The yen 2022-2024: losing currency control without a crisis

From 2022 to 2024, the yen fell about 27% against the dollar and hit its weakest level since 1990 — without triggering a single classic currency-crisis signal.

TL;DR

Between 2022 and 2024 the yen lost about 27% against the dollar to its weakest since 1990, yet no currency-crisis signal (CDS, capital flight, sovereign premia) ever fired. Related framing: the euro below parity in 2022.

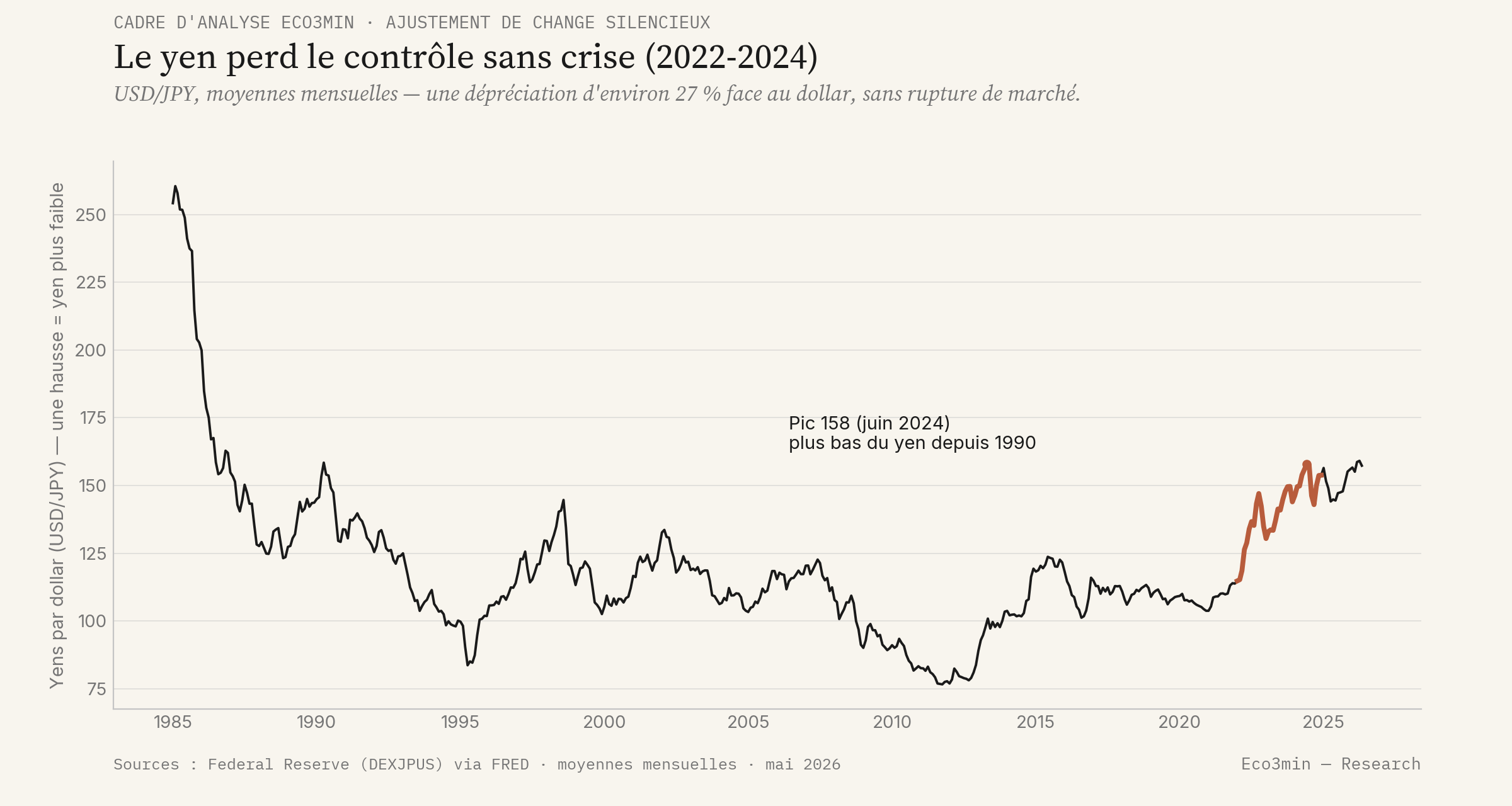

- USD/JPY climbed from 114.8 in early 2022 to a monthly peak of 157.9 in June 2024, around 162 intraday, the yen's weakest against the dollar since April 1990 (FRED, DEXJPUS).

- Bilateral and real-effective are two distinct measures: against the dollar the yen fell about 27%, while on a trade-weighted, inflation-adjusted basis it fell more sharply, the BIS recording multi-decade lows.

- The Bank of Japan kept nominal command, capping its 10-year yield until yield-curve control ended in 2024, while losing real grip as the policy gap with an aggressively tightening Fed fueled the carry trade (IMF 'orderly adjustment').

Some currencies undergo a prolonged erosion of value without ever activating the usual mechanisms of a currency crisis: no panic, no sudden capital flight, no surge in sovereign premia. Volatility stays contained, spreads stay calm — and yet, quarter after quarter, the exchange rate slides. This is one of the four silent adjustment regimes Eco3min documents: the correction is not suppressed, it is spread out over time.

The Japanese yen between early 2022 and mid-2024 provides the clearest illustration. The question is therefore not to explain a collapse — it does not happen — but to understand by which mechanism a central bank can keep its full institutional legibility while losing, in practice, real grip on the trajectory of its currency.

The observable fact — the yen, 2022-2024

USD/JPY rises from 114.8 in early 2022 (103.8 in early 2021) to a monthly peak of 157.9 in June 2024 — around 162 intraday — a yen depreciation of about 27% against the dollar over the period (≈34% measured from early 2021). At that peak, the yen reaches its weakest level against the dollar since April 1990. The full series is available in the dataset USD/JPY exchange rate (1971–2026).

Through this sequence, stress signals stay absent: Japanese sovereign CDS do not widen, capital-flight indicators do not trigger, market volatility stays measured. The Japanese authorities’ FX interventions (autumn 2022, then 2024) are calibrated and occasional, not emergency measures against a panic. The Bank of Japan also retains nominal control of its curve — the 10-year sovereign yield stays capped until the dismantling of yield-curve control in 2024 (see Japan 10-year sovereign yield). A parallel read: the Eco3min study of systemic risk indicators and financial market stress signals.

Two distinct measures coexist and must not be confused. The bilateral USD/JPY rate measures the yen against the dollar alone (≈−27% over 2022-2024). The real effective exchange rate (REER) measures it against a basket of trade partners, adjusted for inflation differentials: on that basis, the BIS documents an even sharper depreciation, with the real effective yen hitting multi-decade lows. Both tell the same weakening story, but at different magnitudes — citing one while attributing it to the other is a common error.

Why no crisis broke out

A classic currency crisis presupposes a rupture: a concentrated speculative attack, exhaustion of reserves, an external financing default, an abrupt widening of risk premia. Nothing of the sort here. Japan retains its status as a net external creditor, durable demand for its domestic debt, and intact institutional credibility. The weakening is integrated into quotes in successive touches rather than in jolts.

This is precisely the condition of the phenomenon: a gradual loss of control can only develop when market attention relaxes. As long as volatility stays low and moves are read as transitory, the currency drift is absorbed without coordinated reaction. The absence of turbulence is not a guarantee of soundness — signals deemed reassuring can coexist with a persistent imbalance, a bias examined in the study of misleading market signals.

The mechanism: policy divergence and real rates

The engine of the episode is the monetary-policy gap. While the Federal Reserve aggressively raises rates to curb inflation, the Bank of Japan keeps an ultra-accommodative stance and caps its long yields. The resulting real-yield gap makes the yen structurally less attractive and fuels the carry trade. The role of the real cost of capital in this kind of arbitrage is developed in the analysis of real policy rates; the dollar-cycle context reads via the trade-weighted dollar index (DTWEXBGS).

The central bank then retains nominal command — it steers its policy rates, frames its curve — while losing real command of the effective exchange rate, once growth, productivity and balance gaps widen against partners. The exchange rate stops working as a warning signal and becomes an adjustment variable: it silently absorbs imbalances that domestic policies have not addressed. The IMF labels this kind of gradual correction an orderly adjustment and documents it in its External Sector Reports (External Balance Assessment framework).

What the case reveals about how markets work

The absence of crisis does not mean the absence of imbalance. Markets can integrate a major adjustment gradually, with no visible jolt — that is the dominant mode, not the exception. As long as global liquidity stays abundant and flows do not turn abruptly, external discipline is not suppressed: it is deferred and diluted over time. The market sanction still exists, but spread out.

This reading belongs to the macro-financial grid developed by the pillar page financial markets, and echoes the case of a durable strong dollar without a visible crisis: the same no-rupture logic is observed at the level of the pivot currency itself — proof that the pattern is not the preserve of secondary currencies. The dollar’s own trajectory is tracked in the US dollar & global crises dataset.

A central bank can preserve its institutional credibility while losing real grip on its currency. The absence of volatility is not a reliable indicator of soundness: the exchange rate works as a silent shock absorber for macro-financial imbalances.

Scope, limits and condition of invalidation

The case authorizes no prediction: it provides neither a timetable for reversal, nor a critical threshold, nor an anticipation of the authorities’ reaction. It offers a grid to distinguish a cyclical shock from a structural drift. This equilibrium — loss of control without crisis — rests on two conditions: abundant global liquidity and capital flows that do not dry up abruptly. It is invalidated if the adjustment ceases to be orderly: an abrupt reversal of flows, an attack on financing, or a loss of institutional credibility that would turn the silent drift into an open crisis. Read alongside: our study on foreign exchange markets and international monetary regimes.

A prolonged currency depreciation without crisis signals a regime where the exchange rate silently absorbs imbalances that domestic policies have not addressed. The central bank keeps nominal command, not real command.

- From 2022 to 2024 the yen lost ≈27% against the dollar (weakest since 1990) without a currency crisis.

- The bilateral rate and the real effective rate are two distinct measures: do not attribute the magnitude of one to the other.

- A central bank can retain nominal command (rates, curve) while losing real grip on its currency.

- The exchange rate works as a shock absorber: the market sanction is not suppressed, it is spread out over time.

Data and further reading

Overall framework: the silent adjustment regimes (regime 3). Data series: USD/JPY, Japan 10-year sovereign yield, trade-weighted dollar index, US real interest rates. All proprietary macro-financial data (CSV/XLSX): Data & research hub.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Eurozone Fragmentation: Sovereign Spreads and the Euro

The euro is issued by a monetary union without a complete fiscal union: nineteen sovereign debts coexist under…

The Euro’s Energy Import Bill: the Gas Shock and the Currency

In 2022, the surge in gas prices turned the euro area's historic current-account surplus into a deficit and…

The ECB-Fed Rate Differential: the Driver of EUR/USD

The rate differential between the ECB and the Fed is the first-order driver of EUR/USD. But it is…