Household vs Corporate Credit: Distinct Macro Effects

Household and corporate credit do not activate the same macroeconomic mechanisms: one supports aggregate demand, the other conditions productive capacity. Aggregating both masks divergent dynamics with different implications for potential growth.

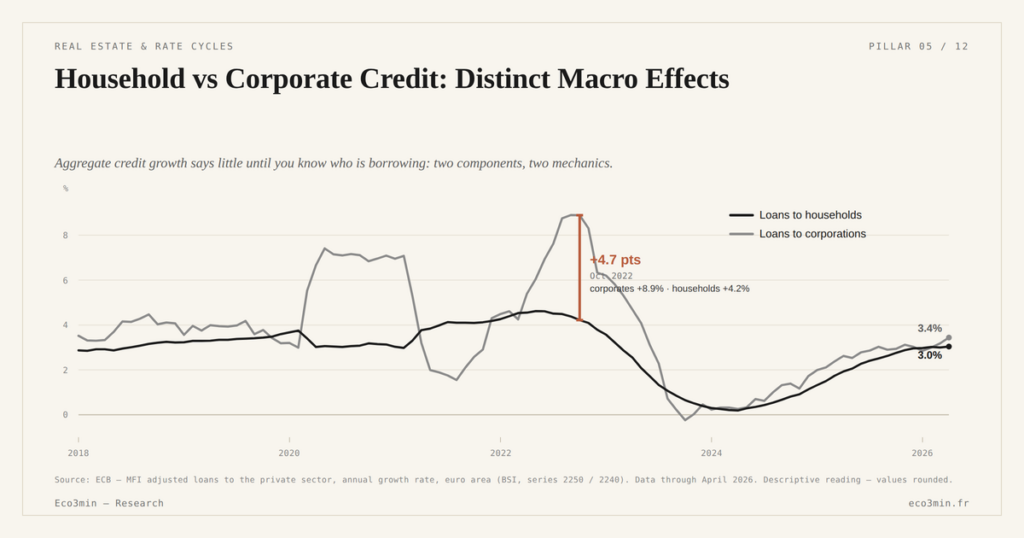

A comparison of the macroeconomic impacts of household credit and corporate credit, based on their uses and transmission channels.

TL;DR

Household credit pulls demand forward while corporate credit builds supply capacity, and euro-area households held about 47% of private-sector credit at end-2025, growing slower than firms.

- Household and corporate credit split euro-area private lending, households at about 47% at end-2025 per ECB data, yet activate different mechanisms: household credit pulls demand forward while corporate credit funds productive capacity.

- French household debt reached about 100% of disposable income at end-2025, up from roughly 85% a decade earlier, a level at which repayment burdens can constrain future consumption.

- The two segments diverge in the cycle: euro-area household credit grew +1.8% against corporate credit's +2.9% at end-2025, and BIS data show two decades of credit growth concentrated in real estate rather than productive investment.

Why all types of credit do not produce the same macroeconomic effects

Credit is often treated as a homogeneous variable. Yet its impact depends on its use and beneficiary. Household financing and corporate financing do not activate the same macroeconomic mechanisms. The first mainly supports demand; the second conditions productive capacity. Conflating these channels leads to incomplete diagnoses. An analytical distinction is essential to grasp the effects of credit.

In the euro area, household credit accounted for ≈47% of total outstanding credit to the private sector at end-2025, according to ECB data. The remainder finances non-financial corporations. These two stocks respond to distinct logics and transmit monetary impulses differently. This heterogeneity fits squarely within the household-corporate segmentation of credit.

Household credit: a short-term demand driver

Household financing concentrates on two main uses: real estate acquisition and consumption. Mortgage credit dominates by far, representing approximately 80% of credit to individuals in France. Eco3min documents this cycle in the framework for reading the residential credit cycle.

This type of credit acts on aggregate demand through several channels. It allows future expenditures to be brought forward by financing them immediately. It supports real estate prices, generating a wealth effect that boosts consumption. It feeds activity in the construction sector.

But this impulse is essentially intertemporal redistribution. Household credit pulls demand forward without necessarily expanding the productive capacity of the economy. When debt reaches high levels, it can even constrain future consumption through the burden of repayments.

The household debt-to-disposable-income ratio reached ≈100% in France at end-2025, compared with ≈85% a decade earlier. This trajectory illustrates a growing dependence on external financing to sustain consumption levels.

Corporate credit: a lever on supply

Corporate financing follows a different logic. It funds productive investment, working capital needs, and external growth operations. Its potential impact bears on production capacity, productivity, and medium-term employment.

The distinction between cash-flow credit and investment credit matters. The first smooths cash-flow timing without altering the productive structure. The second commits capital expenditure that can durably increase value added.

In practice, the share of corporate credit effectively oriented toward productive investment remains hard to measure. A significant fraction finances share buybacks, acquisitions, or financial restructurings. These uses do not produce the same macroeconomic effects as capacity investment.

The asymmetry of cyclical effects

The two types of credit do not respond to the cycle in the same way. Household credit tends to be more procyclical and more sensitive to real estate conditions. Corporate credit responds more to demand prospects and the cost of capital.

During monetary tightening phases, mortgage credit generally contracts faster. Transactions decline, prices adjust, and the flow of new loans falls. Corporate credit often holds up longer, supported by existing credit lines and refinancing needs.

This asymmetry explains why the same tightening of financial conditions can produce very different sectoral effects. To deepen this causal mechanism, the analysis of the credit cycle and its effects on the real economy provides the structuring framework.

What consensus tends to overlook

Macroeconomic analyses often aggregate total credit without distinguishing its components. This approach masks divergent dynamics. A rise in household credit and a rise in corporate credit do not carry the same economic meaning.

An economy where credit grows mainly through household real estate indebtedness does not display the same potential as one where credit funds productive investment. The first accumulates pulled-forward demand. The second builds supply capacity.

BIS data suggest that in several advanced economies, credit growth over the past two decades has concentrated on the real estate segment. This structural orientation has implications for the trajectory of potential growth.

Treating a rise in total credit as an unambiguous signal of economic dynamism. The composition of credit matters as much as its volume. Credit oriented toward household real estate does not produce the same medium-term effects as credit financing corporate investment.

Differentiated sectoral implications

For the real estate sector, household credit dynamics are the main driver. Transaction volumes, prices, and construction activity depend closely on financing conditions for individuals.

For the manufacturing sector, corporate credit has a greater bearing on investment and employment decisions. The availability of long-term financing at controlled cost determines the capacity to modernize the productive apparatus.

For financial markets, the distinction between private credit and other forms of indebtedness affects sectoral risk assessment. The review of private credit compared with public debt helps map these differentiated exposures.

Indicators to watch

Tracking outstanding amounts separately by segment — households/corporates, real estate/consumption/investment — provides a finer reading of the cycle. Surveys on credit demand and lending standards help anticipate inflections before they appear in stock data.

In the euro area, the growth gap between household credit (+1.8% at end-2025) and corporate credit (+2.9%) signals distinct sectoral dynamics that the total aggregate fails to capture.

What this distinction changes in the reading

The question is not only whether credit grows or contracts, but where this dynamic concentrates. A contraction in household mortgage credit alongside stable corporate credit does not carry the same implications as the reverse pattern.

This heterogeneity complicates diagnoses but enriches understanding. It is a reminder that credit is not an abstract variable but a set of flows oriented toward specific uses, each with distinct effects on the economic trajectory.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →US Rental Property Real Yield: What Cap Rate and NOI Actually Leave You

A rental listing leads with a yield. Divide the annual rent by the price and the number looks…

Cap Rate Spread: What Rental Yield Pays Over the 10-Year Treasury

A 5% cap rate sounds attractive. But 5% against what? A risk-free 10-year Treasury yields near 4.5% in…

US Rental NOI, Line by Line: What Net Operating Income Really Subtracts

A US rental yield is advertised gross: annual rent over price. Between that number and the income an…