Crypto Assets Are Not Money: Economic Functions and Structural Limits

Analysis of the economic functions of money and the structural limits of crypto-assets in fulfilling them sustainably.

TL;DR

Money is defined by three functions—unit of account, medium of exchange, store of value—built over decades of institutional anchoring; most crypto-assets fall short of all three.

- Money's three functions emerge through repeated use, legal frameworks and collective acceptance, historically consolidated over decades, sometimes centuries.

- Even when payments are made in crypto-assets, values are typically priced in fiat and then converted, leaving them short of a stable unit-of-account role.

- Since 2024, higher rates and monetary normalization dulled purely technological narratives, while volatility across major crypto-assets in 2025 renewed doubts about their use as monetary instruments.

The rapid rise of crypto-assets has fueled persistent confusion between technological innovation and economic status. Being digital, decentralized, or exchangeable is not sufficient to confer a monetary function. Money is based on stabilized uses and collective conventions that go far beyond simple value transfer. Treating any exchangeable asset as money leads to flawed interpretations of its uses and valuation. Clarifying this distinction helps better understand the real role of crypto-assets in the economy and financial system.

- Money is прежде всего an economic institution, not a technology.

- Most crypto-assets struggle to fulfill core monetary functions.

- Confusing exchangeable assets with money distorts their economic analysis.

What the economic functions of money actually involve

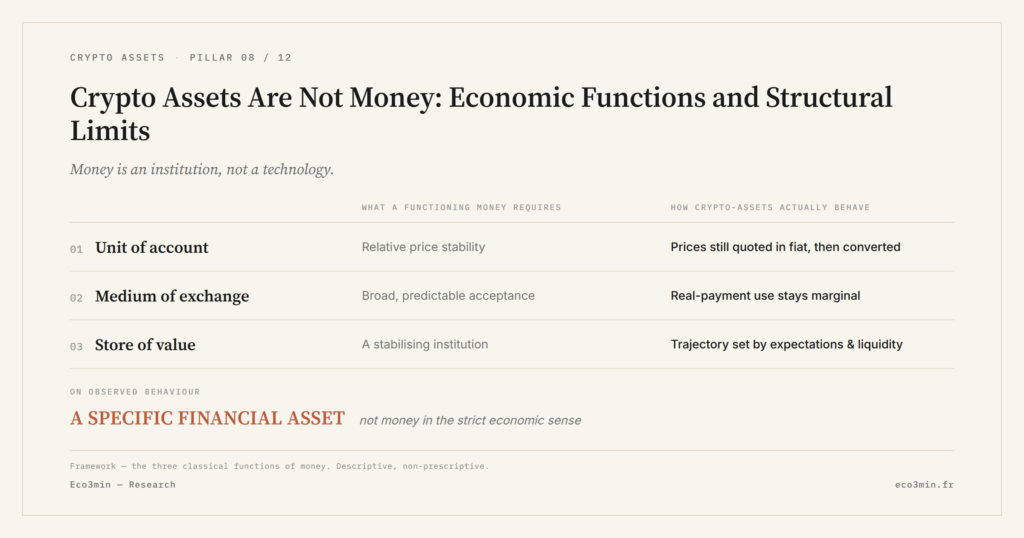

In economics, money is not defined by its form but by three core functions: unit of account, medium of exchange, and store of value. These functions emerge gradually through repeated use, legal frameworks, and collective acceptance. Historically, their consolidation has taken decades, sometimes centuries, supported by institutions capable of ensuring continuity and trust.

A unit of account requires relative price stability. A medium of exchange requires broad and predictable acceptance. A store of value requires the ability to preserve purchasing power over a sufficiently long horizon to support economic decisions. These criteria are demanding and interdependent.

Why crypto-assets struggle to fulfill these functions

Most crypto-assets first struggle to act as a unit of account. High price volatility makes them unstable as a reference of value, limiting their use in pricing or contracts. In practice, even when payments are made in crypto-assets, values are typically calculated in fiat currency and then converted.

As a medium of exchange, crypto-assets remain confined to niche uses. Variable transaction costs, confirmation delays, and regulatory uncertainty constrain their everyday adoption. As a store of value, their trajectory relies more on market expectations than on stabilizing institutional mechanisms.

This lack of stabilizing institutional mechanisms is also reflected in price dynamics, with cycles that are significantly larger and faster than in equity markets, as illustrated in the analysis on the structural intensity of crypto-asset cycles.

The dominant consensus and its limits

Part of the consensus assumes that technological innovation will eventually overcome these limitations. The central scenario suggests that improvements in protocols, lower costs, and broader adoption will be sufficient to create an alternative monetary form.

This view often conflates usage diffusion with economic stabilization. Market observations show that increased adoption does not mechanically translate into stable or coherent price trajectories, as discussed in the analysis of the disconnect between crypto adoption and valuation.

This perspective underestimates the role of collective conventions and institutional frameworks. The challenge is not only technical but deeply economic: without stable usage patterns and institutional anchoring, a transition to monetary status remains uncertain.

The focus on programmed scarcity also reflects this incomplete view. Supply constraints can influence financial dynamics, but they are not sufficient to create autonomous monetary value, as shown in the analysis of the economic limits of crypto scarcity.

A context that makes the issue more visible today

Since 2024, persistently higher interest rates and monetary normalization have reduced the appeal of purely technological narratives. At the same time, volatility observed across major crypto-assets in 2025 has renewed questions about their ability to serve as credible monetary instruments beyond favorable market phases.

What the reader is really trying to understand

Behind the monetary question lies a simpler one: is this a stable economic tool or a financial asset subject to pronounced cycles? The real issue is not whether these assets can circulate, but whether they can sustainably structure economic decisions without external reference. The empirical detail appears in bitcoin through liquidity and real-rate cycles.

Common interpretation mistakes

Confusing occasional payment usage with functional money leads to overestimating the economic relevance of crypto-assets. Isolated transactional use does not create a stable monetary function.

Economic and financial implications

This distinction has direct implications for analyzing crypto-assets. Treating them as currencies leads to misreading their cycles, sensitivity to financial conditions, and interaction with monetary policy. Treating them as specific financial assets, by contrast, provides a clearer understanding of their behavior across liquidity expansion and contraction phases. our sub-pillar on bitcoin and Liquidity Cycles examines this pattern with the data series in hand. For context: the Eco3min study of how liquidity cycles move crypto.

Within a macroeconomic framework shaped by regime adjustments, this approach avoids projecting monetary properties onto assets that do not structurally possess them. It also clarifies debates about their future role within the financial system.

Alternative scenarios and fragility points

A major institutional shift, deep regulatory integration, or the emergence of large-scale non-speculative use cases could alter this analysis. Conversely, tighter regulation or a prolonged liquidity shock would reinforce their status as volatile financial assets rather than functional money.

Recent regulatory developments are moving more toward clarifying participants and access channels than toward monetary recognition. They reshape market structure without altering the economic nature of the assets, as analyzed in the study on the real effects of crypto regulation.

To assess the monetary nature of an asset, one must separately evaluate usage stability, collective acceptance, and institutional anchoring—without conflating technical innovation with economic function.

Money is a stabilized institutional construct, whereas most crypto-assets remain market instruments driven by expectations and liquidity conditions.

Conclusion

Crypto-assets raise legitimate questions about the evolution of monetary forms, but their current economic nature aligns more closely with financial assets than with money in the strict sense. A durable monetary transformation would require deep changes that go far beyond technology alone. Until these conditions are met, the risk is projecting functions onto these assets that they cannot yet fulfill.

3 key takeaways

- Monetary function relies on usage and institutions, not just technology.

- Volatility limits crypto-assets’ ability to serve as a unit of account and store of value.

- Analyzing them as financial assets helps avoid major misinterpretations.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Crypto Seasonality: Why the Signal Is Weaker Than It Looks

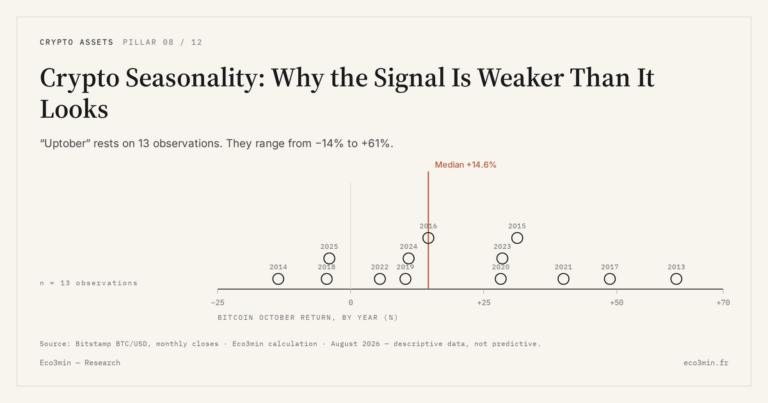

Crypto’s cyclical regularities, monthly seasonality or the four-year cycle, rest on a very small number of observations. That…

Bitcoin Halving: How the Programmed Supply Cut Works

The halving writes bitcoin’s scarcity into an immutable rule, applied without exception since 2012. It shapes the pace…

Crypto Cycles: Why Their Amplitude Dwarfs Equity Swings

Crypto cycles post drawdowns two to four times deeper than equity markets. The asymmetry stems from market microstructure,…