How Liquidity Sustains Equity Markets Without Recovery

Liquidity flows can sustain equity markets without economic recovery. Passive flows, buybacks and central bank policy create autonomous market support, often disconnected from the underlying business cycle.

Liquidity can lift equities without economic recovery. A breakdown of financial flows and their impact on markets.

TL;DR

Passive equity flows keep indices rising through a growth slowdown: global equity ETF net flows ran an estimated $800–900 billion a year between 2023 and late 2025. The corresponding material is set out in hidden risk beneath stable benchmarks.

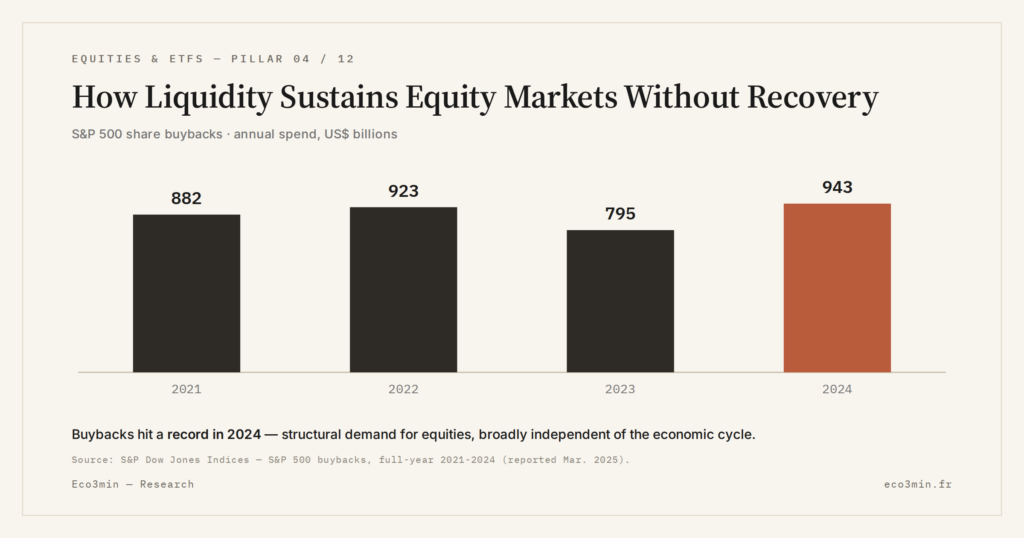

- In 2024, US corporate share buybacks exceeded $900 billion, reducing float and supporting prices even with modest earnings growth.

- In 2024–2025, with US growth around 2%, expectations of monetary easing alone sustained accommodative financial conditions without any pickup in productive investment.

- Passive flows toward market-cap-weighted indices automatically channel capital to the largest names, amplifying concentration and index resilience independent of fundamentals.

- Since late 2025, higher real rates coexist with still-abundant passive and institutional liquidity, making classic economic signals less operative for reading markets.

For several quarters, equity markets have advanced in fits and starts while macroeconomic indicators have remained mixed. Sluggish growth, hesitant productivity, margins under pressure in certain sectors. Indices, however, are holding. The gap is explained less by improving fundamentals than by the circulation of financial liquidity, often invisible in traditional economic statistics. This point is illuminated in how monetary regimes reprice equities.

Financial Flows Disconnected From the Cycle

Liquidity here refers to the financial system’s ability to supply capital available for asset purchases. It comes primarily from monetary policy, institutional savings and market mechanisms such as passive investing. Unlike growth or employment, these flows do not require a dynamic economy to deploy.

Between 2023 and late 2025, despite a marked growth slowdown across several developed economies, assets invested in global equity ETFs continued to rise, with estimated annual net flows around ≈$800 to $900 billion according to aggregated market data. This mechanical demand creates price support, independent of the immediate trajectory of activity.

The phenomenon fits within a broader logic of dissociation between financial markets and the real economy, already structured in the explanatory framework presented in the cluster’s pillar article.

Monetary Policy: The Most Powerful Indirect Channel

Part of the consensus still associates market support with economic recovery. This reading assumes central banks loosen policy only in response to cyclical improvement. Recent episodes show the opposite: liquidity can rise within a deteriorated economic context.

When central banks stabilize or cut policy rates, or signal the end of a restrictive cycle, marginal liquidity returns to financial markets before diffusing into the economy. In 2024–2025, while US growth hovered around ≈2%, expectations of monetary easing were enough to sustain accommodative financial conditions, without any visible acceleration in productive investment. A related read: Why GDP Growth Is a Poor Indicator for Equity Markets.

The channel is indirect but effective: lower expected volatility, compressed risk premia, reallocation toward risk assets. Liquidity acts through valuation, not through production.

Buybacks and Passive Investing: A Structural Demand

Alongside central banks, companies themselves constitute a major source of liquidity for equity markets. Share buyback programs reduce available float and mechanically support prices, even absent revenue growth. In depth: the myths surrounding the stock market.

This demand is amplified by passive flows, whose automatic allocation mechanics reinforce buying pressure on already dominant capitalizations, independent of any fundamental analysis.

In 2024, US corporate share buybacks exceeded ≈$900 billion, a high level relative to modest earnings growth. This internal demand acts as a market shock absorber, broadly insensitive to the short-term economic cycle.

Passive investing reinforces this dynamic. Flows toward market-cap-weighted indices automatically direct capital to the largest names, amplifying concentration and index resilience. To understand this structural mechanism, it is useful to revisit how equity markets function and the weighting logic underpinning them.

A Time Lag Often Misread

This liquidity support creates a lagging effect. Markets rise before the economy improves, or without it actually doing so. This point is often interpreted as the rational anticipation of a future recovery.

Yet in many recent episodes, the rise in indices preceded only a basic economic stabilization, without any genuine subsequent acceleration. Liquidity acts immediately, where macroeconomic adjustments take several quarters. This lag blurs the cyclical reading.

What becomes relevant now relates to the regime change observed since late 2025: higher real rates, but financial liquidity still abundant through passive and institutional flows. This coexistence makes classic economic signals less operative for reading markets.

Equating a rise in indices with improving economic fundamentals leads to ignoring the autonomous role of financial flows and liquidity mechanisms.

What Could Challenge This Support

Liquidity is neither unlimited nor eternal. Several factors can reduce its impact. A more durable monetary tightening than expected, a rise in volatility or a reversal in passive flows would rapidly alter the current equilibrium.

Some market participants currently favor the hypothesis of a gradual normalization without shock. This hypothesis rests on the stability of flows and monetary policy. A break in either parameter would suffice to weaken the current support, even without further macroeconomic deterioration.

Observable Economic Impacts

For companies, this dynamic favors large listed groups able to access financial markets directly, independent of final demand. For households, it widens the gap between daily economic perception and financial asset performance. For markets, it deepens concentration and sensitivity to flows.

Liquidity thus becomes a central reading variable, distinct from growth, employment or productivity. A financial variable, not an economic one.

- Financial liquidity can support equity markets without any improvement in growth or employment.

- Passive flows and buybacks create structural demand broadly insensitive to the economic cycle.

- The time lag between markets and the real economy complicates the cyclical interpretation of equity rallies.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Reading Earnings Surprises: Cash Flow, Margins, Guidance

How to analyze an earnings surprise beyond the simple beat or miss: cash flow, margins, guidance, and weak…

Equal-Weight ETFs: The Quiet Signal Behind Rising Indices

Equal-weight ETFs reveal the true health of the equity market behind mega-cap-driven indices. Their gap with cap-weighted ETFs…

Smart Beta ETFs: The Hidden Risk Behind Factor Performance

Smart beta ETFs now hold ~15-20% of global equity ETF assets. Stacking factor exposures often rebuilds hidden concentration…