Why Real Rates Reshape Saving — and Sometimes Don’t

Real rates drive saving through two opposing forces — the substitution effect pulls toward more saving, the income effect shortens the road to a target. The euro area saving rate stood at ≈15.7% of disposable income in Q3 2025 even as real rates had only just turned positive.

Saving means giving up consumption today against future purchasing power. The real rate measures the reward — or, when negative, the penalty — attached to that arbitrage.

TL;DR

Higher real rates pull saving in two opposite directions: substitution rewards deferral while the income effect shortens the path to a target, so the aggregate link stays weak.

- The data refuse the simple story: the euro area saving rate held at ≈15.7% in Q3 2025 (Eurostat), above its pre-pandemic average, even as real rates had only just turned positive, and the ECB (Occasional Paper, 2024) estimates the saving-to-real-rate elasticity at just 0.1 to 0.3.

- The response tracks the balance sheet: INSEE's 2024 survey puts net wealth near €80,000 for French households under 40 against ≈€350,000 at 50-64, with younger, indebted households saving more as rates rise while wealthier ones can tilt the other way.

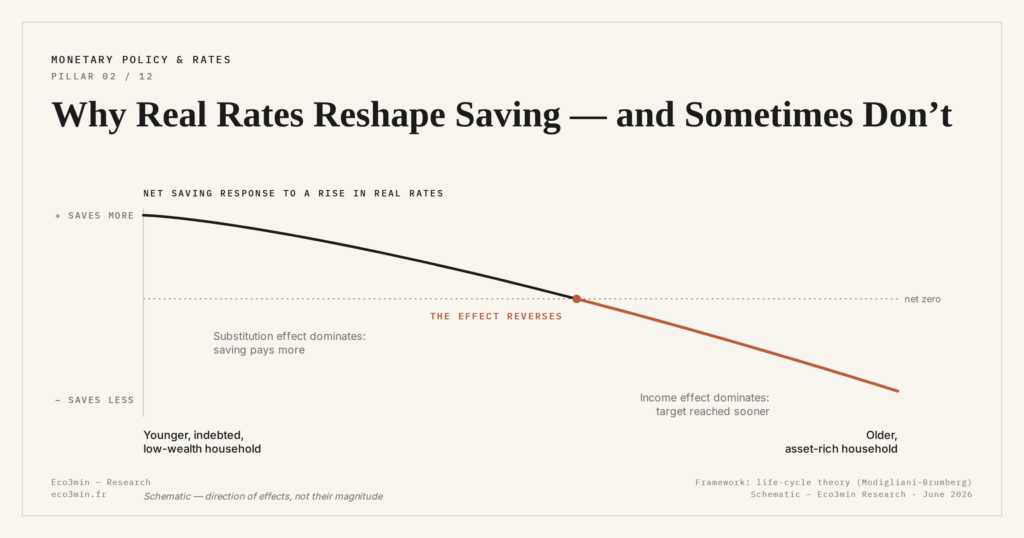

Two effects pull in opposite directions on saving behaviour: the substitution effect rewards deferred consumption, the income effect shortens the road to a target. Their net resultant is what shows up in the saving rate.

Real rates drive saving trade-offs through the substitution effect and the income effect. Analysis of a frequently misunderstood mechanism.

The intuition runs: high rates encourage saving, low rates discourage it. The data refuse to validate it. The euro area household saving rate stood at ≈15.7% of disposable income in Q3 2025 according to Eurostat — above the pre-pandemic average — even as real rates had only just turned positive after a decade of negative returns. The link between real rates and saving is not linear because two opposing mechanisms operate at the same time, and their relative weight shifts with household structure. Related discussion: our overview of how monetary policy reaches corporate earnings.

Substitution and income: two opposing forces

The substitution effect points where intuition expects it to. A higher real return raises the relative price of present consumption against future consumption: each euro saved today buys more tomorrow, which pushes households to defer purchases. This is the most direct channel through which real rates reshape intertemporal decisions.

The income effect runs the other way. A household saving toward a fixed objective — funding retirement, building a property down payment, reaching a wealth target — reaches that objective faster when real returns rise. The saving effort required per month then falls. This second effect explains why a rise in real rates does not always translate into a higher aggregate saving rate. The logic appears in the historical decoding of curve-and-index divergences. Reading real rates as a cross-cutting variable in household decisions requires integrating this ambivalence rather than wishing it away.

What the data actually show

Empirical work delivers no clean verdict. According to an ECB meta-analysis (Occasional Paper, 2024), the elasticity of saving to real interest rates in advanced economies is weakly positive, on the order of 0.1 to 0.3. The substitution effect dominates, but narrowly. The magnitude of the response varies far more with the household profile than with the rate move itself.

Younger, indebted households respond more strongly than older households with accumulated wealth. According to INSEE (Patrimoine survey, 2024), French households under 40 hold an average net wealth of ≈€80,000, against ≈€350,000 for the 50-64 age group. For the first group, higher real rates make the saving effort more rewarding and tilt the trade-off toward more saving. For the second, whose wealth appreciates mechanically with rates, the incentive can reverse. This heterogeneity explains why macro aggregates mask very different individual paths — paths that fit inside the broader framework of intertemporal trade-offs each household resolves according to its own constraints.

Assuming that high rates mechanically lift saving ignores the income effect. A household targeting €300,000 in retirement capital reaches that goal faster with real returns at 2% than at 0%. The monthly saving effort can therefore decline as rates rise — counterintuitive, but consistent with the life-cycle framework. It is precisely where that framework stops matching observed behaviour that the shortfall of measured saving against life-cycle predictions begins.

What the current regime shifts in saving flows

The move from negative to weakly positive real rates in the euro area in early 2026 has not produced a uniform rise in the saving rate. It has produced a recomposition of flows across vehicles. According to Banque de France data (Q3 2025), inflows into regulated savings have slowed, while euro-denominated life insurance products have recorded positive net inflows for the first time since 2021 — a shift consistent with the return of positive real returns on bond-based wrappers. The aggregate saving rate masks this reallocation, which is the part of the adjustment most sensitive to the liquidity environment that shapes the menu of saving vehicles available to households.

Last updated — 28 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…