Silent adjustment regimes: markets price the absence of crisis

Markets price the absence of catastrophe, not the quality of capital allocation. As long as no rupture is visible, an economy or an asset class can accumulate inefficiency without triggering any correction — and it is precisely this absence of signal that makes the phenomenon so hard to read.

TL;DR

Eco3min groups four macro-financial configurations where imbalances accumulate and get priced in gradually, linked by one variable: the real cost of capital, whose level matters more than its nominal path.

- Four configurations share the pattern: zombie firms kept alive by framework stability (BIS, Banerjee and Hofmann 2018), monetary policy that buys time without reviving investment, a currency that silently absorbs imbalances, and management tools that synchronize behavior into procyclicality.

- The thread is the real cost of capital, nominal rates adjusted for inflation: when it stays durably binding, long-horizon projects lose attractiveness and investment retreats toward conservative uses, whatever the headline rate level.

- The signature is calm indicators while fragility builds: risk premia that do not widen, a financial conditions index (NFCI) that does not tighten, high-yield credit spreads that hold, until a shock reveals the accumulated scale.

- The grid offers no timetable, threshold or crisis prediction; the reading lapses only when a structural shock restores a corrective pull, or when the real cost of capital recedes durably and selection mechanisms regain their power.

This page gathers a family of macro-financial configurations that share one property: the system keeps its appearance of robustness while its performance mechanisms quietly erode. The risk here is never event-driven — it is cumulative, diffuse, and stays invisible in conventional aggregates until a shock reveals its scale.

The central question is therefore not to explain a crisis — it does not happen — but to understand by which mechanism markets can operate durably in a sub-optimal regime without exerting any corrective pull. The answer lies in a widespread confusion: equating the persistence of the framework (institutional, monetary, regulatory) with the soundness of the decisions taken within it. A broader view: our analysis of monetary transmission to corporate earnings.

OECD work on productivity, the Bank for International Settlements’ annual reports on capital allocation, and the IMF’s Global Financial Stability Reports have documented since the mid-2010s this coexistence of surface stability and cumulative erosion of efficiency — in connection with the debates on the “zombification” of advanced economies and secular stagnation.

Eco3min groups under the term silent adjustment regime any configuration where an imbalance is absorbed or accumulates gradually, priced in, without an identifiable crisis episode. This grid does not rename existing mechanisms: it classifies them and links each to its reference literature (BIS, IMF, FSB). Four main forms are distinguished below.

Stability is not optimality

Several developed economies have been going through, since the middle of the previous decade, a phase of paradoxical continuity: the institutional architecture holds, alliances endure, no systemic shock rattles the edifice — and beneath that façade, indicators of productive vitality weaken. Productivity gains shrink, innovation struggles to irrigate the productive fabric, capital is deployed along increasingly conservative lines.

The dominant narrative reads this continuity as proof of resilience. Avoiding recession, the orderly decline of inflation and the absorption of geopolitical tensions are brandished as so many demonstrations of structural robustness. The reasoning conflates two distinct things: that a framework holds says nothing about the quality of the trade-offs made within it. An economy can combine strategic solidity with mediocre capital allocation — the former does not buy the latter. This divergence between political and economic equilibria over long horizons belongs to the grid of the pillar page Macro-financial regimes.

This reading bias — interpreting reassuring aggregate signals as a guarantee of structural health — is examined in detail in the study of misleading market signals. The stability of risk premia, in particular, is regularly mistaken for a signal of optimality, when it often reflects nothing more than the absence of anticipated rupture.

The silent variable: the cost of capital

The thread linking these regimes is the real cost of capital. When real interest rates — nominal rates adjusted for inflation — remain durably binding, even at moderate levels, long-horizon projects mechanically lose attractiveness. Investment retreats toward conservative uses, at the expense of innovation and future productivity. The mechanism is developed in the analysis of real policy rates; the long series is documented in the dataset US real interest rates (1962–2026).

What matters is not the headline level of rates, but their real incidence on financing conditions. A cyclical improvement — disinflation, positive growth — does not automatically translate into financial easing: as long as the real cost of capital stays high, long-duration assets remain under pressure. This divergence reads by comparing macro aggregates with the system’s effective liquidity, tracked by the net liquidity index.

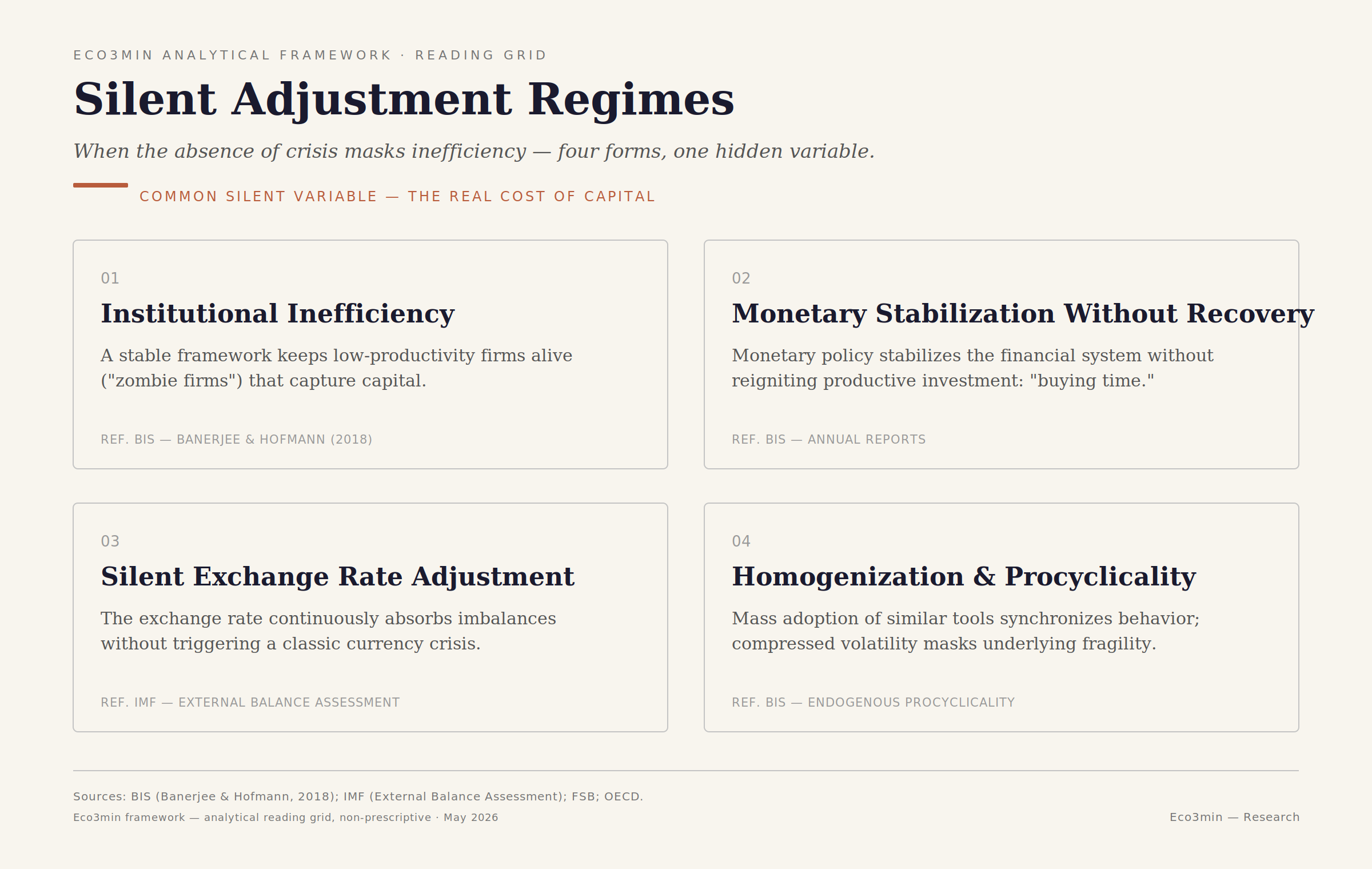

Four silent adjustment regimes

The same logic plays out across four distinct fields. In each, a mechanism of selection or sanction weakens without disappearing: the correction is not suppressed, it is spread out over time.

1. Prolonged institutional inefficiency

The stability of the framework keeps low-productivity firms in business — the “zombie firms” in the BIS terminology (Banerjee and Hofmann, 2018) — which capture resources at the expense of more dynamic players and drag down aggregate productivity gains. Institutional anchoring reduces the pressure to adjust and freezes trade-offs, at the cost of a gradual erosion of efficiency.

2. Monetary stabilization without revival

Monetary policy can succeed in stabilizing the financial system while failing to restart a cycle of productive investment: authorities “buy time” without resolving the underlying imbalances (debt, declining potential growth). The implicit benchmark ceases to be potential growth and becomes the absence of catastrophe — a perspective developed by the pillar monetary policy and rates.

3. Silent exchange-rate adjustment

A currency can weaken durably without triggering the classic mechanisms of a currency crisis — the exchange rate taking on the role of adjustment variable, absorbing imbalances that domestic policies have not addressed (the IMF’s orderly adjustment framing, External Balance Assessment). The case is studied in detail in Central bank and loss of currency control without a visible crisis, from the series USD/JPY (1971–2026) and Japan 10-year sovereign yield.

4. Homogenization and procyclicality

The mass adoption of similar management tools synchronizes behavior: the prolonged compression of volatility masks an accumulation of vulnerabilities, which are released in a synchronized way when conditions turn — the BIS’s “endogenous procyclicality.” This mechanism is covered in Financial innovation and the rigidification of market behavior; volatility dynamics are tracked via the VIX index (1990–2026).

A fifth variant, at the edge of this grid, concerns stabilization through regulation: a diffuse regulatory framework reduces systemic uncertainty and filters out the most fragile actors without a visible shock (reduction of cliff effects, FSB). It is documented for crypto-assets in Regulation and implicit stabilization of crypto-assets.

- Mistaking the absence of crisis for economic efficiency.

- Reading the stability of risk premia as a signal of optimality.

- Confusing a cyclical improvement with a real easing of financing conditions.

- Assuming markets automatically sanction inefficiency.

What this family of cases reveals about how markets work

The common signal is structural, not cyclical: markets can operate durably in a regime where prices reflect the absence of rupture rather than the quality of prospects. Risk premia do not widen, valuations do not correct sharply, but the capital-selection mechanisms lose their informational power.

Concretely, this reads in indicators that stay calm while fragility accumulates: the financial conditions index (NFCI) that does not tighten, the high-yield credit spreads that do not widen — until the turn comes. This reading belongs to the framework developed by the pillar page financial markets, where liquidity and diversification appear as endogenous properties, never guaranteed by construction.

In a silent adjustment regime, markets do not react to bad decisions but to the preservation of the established order. The risk is not a brutal rupture: it is a gradual erosion of the capacity to adapt, invisible in conventional indicators.

Scope, limits and condition of invalidation

This grid is observed in economies of varied profiles, but also in regulated sectors, firms shielded from competition, or asset classes benefiting from implicit support. It provides, however, neither a timetable for rupture, nor a critical threshold, nor a crisis prediction: it illuminates a dynamic, not a tipping point.

The reading loses its relevance in two cases. First, when a structural shock — an abrupt change of monetary regime, a systemic crisis — renders the framework obsolete and reintroduces a corrective pull. Second, when the real cost of capital recedes durably: the constraint that feeds the inertia then loosens, and selection mechanisms regain their informational power.

Markets price the absence of catastrophe, not the quality of allocation. As long as the stability of the framework is taken for granted and the real cost of capital stays binding, inefficiency can accumulate without any visible correction.

- The persistence of an institutional, monetary or regulatory framework does not guarantee the soundness of the decisions taken within it.

- Markets can evolve durably in a sub-optimal regime without issuing any warning signal.

- The real cost of capital links these regimes; the real level of rates matters more than their nominal path.

- The correction is not suppressed but deferred — the market sanction is spread out over time.

Case studies applying this grid: silent exchange-rate adjustment, homogenization of behavior and stabilization through regulation. Related case on decision discipline: performance without outperformance. Proprietary macro-financial data (CSV/XLSX, Python/R code): Data & research hub and the crypto-assets pillar.

The configurations hardest to decode are not those marked by instability. They are those where the system keeps running on the surface while quietly undermining its own internal mechanisms. The silence of the market is not the silence of the economy.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…

Inverted Yield Curve: Reading a Regime Signal Without Immediate Effect

The inverted yield curve operates as a regime signal, not a timing tool. Its lagged effects are constitutive…