When Financial Innovation Rigidifies Market Behaviour

Some financial innovations do not improve market efficiency but homogenise decisions and reinforce systemic fragility. A macro-financial case study on the invisible collective effects of innovation.

Contemporary financial markets present a striking paradox: innovations meant to optimise risk management and improve diversification produce the opposite effect. By standardising practices and rigidifying strategies, they amplify collective vulnerability during episodes of stress.

TL;DR

Innovations built to spread risk can concentrate it: when identical optimised strategies are adopted at scale, behaviour synchronises and stress propagates faster, per BIS, IMF and FSB work. The broader logic is traced in AI’s systemic footprint in markets.

- Innovations meant to optimise risk (structured products, standardised frameworks, quantitative strategies) can amplify collective vulnerability by homogenising behaviour, per BIS, IMF and FSB work on procyclicality.

- When the same models scale across participants, repositioning concentrates on identical thresholds, liquidity evaporates and hedging mechanisms stop absorbing shocks.

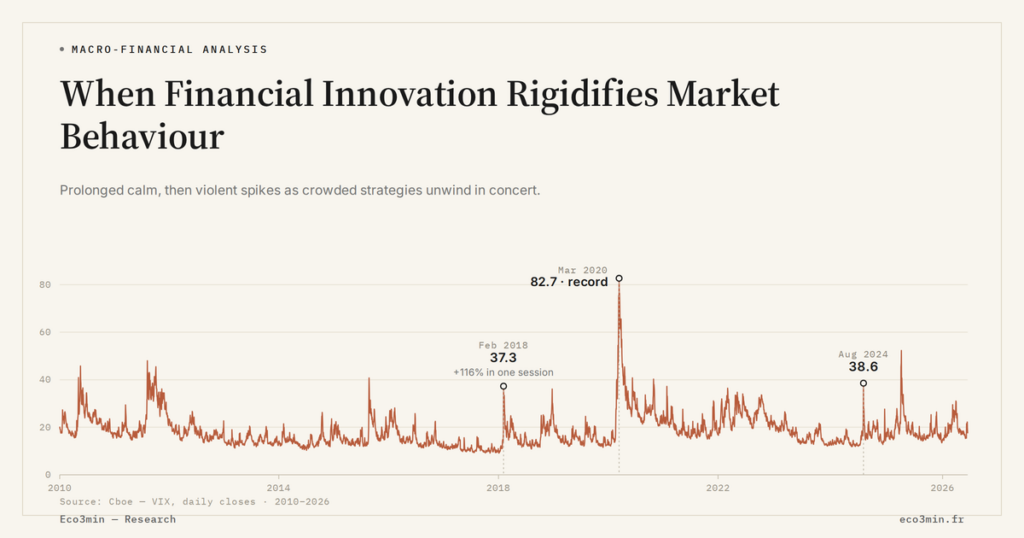

- The IMF's Global Financial Stability Reports note that prolonged volatility compression can mask vulnerabilities that surface abruptly when conditions turn.

- The analysis covers traditional-market innovation since the mid-2010s and explicitly sets aside crypto-assets and blockchain.

This reading aligns with the analyses developed by the Bank for International Settlements (BIS), the IMF and the Financial Stability Board (FSB) on the procyclicality of investment strategies and the systemic risks tied to the homogenisation of market behaviour.

This analysis draws on the work of financial stability institutions (BIS, IMF, FSB) on the procyclicality of financial innovations and the mechanisms by which the standardisation of behaviour amplifies systemic risk.

Introduction — The empirical observation

Since the mid-2010s, the financial industry has celebrated innovation as a driver of progress. New investment vehicles, sophisticated algorithms, automation of decision-making processes: these advances promise more efficient capital allocation and better risk control. More on this: Why AI Drives Concentration Among Financial Players.

Yet observation of the markets reveals a more nuanced reality. Across several asset classes, investor behaviour converges in a way that has become a concern, responses to shocks synchronise and portfolio adjustments grow more abrupt. Periods of turbulence no longer reflect greater resilience but an amplified propagation of stress.

This paradox raises a fundamental question: through which mechanisms do tools designed to smooth exchanges end up crystallising behaviour and weakening the entire system?

This analysis covers financial innovation broadly defined — structured products, standardised management frameworks, quantitative strategies — and deliberately excludes crypto-assets and blockchain technologies. The phenomena studied stem from institutional and behavioural dynamics at work in traditional markets.

The market environment and the dominant narrative

These dynamics fit within a singular context: a decade of exceptionally low rates, followed by gradual monetary tightening. The search for yield, combined with regulatory requirements and the standardisation of professional practices, accelerated the mass adoption of instruments presented as both high-performing and prudent.

The prevailing narrative establishes an equivalence between innovation and efficiency gains. New products are perceived as technical responses to structural problems: insufficient diversification, excessive transaction costs, imperfections in risk hedging. This reading frame celebrates the sophistication of tools without questioning their systemic effects.

Within this interpretive frame, low volatility observed over long periods is read as validation of the model. Yet, as the analysis of reassuring macroeconomic indicators demonstrates, this apparent calm can conceal an insidious concentration of vulnerabilities and a growing dependence on shared mechanisms.

Anatomy of the phenomenon

The case study covers a market sequence characterised by the broad diffusion of so-called “optimised” strategies. Allocation decisions rest on comparable models, obey similar constraints and operate within converging time horizons.

In a first phase, this uniformity produces seemingly beneficial effects. Volatility recedes, performance dispersion narrows, capital flows stabilise. Strategies appear all the more effective as they are massively adopted.

This compression of volatility and behavioural mimicry can create the illusion of a more efficient market, when they sometimes signal a latent fragility tied to the standardisation of approaches, as highlighted in the analysis of misleading economic indicators.

When conditions deteriorate — a higher cost of capital, an exogenous shock or a sharp revision of expectations — repositioning takes place in concert. Sell orders concentrate on the same segments, liquidity evaporates rapidly and hedging mechanisms cease to play their shock-absorbing role.

Concrete manifestation — Innovation turned into a collective reflex

This regime becomes tangible when identical management rules activate simultaneously across otherwise independent participants. Trades trigger on comparable thresholds, risk adjustments follow parallel paths and decisions deemed prudent converge in time.

This configuration emerges as soon as investors adopt solutions perceived as rational not for their intrinsic superiority, but because they reduce divergence from prevailing practices.

Innovation then ceases to be a source of differentiation. It becomes a tacit compliance framework: the chosen solutions are those that appear acceptable in light of sectoral norms, peer comparisons and institutional expectations, even when they restrict individual room for manoeuvre.

What stands out is not so much the existence of losses as their synchronisation and relative scale, both revealing of a collective fragility built up by gradual accumulation.

Decoding the mechanisms at work

The dominant narrative posits that financial innovation diversifies behaviour. This hypothesis obscures a crucial point: when the same tools are adopted at scale, they mechanically generate similar reactions.

According to the IMF’s Global Financial Stability Reports (GFSR), the prolonged compression of volatility can mask an accumulation of vulnerabilities, with adjustments occurring in synchronised and amplified fashion when market conditions turn.

On the macro-financial side, the first identified lever is the cost of financing. In an environment of durably restrictive real interest rates, room for manoeuvre narrows. Strategies then favour short-term optimisation and the reduction of apparent volatility over structural adaptation to a changing environment.

On the micro-financial side, the automation and standardisation of decision-making processes reinforce correlation across participants. Management rules, designed to contain individual risk, end up amplifying collective risk during periods of stress.

Expectations are the final key driver. The trust placed in the robustness of innovations dulls the incentive to question dominant strategies, until the moment when their procyclical character manifests abruptly.

The drivers of persistence

At this stage, innovation no longer functions as a lever of differentiation but as an implicit norm. Departing from it does not represent a strategic risk-taking but a relative risk: that of appearing deviant, less compliant or more exposed than peers.

In this equilibrium, alignment with dominant practices provides a form of institutional protection. As long as the collective framework holds, no participant has any interest in breaking the convergence. Innovation then ceases to be a vector of adaptation and becomes an unchallenged norm — stabilising on the surface but rigidifying in its aggregate effects. Rational one desk at a time, that alignment is exactly why the risk of algorithmic dominance is convergence rather than speed.

Lessons for understanding markets

This case sheds light on a fundamental property of contemporary markets: individual efficiency does not guarantee collective efficiency. This structural logic is developed in our sub-pillar on financial innovation and market infrastructure. Strategies that are rational in isolation can, once aggregated, produce destabilising dynamics.

Financial markets can thus tip into regimes where apparent stability rests on excessive homogeneity of behaviour. This reading aligns fully with the analytical framework developed on the pillar page dedicated to financial markets, where liquidity and diversification appear as endogenous properties — by no means guaranteed.

The signal sent by this type of configuration is structural in nature: some innovations reduce the dispersion of decisions at the price of greater vulnerability to shocks.

Reading frame — When innovation locks in markets

This case highlights a regime logic: individual rationality can produce aggregate instability when innovation becomes normative. What presents itself as a modernisation of practices then morphs into a standardisation of behaviour.

In these configurations, innovation does not weaken markets through excess complexity but through a reduction in decisional diversity. Surface stability masks a real rigidification, until the shock reveals a fragility built collectively.

General scope, limits and key takeaways

This dynamic extends well beyond the perimeter of the case studied. It can be identified across different market segments whenever innovation becomes prescriptive and compliance prevails over adaptation. A close neighbour in this cluster: When Market Speed Becomes a Source of Fragility.

That said, this case does not allow the conclusion that all financial innovation is harmful. It provides neither a crisis calendar nor a precise turning-point signal. It highlights a mechanism, not an inevitability.

The structural takeaways can be summarised as follows:

- Financial innovation can standardise behaviour rather than diversify it.

- Reducing individual risk can worsen systemic risk.

- Apparent stability can mask growing vulnerability.

- Market analysis must integrate the aggregate effects of dominant strategies.

When innovation becomes the standard, individual rationality synchronises decisions and turns risk management into a source of systemic fragility.

This case study thus offers a reading frame transposable to other contexts, recalling that the most perilous shifts are sometimes those that appear, at first sight, the most rational.

Last updated — 23 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Euro Below Parity in 2022: What Parity Means

In September 2022, the euro fell below parity with the dollar, to around 0.95, a low not seen…

Eurozone Fragmentation: Sovereign Spreads and the Euro

The euro is issued by a monetary union without a complete fiscal union: nineteen sovereign debts coexist under…

The Euro’s Energy Import Bill: the Gas Shock and the Currency

In 2022, the surge in gas prices turned the euro area's historic current-account surplus into a deficit and…