Monetary Policy: The Central Role of Credit Access

Monetary policy effectiveness depends less on the level of rates than on actual credit availability. Lending criteria and bank balance sheets often weigh more than funding cost.

The effectiveness of monetary policy depends less on the level of rates than on actual access to credit.

TL;DR

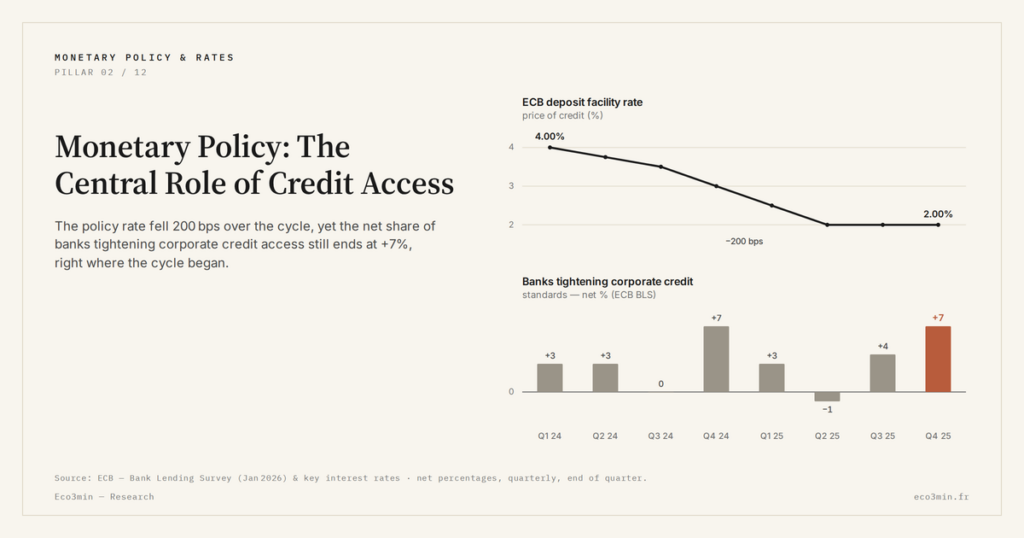

What banks actually lend weighs more than the rate they post: in Q4 2025, 18% of euro-area banks tightened corporate criteria even after three policy-rate cuts (ECB Bank Lending Survey).

- Between a central bank's refinancing rate and credit actually granted sit prudential ratios (CET1, leverage ratio), bank risk appetite and standards like France's HCSF, filters that can offset an easing.

- France's 2023-2024 housing freeze was a volume story: mortgage loans granted fell 40% from the 2022 peak to the 2024 trough (Banque de France), with HCSF caps holding debt-service at 35% and loan duration at 25 years.

- By early 2026, even with rates easing toward 3.2-3.4% (Crédit Logement/CSA), French credit production had recovered only to 60% of its 2022 level, lending criteria rather than funding cost staying the binding constraint.

The level of rates alone does not explain the real impact of monetary policy. What often matters more is the effective availability of credit. This is traced in detail in our study on the transmission of monetary policy to the real economy. When access tightens, transmission intensifies — even without an immediate change in rates. This distinction is frequently overlooked in monetary debates.

The objection comes up regularly: “rates have fallen, why isn’t credit picking up?” The question reveals a confusion between the price of credit and its availability. An attractive rate is of no use if the bank turns down the file. The real bottleneck of monetary transmission often sits in lending criteria, not in funding cost.

The price of credit is not the availability of credit

When a central bank lowers its policy rate, it cuts commercial banks’ refinancing costs. But between that refinancing cost and the credit actually distributed, several filters intervene: prudential ratios (CET1, leverage ratio), institutions’ risk appetite, internal lending criteria and regulatory standards (HCSF in France, for example).

ECB data (Bank Lending Survey, Q4 2025) show that 18% of euro area banks had still tightened their corporate lending criteria in the fourth quarter of 2025, despite three consecutive policy rate cuts. This tightening, driven by heightened risk perception and capital constraints, partly neutralised the monetary easing. Rate policy was sending an opening signal; bank balance sheets were sending a caution signal. Directly related: Our read of the way rate cycles shape corporate profitability.

The structural functioning of the banking channel in transmission explains this gap. Banks are not automatons that mechanically pass through rate variations. They assess risk, manage their balance sheet and arbitrage between profitability and exposure — decisions that may run counter to the central bank’s intended direction.

When credit disappears without rates moving

The most insidious phenomenon is quantitative credit rationing. In this case, posted rates remain stable but banks reduce the amounts granted, lengthen processing times, demand additional collateral or simply turn down files deemed too risky. This rationing is invisible in rate statistics but very real in borrowers’ experience.

France went through this between 2023 and 2024. The average mortgage rate had indeed risen, but the determining factor was the collapse in the number of loans granted: -40% in volume between the 2022 peak and the 2024 trough, according to the Banque de France. It was not the price of credit that froze the housing market — it was its rarefaction, amplified by HCSF rules capping the debt-service ratio at 35% and maximum loan duration at 25 years.

Watch the tap, not just the meter

To assess the actual effectiveness of monetary policy, credit volume indicators are at least as important as rate indicators. Monthly mortgage origination, net corporate loan flows, loan rejection rates and lending condition surveys provide a more complete picture than tracking policy rates alone.

The selective distribution of credit across borrower profiles reinforces the need to look beyond averages. A falling average rate can coexist with deteriorating credit access for the most fragile profiles — small businesses, first-time homebuyers, sectors deemed risky.

The distinction between rates and credit access is particularly visible in the French housing market in early 2026. Despite rates easing toward 3.2-3.4% (Crédit Logement/CSA), credit production has only recovered to 60% of its 2022 level. Lending criteria — not funding cost — remain the main limiting factor.

The focus on interest rates as the sole indicator of monetary policy obscures the mechanism that often determines its real effectiveness: actual credit access. The concrete diffusion of monetary impulses through the economic fabric depends on banks’ willingness and ability to lend, not only on the price at which they refinance themselves. The instruments deployed by monetary authorities — targeted refinancing operations, temporary prudential easing — are designed precisely to act on this quantitative dimension when the rate channel alone is not enough.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…