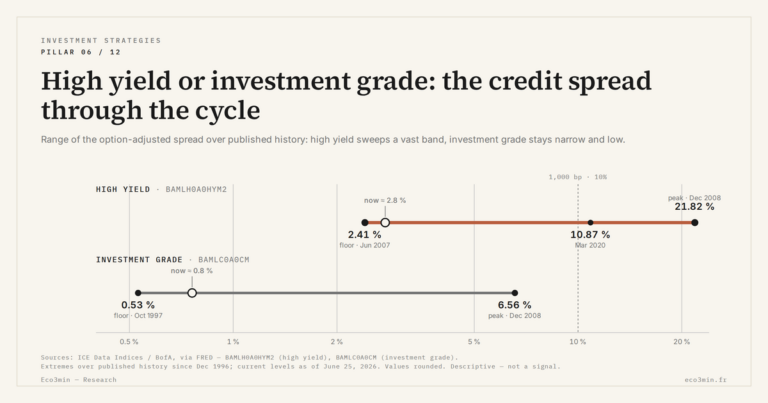

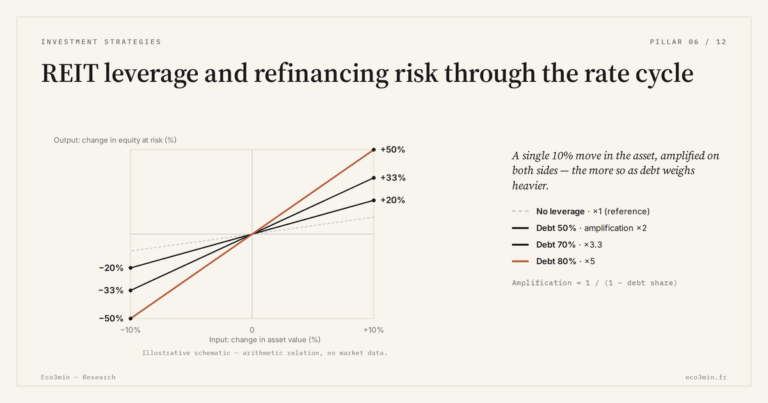

REIT leverage and refinancing risk through the rate cycle

For listed REITs, the leverage that matters most sits inside the vehicle, as property debt that must be refinanced. When rates rise, two things compress returns at once: assets reprice down as cap rates climb, and maturing debt rolls over…