period (OECD Compendium of Productivity Indicators, 2025).

- BIS work (Annual Report 2023) finds the advanced economies with the lowest real rates between 2010 and 2020 recorded the weakest labor-productivity gains over the same span — a correlation, not established causation.

- r* is not directly observable: the Fed's Laubach-Williams model (Q4 2025) places US r* between 0.5% and 1.5%, leaving 10-year real rates near 2% in early 2026 either modestly restrictive or simply neutral.

The quantity-quality dilemma in investment, a function of the real-rate regime, sits at the heart of debates over productivity in advanced economies.

Real rates condition capital accumulation and productivity, the determinants of potential growth. The quantity-quality dilemma.

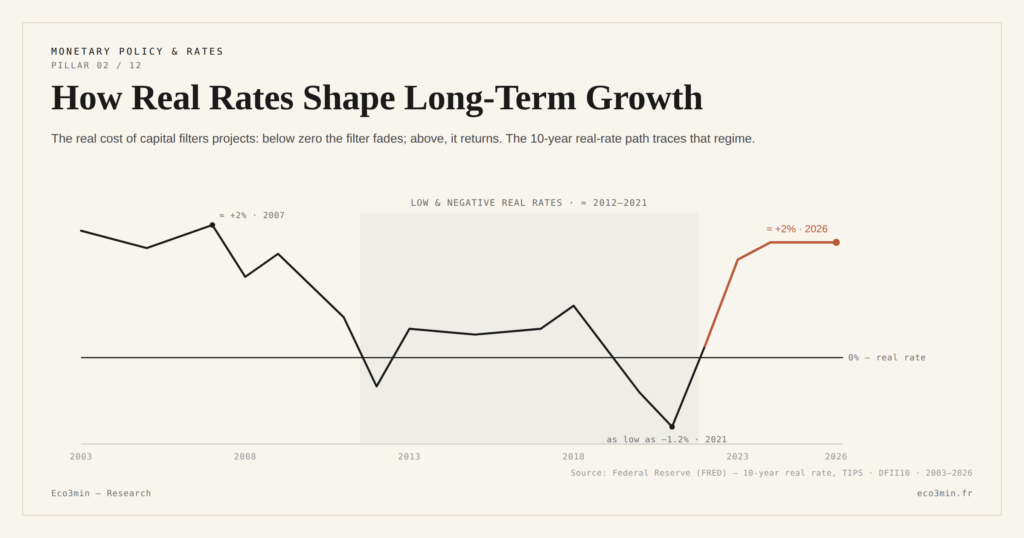

Total factor productivity in advanced economies has decelerated persistently over the past two decades. According to OECD estimates (Compendium of Productivity Indicators, 2025), annual multifactor productivity growth in the OECD area fell from ≈1.2% over 2000–2007 to ≈0.5% over 2010–2019. This inflection coincides precisely with the period of durably low and then negative real rates — a temporal overlap that invites examination of the structural link between the real-rate regime and the long-term growth trajectory. Companion analysis: The Eco3min framework on the transmission of monetary policy to company results.

The Quantity-Quality Dilemma in Investment

A low real-rate regime encourages investment by volume: the hurdle rate required to commit to a project falls, and low-return investments become viable. Capital accumulation appears to accelerate. But the added quantity comes at a cost in quality. Marginal projects financed at zero or negative real cost contribute little to productivity and tie up resources — labor, commodities, land — that could have been allocated to more productive uses.

BIS work (Annual Report 2023) shows that the advanced economies with the lowest real rates between 2010 and 2020 also recorded the weakest gains in labor productivity over the same period. This correlation does not prove direct causality, but it suggests that the selection mechanism operating through real rates — described in the analytical core on real rates — plays a role in the quality of capital accumulation.

The Equilibrium Real Rate: An Unstable Benchmark

The concept of the equilibrium real rate — r*, the rate consistent with full employment without excessive inflation — provides a theoretical benchmark for assessing whether monetary policy is restraining or supporting potential growth. If the observed real rate sits above r*, policy is restrictive and weighs on capital accumulation. If it sits below, policy stimulates accumulation — at the risk of fueling the distortions described above.

The problem is that r* is not directly observable. Federal Reserve estimates (Laubach-Williams model, Q4 2025) place r* in the United States between 0.5% and 1.5% — a range wide enough to make any clear-cut conclusion uncertain. With 10-year real rates near 2% in early 2026, monetary policy may be modestly restrictive — or simply neutral if r* has drifted higher under the influence of structural factors. These factors — demographics, energy transitions, productivity — are precisely the structural drivers behind a higher-rate regime, and they shape the path of r* and, by extension, of potential growth.

Treating low real rates as a mechanical driver of long-term growth ignores the composition effect on investment. This historical regularity is examined in our analysis of inversions accompanied by equity gains. If the volume of accumulated capital rises but its marginal productivity declines, potential growth can slow despite abundant financing. The real-rate regime acts on the quality of growth, not just its quantity.

What the Current Regime Implies for the Long-Term Trajectory

The return to mildly positive real rates — the early-2026 configuration — restores a selection mechanism that had disappeared. Investments in the energy transition and digitalization, whose expected returns are substantial, continue to attract financing. By contrast, extensive expansions with low value added — office commercial real estate, excess industrial capacity — face the filter of the real cost of capital.

If this reconfiguration continues, it could contribute to a gradual recovery in productivity across advanced economies — though the scenario is not guaranteed. Uncertainty over the level of r*, the timing of adjustments and possible supply shocks limit visibility. This structural setting fits within the long-term monetary framework that shapes resource allocation across advanced economies.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…