Inflation: The Lagged Response to Monetary Decisions

Inflation does not react instantly to central bank decisions. A gradual transmission chain — financial conditions, demand, wages and costs, then final prices — introduces delays measured in quarters between policy moves and observed inflation.

Inflation does not react instantly to central bank decisions. Between the adjustment of policy rates and the evolution of prices, a gradual transmission chain — financial, real and wage-related — introduces delays measured in quarters.

TL;DR

Inflation trails monetary decisions by quarters, with euro-area industrial producer prices falling from mid-2023 while consumer prices followed only about nine months later (Eurostat, December 2025).

- Prices move in stages: commodities adjust in real time, industrial prices lag two to four months, consumer prices six to twelve as distribution margins readjust, with the euro-area PPI trough exceeding -8% year-on-year.

- Wages are the inertia anchor: collective bargaining covers over 80% of employees in countries like France, Italy and Belgium, and negotiated euro-area wages still ran +3.8% year-on-year in Q3 2025 (ECB), indexed to past inflation.

- Second-round effects keep costs hot: euro-area services producer prices rose +3.2% year-on-year in Q3 2025 (INSEE), wage-driven, as firms passing labour costs into prices can stretch an episode beyond the initial shock.

Understanding these lags is essential to read price dynamics accurately. Monetary policy acts first on financial conditions, then on demand, on production costs and finally on the formation of final prices. Each link adjusts at its own pace, creating structural inertia between the monetary decision and observed inflation.

Inflation responds with a lag to monetary policy decisions because of nominal rigidities and price chains. Between a central bank’s decision and the observable evolution of price indices, transmission runs through several interdependent mechanisms — financing conditions, consumption and investment trade-offs, wage negotiations and margin adjustments — that diffuse gradually into the real economy.

This lag is neither an anomaly nor a malfunction: it reflects the very structure of modern economies. Contracts are rigid in the short term, wages are renegotiated periodically, firms adjust prices cautiously to preserve demand, and supply chains transmit cost variations through successive stages. Monetary policy therefore operates by accumulation, not by instantaneous impulse.

Inflation does not move immediately after monetary tightening or easing. Price and wage chains embed deep rigidities. This lag often feeds the perception of a loss of monetary control. In practice, it reflects the long timeframe of nominal adjustments. Grasping this mechanism places inflation back within the transmission sequence.

What shifts the price trajectory is less the rate move itself than the speed at which contracts, wages and intermediate costs adjust. This mechanism, familiar to economists, remains largely absent from public debate on inflation.

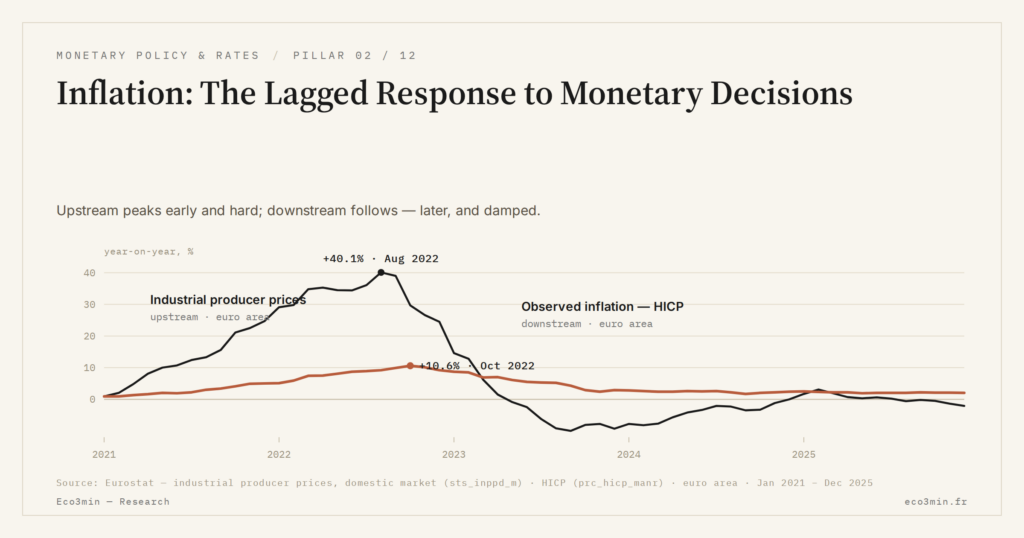

Prices that move in stages

Inflation does not form in a single location of the economy. It results from the superposition of pricing decisions taken at different moments by agents that do not react to the same signals. Commodity prices adjust in real time on international markets. Industrial prices incorporate these variations with a two to four-month lag, the time needed for existing inventories to clear. The Eco3min dossier on the slow feed-through of rates into margins situates this within the wider regime. Consumer prices only move once distribution margins have readjusted — a process spanning six to twelve months. Companion analysis: Our note on liquidity, financial conditions and the plumbing of QT cycles.

Eurostat data (December 2025) illustrate this sequence. The euro area industrial producer price index began declining as early as mid-2023, with a cumulative drop of more than 8% year-on-year at its trough. The harmonised consumer price index followed this move only with a roughly nine-month lag. The desynchronisation between inflation, growth and rates is largely explained by these cascading lags along the value chain.

Wages: the inertia anchor in the price chain

Wages constitute the stickiest cost item. In the euro area, collective bargaining covers more than 80% of employees in several countries (France, Italy, Belgium, Austria). These agreements are negotiated over annual or multi-year cycles, with indexation clauses tied to past inflation rather than anticipated inflation.

According to ECB data on negotiated wages (Q3 2025), euro area wage growth still stood at +3.8% year-on-year, a pace clearly above the 2% inflation target. This persistence of robust wage dynamics — even as headline inflation receded — illustrates the post-inflation catch-up effect: wages incorporate the 2022-2023 price surge with a lag, mechanically prolonging pressure on unit costs.

The persistence of inflation despite monetary tightening finds here one of its core explanatory mechanisms. As long as wages catch up with past inflation, production costs remain under pressure and the decline in final prices is delayed.

Interpreting inflation persistence above target as a monetary policy failure. Tightening acts first on financial conditions, then on demand, and finally on prices — with a cumulative lag of 18 to 24 months. The inflation observed today partly reflects pricing decisions taken before tightening reached the productive economy.

Second-round effects: when inflation self-sustains

The main risk in the transmission sequence to prices lies in second-round effects. When firms pass higher wage costs into their sale prices, they feed a price-wage loop that can extend the inflation episode well beyond the initial shock.

INSEE data on services producer price indices (Q3 2025) show a +3.2% year-on-year increase, driven by the wage component. This labour-intensive sector provides fertile ground for second-round effects. The time monetary policy takes to reach price-formation mechanisms determines how long these loops can operate before being interrupted.

Market consensus in early 2026 anticipated euro area inflation returning to 2% by late 2026 or early 2027. This projection assumes a gradual easing of wage dynamics and the absence of any new supply shock. Central banks’ steering of this disinflation phase runs up against the irreducible inertia of wage contracts and indexation mechanisms — variables on which the monetary instrument has only an indirect and delayed grip.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…

Inverted Yield Curve: Reading a Regime Signal Without Immediate Effect

The inverted yield curve operates as a regime signal, not a timing tool. Its lagged effects are constitutive…