T10YIE in 2024-2026: Reading the Post-Cycle Anchoring Regime

Since late 2022, T10YIE has been trading in a narrow 2.2-2.4% corridor. Powell labels this zone well-anchored, yet it sits structurally above the Fed’s 2% target. Three competing readings illuminate this gap without resolving it.

TL;DR

T10YIE's stability near 2.28% since 2023 fits three incompatible stories about the 2% gap, each implying a different Fed stance: residual risk premium, shifted anchor, or wider TIPS liquidity premium.

- First reading (Powell's implicit view): the ACM decomposition splits T10YIE into pure expectations near 2.0-2.1% and an inflation risk premium of 25-40 bps set to erode over 5-10 years.

- Second reading: a tacit anchor shift, with US deficits at 6-7% of GDP since 2023 versus a 3% average over 2003-2019, plus asymmetric Fed communication.

- Third reading: a technical bias, the inflation-swap/T10YIE spread holding 40-55 bps since 2022 against 15-30 bps in 2003-2019.

- Short-term evidence leans to the second reading, though all three are likely partially true with shifting weights into 2027-2030.

This article exposes the three hypotheses competing to interpret the current regime: genuine anchoring, tacit re-anchoring at a higher level, or durable widening of the liquidity premium. For the wider context, see T10YIE and regime-based reading.

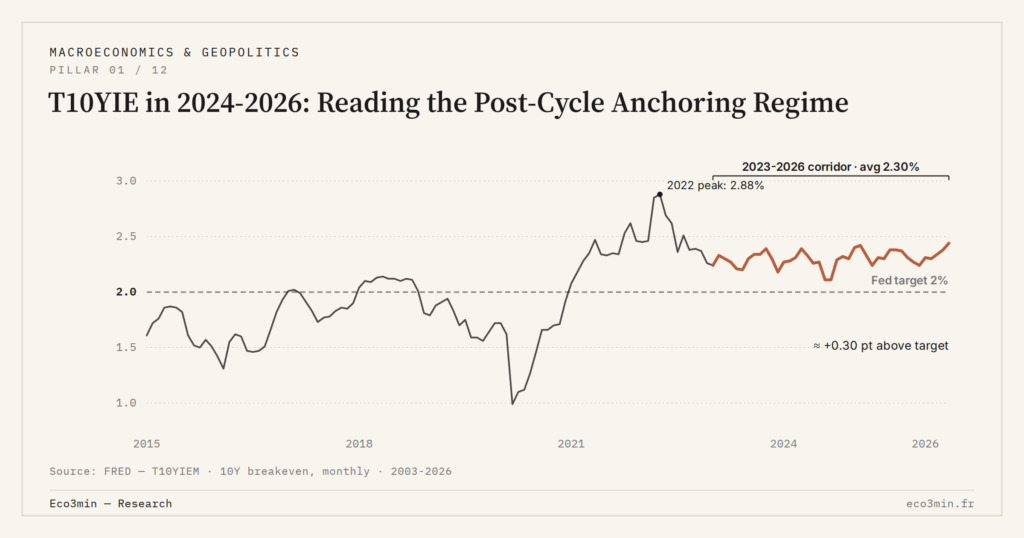

1. The 2.2-2.4% corridor: empirical description of the current regime

After the April 2022 peak at 2.99%, T10YIE progressively retreated below 2.5% by mid-August 2022, then continued to decelerate to 2.21% by end-December 2022. This is set in context in the ongoing macro cycle framework. Since early 2023, the breakeven has been trading in a narrow band — between 2.15% and 2.42% according to FRED monthly data — around a 2.28% average. This statistical stability is remarkable: over 39 months of observation (January 2023 to May 2026), the standard deviation of monthly averages stands at only 0.07 percentage points, against 0.38 over the full 2003-2025 sample.

This volatility compression is an analytical fact in itself. It suggests that bond arbitrageurs consider 10-year inflation expectations as stabilized — without however converging toward the Fed’s 2% target. The full picture is drawn in how anchoring shapes price perception. This dimension echoes the 2022 episode this regime inherits from: the return to anchoring succeeded on stability but not entirely on the originally targeted level.

Examination of complementary data sharpens the reading. The Philadelphia Fed Survey of Professional Forecasters showed, at Q1 2026, a median expected 10-year CPI inflation of 2.40% — in the upper end of the T10YIE corridor. The University of Michigan survey showed 3.1% over 5-10 years for the same period, a markedly higher figure but consistent with the documented behavioral biases of household surveys. The 10-year inflation swap spread against T10YIE — a proxy for the TIPS liquidity premium — oscillates in 2024-2026 around 40 to 50 basis points, the upper end of its historical range. A closer look: the copper/gold ratio as a growth-versus-fear gauge.

This triangulation of measures allows posing the central problem: if the Fed target is 2% and if T10YIE oscillates at 2.28% on average, that is 28 basis points above, how should this gap be characterized? Three competing interpretations are available to the analysis, with opposite monetary-policy implications.

A preliminary methodological note: corridor stability is in no way an argument in favor of any particular reading among the three proposed. Volatility compression is compatible with genuine anchoring, with a new tacitly accepted equilibrium point, and with a durably higher liquidity premium. To arbitrate between the three hypotheses, one must examine the underlying structures, not the raw breakeven statistics alone. This is precisely what the following three sections propose to do.

The first reading interprets the 2.2-2.4% corridor as genuine anchoring, where true expectations are stabilized at 2% but a residual inflation risk premium of 20 to 40 basis points is added. This premium would compensate for the memory of the 2021-2022 shock and the residual possibility of another shock — without any change in the deep structure of expectations.

This reading is defended by a majority of Federal Reserve Board economists and constitutes Jerome Powell’s implicit public position. It rests on the ACM factor decomposition (Adrian, Crump, Moench) that isolates a pure expectations component around 2.0-2.1% and an inflation risk premium around 25-40 basis points for the 2024-2026 period. The internal consistency of this decomposition with the 2.40% SPF reinforces its credibility — the SPF itself implicitly embeds a comparable inflation risk premium.

One implication of this reading is that the Fed can, over time, normalize its policy by accepting a T10YIE durably above 2% without considering it an anchoring failure. The inflation risk premium should erode progressively as the temporal distance from the 2022 shock grows — a mean reversion typically spread over 5 to 10 years according to academic literature. Under this reading, the 2024-2026 corridor reflects a post-shock healing phase rather than a structural change.

The central empirical argument of this reading comes from historical comparison. After inflation-pressure episodes, 10-year expectations retrospectively estimated by the Cleveland Fed typically take 3 to 5 years to return to the initial level. The 2022-2026 delay is consistent with this progressive re-anchoring mechanism, without requiring a stronger hypothesis on a structural change.

3. Second reading: tacit re-anchoring at a slightly higher level

The second reading is intellectually more demanding. It considers that the market has tacitly shifted its expectations anchor toward 2.2-2.3%, consistent with a new post-pandemic macroeconomic equilibrium. The official Fed target remains at 2%, but the market no longer fully believes it and prices a slightly higher equilibrium. This would be a discreet but real credibility failure of the target.

Three structural arguments support this reading. First argument: the partial deglobalization observed since 2022, with US industrial relocation, supply-chain fragmentation, and structurally more volatile energy costs, exerts persistent upward pressure on production costs. This dimension is documented by the literature on the inflationary consequences of dismantling efficient globalization.

Second argument: US fiscal policy remains structurally more generous than pre-pandemic. The US federal deficit has oscillated between 6% and 7% of GDP since 2023, against a 3% average over 2003-2019 according to the OMB. This fiscal dimension exerts persistent nominal pressure that partially erodes pure monetary credibility. For the theoretical framework, see the analysis of structural inflation regimes.

Third argument: Fed communication itself does not react symmetrically. If T10YIE were at 1.7% since 2023, Powell would probably harden the tone to bring the breakeven back toward 2%. But with T10YIE at 2.3%, the “well-anchored” formula is maintained without downward pressure — as if the Fed were implicitly accepting the anchor shift. This asymmetry is documented in the FOMC narrative on anchoring and constitutes the strongest indirect signal of the second reading.

The third reading is technically the most demanding and the least publicly discussed. It considers that T10YIE embeds a structurally higher TIPS liquidity premium since 2022, without any real change in underlying expectations. Under this reading, true expectations would remain around 2% but the raw T10YIE reading would be biased upward by technical factors related to the inflation-linked bond market.

The central empirical argument comes from the spread between 10-year inflation swap and T10YIE — already mentioned as a direct proxy for the TIPS liquidity premium. This spread (Asset Swap, ASW) historically stood around 15 to 30 basis points during the 2003-2019 phase. Since 2022, it has oscillated between 40 and 55 basis points, a structural widening of 15 to 25 basis points. If this widening is durable, it mechanically explains part of the gap between raw T10YIE and the Fed target. More on this: our reading of inflation regime by regime.

Several structural factors can explain this durable widening. First factor: post-COVID prudential regulation has reduced dealers’ ability to carry TIPS inventory, mechanically widening the liquidity premium. Second factor: the composition of TIPS holders has shifted — pension funds and life insurers represent a growing share against hedge funds, which reduces active arbitrage. Third factor: the Fed QE program on TIPS, active between 2020 and 2022, temporarily distorted pricing and normalization may not be complete.

This third reading has important practical implications for the Fed. If it is accurate, raw T10YIE overstates the anchoring problem and the Fed can maintain a less restrictive stance without genuine de-anchoring risk. To empirically distinguish the three readings, the analyst must simultaneously track the raw breakeven, the SPF, the Michigan, and the ASW spread — triangulation alone allows arbitration. This divergence between measures is the subject of dedicated analysis in the current gap with realized inflation.

Arbitration between the three readings is not time-invariant: it is likely that they are simultaneously partially true, with relative weights that evolve. In the short term (2024-2026), empirical indices converge more toward the second reading — structurally elevated deficits, supply-chain fragmentation, asymmetric Fed communication — without excluding a contribution of durably widened liquidity premium. In the medium term (2027-2030), the return toward the 2% target will depend as much on the US fiscal trajectory as on the evolution of TIPS liquidity, two variables that are not in the direct perimeter of monetary policy and which make the horizon more uncertain than the current corridor stability suggests.

A final note for the analyst: the three-reading framework is itself an analytical tool, not a definitive map of reality. Future macro data will progressively constrain which combination of readings is most consistent with the observed trajectory of T10YIE, the SPF, Michigan, and the ASW spread. Maintaining the three readings as live working hypotheses, rather than collapsing them prematurely into a single interpretation, is the practical methodology that allows updating the regime assessment as new information arrives — a discipline particularly valuable in regimes where stability conceals structural questions that data alone cannot answer rapidly.

Reading Powell’s “well-anchored” formula as synonymous with “at the 2% target.” The T10YIE 2.2-2.4% corridor is technically anchored in the sense of the Fed reaction function — it stays below the 2.5% tolerance threshold — but it sits structurally 20 to 40 basis points above the target. Conflating the two levels misses the central editorial question of the 2024-2026 regime: genuine anchoring, tacit re-anchoring, or durable liquidity premium?

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Monetary Tightening: How Central Banks Are Reshaping Financial Markets

After more than a decade of ultra-accommodative policy, monetary tightening has reintroduced the real cost of capital as…

Hidden Unemployment: Reading the Real Labor Market in 2026

Headline unemployment is stabilizing while broad underemployment still runs above pre-2020 levels. Reading the gap between official rates…

2026 Economic Outlook: Key Trade-Offs After the End of Cheap Money

2026 ushers in a more constrained macro regime where real rates stay positive, fiscal space narrows and geoeconomic…