T10YIE in the Fed’s Reaction Function: Anchoring Expectations and the FOMC Narrative

Since the post-COVID inflation episode, T10YIE has become a direct input to the Fed’s reaction function rather than an indicator merely observed on the side. Understanding this integration clarifies the reading of every FOMC statement since 2022.

TL;DR

The Fed treats T10YIE as a direct input to its reaction function; the ritual 'well-anchored' line in every FOMC statement since late 2021 is a live diagnosis of the breakeven.

- The doctrine predates the rhetoric: T10YIE entered Fed policy logic with Bernanke (2007) and was formalized in the January 2012 Statement on Longer-Run Goals, which fixes the 2% target on average long-term expected inflation, not the monthly CPI print.

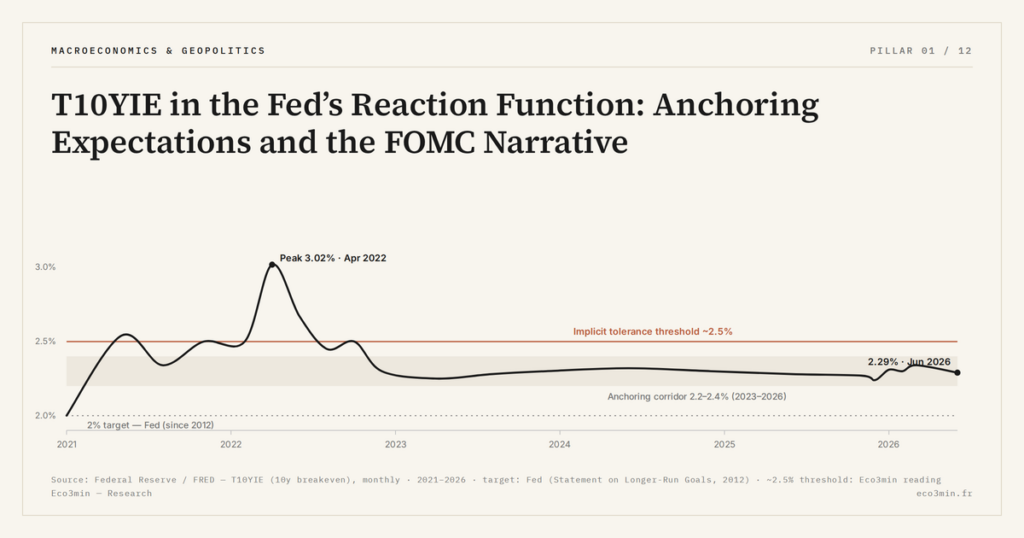

- The 2.5% breakeven level marks the implicit boundary of Fed tolerance: below it the disinflation path stays flexible, above it the tone and the action tighten explicitly.

- The dot plot tracks the signal: when T10YIE drifts above 2.5% between two quarterly SEPs, the median Fed funds dots typically shift up 25 to 50 basis points in the next one.

- The credibility loop runs both ways, with communication acting before rate moves, but Jeremy Stein flags its circularity: markets price Fed decisions into T10YIE while the Fed reads T10YIE to decide.

This article describes the mechanics of Fed usage of T10YIE: the ritual “well-anchored” phrase, articulation with the dot plot, the credibility loop. For the full breakdown, see the 10-year reference expectation measure.

1. The official role of inflation expectations in the Fed reaction function

The Fed’s modern doctrine on inflation expectations is documented at least since Ben Bernanke (2007, Constraints on the Conduct of Monetary Policy). The principle is explicit: the 2% target’s credibility is measured first by the stability of long-term expectations. If those expectations drift durably above target, the Fed must tighten further, hold longer, and accept a higher economic cost. If they remain anchored, the Fed can tolerate a temporary overshoot of realized inflation without revisiting its reaction function.

This principle was formalized in the Statement on Longer-Run Goals adopted in January 2012, which sets the 2% target and explicitly states that the objective is average long-term anticipated inflation, not monthly realized inflation. The nuance is not anecdotal: it legitimizes the use of expectations indicators like T10YIE in conducting policy, rather than a mechanical reaction to the latest CPI print.

In practice, the contemporary Fed reaction function integrates four main arguments: the gap of core PCE inflation to the 2% target, the unemployment gap to the natural rate (NAIRU), global financial conditions, and long-term inflation expectations. The fourth argument is where T10YIE enters directly as an observable variable. Other expectations measures — the Survey of Professional Forecasters, Michigan, inflation swaps — complement the reading, but T10YIE remains the central instrument by its daily frequency and its construction transparency.

The doctrinal framing has a major practical consequence: the Fed explicitly accepts asymmetric reasoning. A moderate and temporary overshoot of the 2% target is tolerable as long as expectations remain anchored; a de-anchoring of expectations, even without a current overshoot of the target, requires a reaction. This reaction asymmetry explains why the Fed can alternate phases of patience and phases of urgency depending on T10YIE’s evolution, without changing its official doctrine.

2. The “well-anchored” phrase in 2022-2026 FOMC statements

Since late 2021, Jerome Powell has systematically included in every FOMC communiqué a formula now ritualized: “longer-term inflation expectations remain well-anchored.” This sentence is not neutral boilerplate: it publicly states the condition of T10YIE and other measures, and signals to markets that the Fed adjusts its reaction function on this reading. The history of FOMC statements since November 2021 shows the formula has been maintained at every meeting, including during the April 2022 spike — the Fed’s interpretation being that even a T10YIE at 2.99% still sat in the anchoring zone.

A close examination of the statements reveals subtle variations in the formulation that are themselves signals to markets. The standard version “longer-term inflation expectations remain well-anchored” indicates status quo. When Powell adds “as indicated by a broad range of surveys and market-based measures,” he signals that he references not only T10YIE but also household and professional surveys — typically to reassure when T10YIE alone drifts slightly. When Powell temporarily omits the formula — as in March 2022, when it was replaced by a more cautious wording — that signals a concern which will translate into action tightening. Related analysis: how inflation regimes shape markets.

Several Board members have made explicit in individual speeches their reading of T10YIE. Loretta Mester (Cleveland Fed, November 2022) explicitly cited the 10-year breakeven as a calibration parameter for her own Fed funds expectations. John Williams (New York Fed, February 2023) discussed T10YIE in comparison with SPF and Michigan in a speech on decomposing the expectations signal. Christopher Waller (Board of Governors, March 2024) explicitly linked the expected tightening pace to breakeven dynamics, within an explicit reaction-function logic. For the empirical context of these interventions, see the 2022 episode as a reaction-function test.

3. T10YIE as input to the Summary of Economic Projections

The Summary of Economic Projections (SEP), published quarterly by the Fed, contains individual FOMC member projections for core PCE inflation, unemployment, growth, and Fed funds rate at various horizons. Although the SEP does not explicitly mention T10YIE as input, FOMC members regularly reference the breakeven in individual communications to explain the calibration of their own projections. The mechanism is implicit but documented: T10YIE weighs in the construction of quarterly dot plots.

The empirical correspondence between T10YIE level and median dot shifts is measurable. When T10YIE drifts significantly above 2.5% between two SEPs, the median dots of Fed funds at 1 and 2 years move upward in the following SEP, generally by 25 to 50 basis points. This correspondence is not mechanical — it also depends on realized CPI, financial conditions, and FOMC communication — but it is systematic enough that macro strategy desks treat it as a reliable heuristic.

Another dimension of the T10YIE / SEP link concerns the longer-run projection. The SEP publishes a “longer run” projection for core PCE inflation, fixed at 2% since 2012 and unchanged since. If T10YIE were to drift durably more than 50 basis points above, the Fed would face pressure to revise that longer-run projection — not mechanically, but in a logic of internal consistency between market reading and official doctrine. To date (Q1 2026), no such revision has occurred despite T10YIE structurally between 2.2% and 2.4% since 2023, which opens the reading already discussed of current anchoring and 2024-2026 FOMC narrative.

One last empirical dimension: the inter-member dispersion in the dot plot itself carries information about the FOMC’s reading of T10YIE. When the dispersion widens — typically when the breakeven enters a zone of uncertainty — it signals internal disagreement on the reaction trajectory. In 2022, dispersion reached its highest level since 2015, reflecting divergences on the pace needed to quickly re-anchor T10YIE. The return to tighter dispersion from 2023 onward coincided with the breakeven’s stabilization in its current corridor.

A further institutional point is worth noting: T10YIE figures regularly in the staff memos prepared for FOMC meetings, available in the released transcripts with the standard five-year lag. The transcripts of the 2018-2020 meetings, released publicly in 2024-2026, show that staff systematically presented T10YIE alongside SPF and TIPS-implied curves as part of the standard expectations dashboard. This institutional embedding precedes the post-COVID rhetoric and confirms that the explicit “well-anchored” language was a public-facing crystallization of a practice already mature internally. The implication for analysts: changes in Powell’s phrasing typically reflect an internal staff diagnosis that predates the public statement by one or two meetings.

4. The credibility loop: communication acting on what it describes

When Powell qualifies T10YIE as “well-anchored,” he does not merely describe a state: he acts on that state. Public declaration of anchoring by the central bank mechanically reinforces anchoring by signaling to markets that the Fed remains ready to tighten if the breakeven drifts. This mechanism, sometimes called the credibility loop, is one of the foundations of modern monetary policy and constitutes the main channel by which communication substitutes for actual action in many situations.

The loop works in both directions. When T10YIE drifts, Powell hardens the tone in the FOMC statement, which re-anchors expectations without necessarily going through an immediate rate hike. When T10YIE re-anchors, Powell can soften communication, which stabilizes financial conditions without cutting rates. This double mechanism gives the Fed considerable tactical room — communication acts before action, which reduces the economic cost of transition phases.

A recurring critique of this loop comes from Jeremy Stein (Harvard, former Board of Governors). Stein points out that the system risks circularity: markets embed Fed decisions in T10YIE, the Fed reads T10YIE to decide, and the loop can produce oscillations that do not reflect the underlying evolution of expectations. This critique is the central argument for never treating T10YIE as a single decision variable but as one input among others in the reaction function.

A final dimension concerns the practical asymmetry. The Fed reacts swiftly to an overshoot above the 2.5% threshold — as the 2022 episode demonstrated — but with more patience when the breakeven falls below 2%, as in 2014-2016 and 2019-2020. This asymmetry reflects an implicit central-bank preference for combating an inflation risk — which erodes purchasing power and destabilizes nominal contracts — over a deflation risk that can be countered by unconventional tools. This preference is documented in the academic work of Janet Yellen during her Fed Chair tenure.

- T10YIE has been a direct input to the Fed’s reaction function since Bernanke (2007) and was formally integrated in the 2012 Statement on Longer-Run Goals.

- The ritual phrase “longer-term inflation expectations remain well-anchored” in every FOMC statement is an operational diagnosis of T10YIE, not neutral boilerplate.

- The 2.5% threshold constitutes the implicit boundary of Fed tolerance. Below: flexibility in the disinflation path. Above: explicit tightening of tone and action.

- The credibility loop works in both directions — communication acts before action — but exposes the Fed to the circularity risk documented by Stein.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Monetary Tightening: How Central Banks Are Reshaping Financial Markets

After more than a decade of ultra-accommodative policy, monetary tightening has reintroduced the real cost of capital as…

Hidden Unemployment: Reading the Real Labor Market in 2026

Headline unemployment is stabilizing while broad underemployment still runs above pre-2020 levels. Reading the gap between official rates…

2026 Economic Outlook: Key Trade-Offs After the End of Cheap Money

2026 ushers in a more constrained macro regime where real rates stay positive, fiscal space narrows and geoeconomic…