How Credit Conditions Shape Asset Valuations

Credit availability, leverage and liquidity shape asset prices well beyond fundamentals. The procyclical loop linking financing conditions to valuations amplifies both expansion and correction phases.

The role of credit, leverage and liquidity in the formation of prices for financial and real assets.

TL;DR

When credit is cheap and plentiful, leveraged buyers bid prices above what earnings justify; the same liquidity that looks abundant can vanish once financing tightens.

- Access to cheap credit lets buyers mobilize more capital per unit of equity; Fed data put average leverage in US commercial real estate near 65% at end-2025, up from 58% in 2019.

- Apparent market liquidity depends on financing availability and can vanish when conditions tighten; euro-area high-yield spreads near 350 basis points in early 2026 assume the most fragile issuers keep refinancing access.

- Credit spreads and loan-to-value ratios act as leading indicators of valuation pressure, while ECB surveys signaled continued tightening of origination standards in early 2026, particularly in real estate.

How Credit Conditions Shape Asset Valuations

Asset prices do not respond solely to earnings prospects. The abundance or scarcity of credit alters investors’ capacity to take positions. Financial leverage and liquidity reshape risk perception. The relationship is often reduced to a question of interest rates. It rests, however, on a broader financing dynamic. Credit thus acts as a key determinant of valuations.

When financing is accessible and cheap, buyers can mobilize more capital for the same initial equity stake. The mechanic pushes prices higher, regardless of the underlying fundamentals.

Leverage Amplifies Price Moves

Access to credit allows investors to acquire assets with partial equity. An investor with €100,000 can control a €500,000 asset at 5x leverage. If the asset appreciates by 10%, the gain on equity reaches 50%.

The arithmetic works in both directions. On the way down, losses are amplified just as much. Leverage turns moderate variations into significant moves on equity.

At the aggregate level, credit availability determines the level of leverage the system can support. In expansion phases, conditions ease. Loan-to-value ratios rise. Collateral requirements decline. Prices rise.

Fed data show that average leverage in US commercial real estate stood at roughly 65% at end-2025, compared with roughly 58% in 2019. The increase reflects more generous financing access during the low-rate period.

Liquidity Creates an Illusion of Stability

As long as credit remains abundant, markets display apparent liquidity. Transactions clear without friction. Bid-ask spreads stay contained. The fluidity masks a dependence on financing.

When conditions tighten, liquidity can vanish abruptly. Leveraged buyers withdraw. Forced sellers emerge. Prices adjust discontinuously.

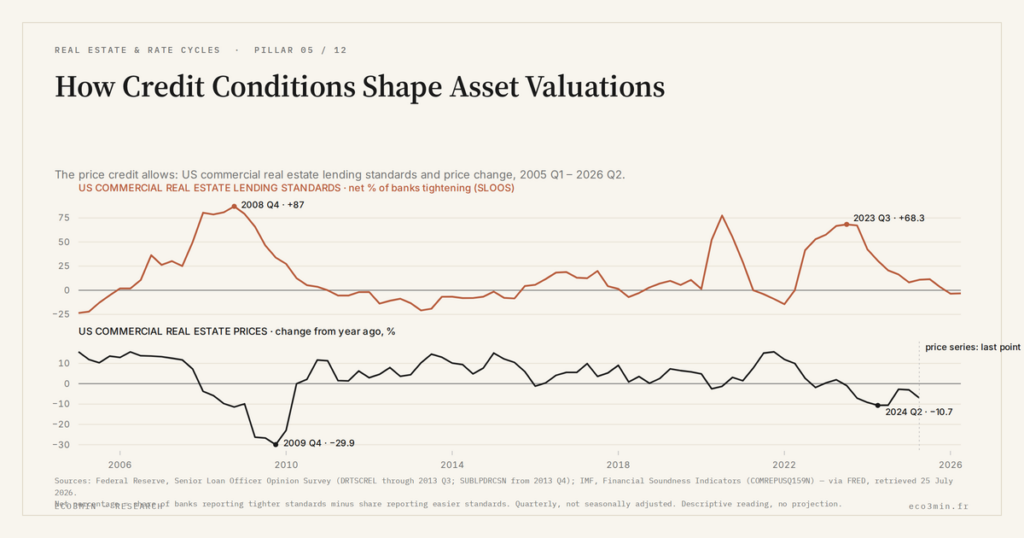

This phenomenon explains why real estate markets, heavily dependent on credit, experience corrections more abrupt than their apparent inertia would suggest. Assessment of the credit cycle as a driver of valuations offers a structuring framework for this sequence.

The Effect Across Asset Classes

Not all assets are equally sensitive to credit conditions. Real estate, financed by construction with leverage, reacts strongly to shifts in financing access. Equities of indebted companies likewise amplify credit-cycle moves.

Corporate bonds embed credit cost directly in their valuation. Spreads, the yield gap to sovereigns, reflect the perception of default risk, itself tied to financing conditions.

In early 2026, euro-area high yield spreads were trading around 350 basis points, a historically moderate level. The compression assumes refinancing access remains intact for the most fragile issuers.

What Current Valuations Embed

Asset prices incorporate implicit assumptions about future financing conditions. Elevated valuations generally assume that credit will remain available, that refinancing rates will stay contained, and that leveraged buyers will be able to maintain their positions.

These assumptions deserve scrutiny late in the cycle. Consensus expects a gradual easing of monetary conditions. But transmission from central bank policy to actual credit conditions is neither automatic nor immediate.

A divergence between policy rates and origination standards can keep valuations under pressure even as rates fall. The scenario partially materialized in 2024-2025, when the ECB’s first rate cuts did not immediately revive mortgage credit. The full mechanism, from rate shock to price adjustment, is detailed in the mortgage credit transmission mechanism to prices.

- Credit determines leveraged purchasing power, directly influencing asset prices beyond fundamentals alone.

- Apparent market liquidity depends on financing availability and can disappear quickly during a tightening phase.

- Credit spreads and loan-to-value ratios act as leading indicators of valuation pressure.

Feedback Mechanisms

The credit-valuation relationship runs in both directions. High asset prices improve collateral values, easing credit access. The virtuous loop fuels expansion phases.

In a downturn, the mechanism reverses. Falling prices reduce collateral values. Lenders tighten standards. Forced sales deepen the correction. Take of financial leverage and systemic fragility details this negative feedback loop.

This procyclicality is a structural feature of credit-financed markets. It amplifies both rallies and corrections, generating dynamics that go beyond what fundamentals alone would justify.

Why This Dynamic Matters Now

After a decade of exceptionally favorable financing conditions, valuations of many assets embed optimistic assumptions about future credit availability. Commercial real estate, private equity and certain bond segments have been particularly sensitive to this environment.

The shift to higher rates and tighter origination standards forces a reassessment. Not necessarily a violent correction, but an adjustment of multiples consistent with a durably higher cost of capital.

Variables That Could Alter the Trajectory

A rapid return to highly accommodative financing conditions would extend the current cycle. A pronounced recession would accelerate the adjustment by forcing sales and degrading credit quality. A stabilization of rates at intermediate levels would imply a gradual but durable adjustment of valuations.

The behavior of commercial banks is the key variable. Their risk appetite determines, beyond policy rates, the actual conditions of access to financing. ECB surveys signaled in early 2026 a continued tightening of origination standards, particularly in real estate.

Understanding the credit cycle in its entirety allows these signals to be situated in a coherent perspective and their effects on different asset classes anticipated.

Last updated — 25 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →US Rental Property Real Yield: What Cap Rate and NOI Actually Leave You

A rental listing leads with a yield. Divide the annual rent by the price and the number looks…

Cap Rate Spread: What Rental Yield Pays Over the 10-Year Treasury

A 5% cap rate sounds attractive. But 5% against what? A risk-free 10-year Treasury yields near 4.5% in…

US Rental NOI, Line by Line: What Net Operating Income Really Subtracts

A US rental yield is advertised gross: annual rent over price. Between that number and the income an…