Why Expecting Quick Monetary Policy Results Is a Mistake

Monetary policy operates with cumulative and lagged effects over twelve to eighteen months. Expecting quick results leads to premature judgments and to two symmetric errors — demanding excessive tightening or prematurely loosening.

Monetary policy operates on a long timeframe, making the expectation of quick results illusory.

TL;DR

Monetary policy's attention peak falls within 48 hours of a decision; its real economic impact lands twelve to eighteen months later — a gap that breeds premature verdicts.

- The ECB notes media coverage of a rate decision peaks within 48 hours, while its economic impact peaks twelve to eighteen months later (Economic Bulletin 4/2025).

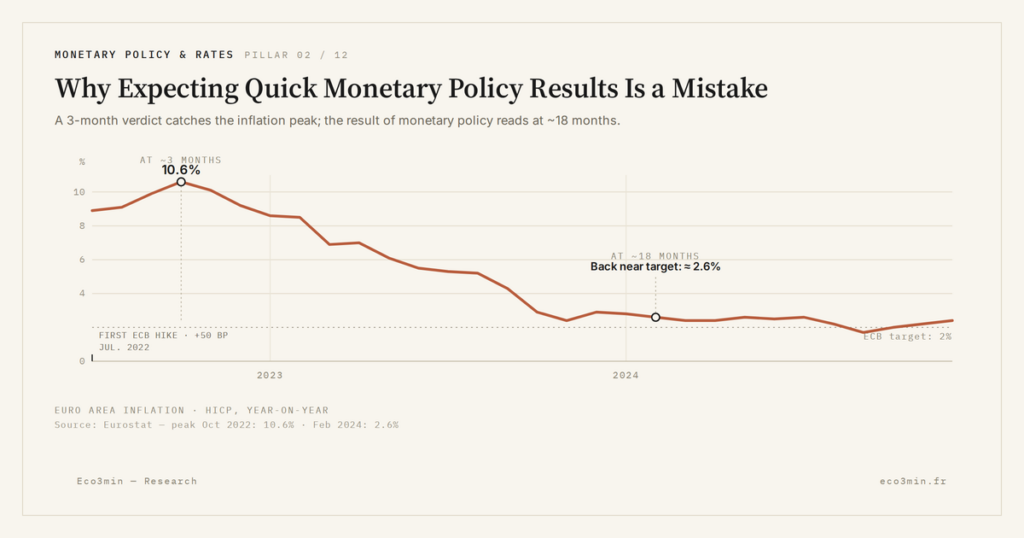

- After the ECB's first hikes in July 2022 inflation kept accelerating, feeding doubts about the strategy; two years on it had been divided by four.

- The euro-area composite PMI fell below 50 by November 2022, but GDP only neared stagnation in Q1 2023 and employment slowed only in H2 2024 (IHS Markit, December 2025).

The expectation of quick results often accompanies monetary decisions. This impatience leads observers to judge central bank action prematurely. Yet transmission rests on cumulative and lagged effects. Visible reactions do not immediately reflect the actual impact.

An immediacy bias entrenched in public debate

The information cycle imposes a tempo incompatible with that of monetary policy. Each ECB meeting generates a wave of commentary that assesses the decision against its visible effects in the days or weeks that follow. This temporal framing is unsuited: it amounts to judging a long-course medical treatment on first-day results. A related read: The Eco3min study of the profit-side response to tighter policy.

According to an ECB analysis (Economic Bulletin 4/2025), the volume of media coverage of monetary policy decisions peaks within the 48 hours following the announcement, then declines rapidly. The peak of actual economic impact, by contrast, occurs twelve to eighteen months later. This gap between the attention peak and the impact peak creates a window in which premature judgments form and crystallize. The phenomenon notably feeds the contradictory readings of markets in restrictive regimes — detailed in our analysis of the markets-versus-inverted-curve paradox.

The 2022-2024 tightening offers the most recent illustration. After the ECB’s first rate hikes in July 2022, commentators highlighted the absence of effect on inflation — which continued to accelerate. The apparent lack of short-term results fueled doubts about the strategy. Two years later, inflation had been divided by four, retrospectively validating the action taken.

Effects that accumulate before becoming visible

Monetary policy operates not in jolts but through gradual accumulation. Each rate hike marginally tightens financing conditions, modestly reduces credit demand, imperceptibly slows investment projects. These micro-adjustments are individually insignificant. It is their superposition over several quarters that produces the measurable macroeconomic effect.

This cumulative logic explains why the first signs of impact are often ambiguous. Leading indicators — PMI surveys, investment intentions, credit standards — begin to turn well before lagging indicators such as GDP or employment. According to IHS Markit data (December 2025), the euro area composite PMI had begun contracting below 50 as early as November 2022, four months after the start of tightening. But GDP only recorded its first quarter of near-stagnation in Q1 2023 — and employment only began to slow in the second half of 2024.

The errors that impatience produces

The expectation of quick results leads to two symmetric errors. The first consists of concluding too early in failure and demanding even more aggressive tightening — at the risk of triggering excessive slowdown when the cumulative effects finally materialize. The second consists of prematurely loosening monetary policy at the first signs of disinflation, without waiting for the process to consolidate.

The recurring biases that distort monetary policy analysis are amplified by this impatience. The observer who judges after three months what is playing out over eighteen does not assess monetary policy — they assess their own tolerance for uncertainty. Accepting the time of transmission is a precondition for any rigorous reading of monetary action.

Judging the effectiveness of a monetary decision over a horizon of a few weeks or months. Monetary transmission operates through gradual and delayed accumulation. Visible effects represent only the tip of a process that unfolds over one to two years. Any evaluation before that horizon is structurally incomplete.

Impatience with monetary policy is not an anecdotal psychological trait — it is a systemic bias that distorts public debate and can influence the decisions of economic agents. An investor who abandons a project because ’the rate cut has changed nothing’ after two months may miss a financing window that opens six months later. Integrating the actual timeframe of monetary transmission into one’s reasoning is not an academic exercise — it is a condition for an accurate reading of the economic situation. Central banks’ regular communication on their projection horizons aims precisely to anchor this patience in agents’ expectations.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…