Three Common Misreadings of Monetary Policy

Three recurring confusions distort the reading of monetary policy: equating announcement with impact, attributing other forces to the monetary instrument, and projecting a symmetry between hikes and cuts that the data do not support.

Recurring confusions distort the reading of monetary policy and its economic effects.

TL;DR

Three confusions recur in reading monetary policy: equating the decision with its effect, crediting policy for moves driven by other forces, and assuming a hike and a cut work symmetrically.

- Decision is not effect: a 25 basis-point ECB cut draws instant commentary on credit and real estate, yet consequences land over a twelve-to-twenty-four-month transmission, while prices repricing within minutes get mistaken for a real economic move.

- The asymmetry is quantified: ECB structural-model projections (December 2025) put a 100 basis-point cut's GDP impact at +0.3 to +0.6 points over two years, below the -0.5 to -0.9 points of a symmetric hike.

- Attribution is genuinely hard: Romer and Romer's work (updated within the NBER framework, 2024) shows isolating exogenous monetary shocks remains a major methodological challenge, so rebounds get wrongly credited to rate moves.

- Misreadings become positioning errors: an investor expecting an immediate mortgage-credit rebound after a cut, or a firm awaiting a 'clear' signal, can end up out of step with a lagged, sequential reality.

Monetary policy is often interpreted through misleading shortcuts. Confusing the decision with its effect, or the short term with cumulative transmission, leads to flawed readings. The figures are laid out in the Eco3min framework on monetary transmission channels. These biases are reinforced by the attention paid to immediate reactions. They obscure the underlying mechanisms. Identifying these errors allows for a more rigorous reading of monetary action.

Confusing the announcement with its impact

The first confusion equates the moment of the decision with the moment of the effect. When the ECB cuts its deposit rate by 25 basis points, immediate commentary focuses on expected consequences — for credit, real estate, employment. Yet those consequences materialise only at the end of a transmission process spanning twelve to twenty-four months.

This confusion is sustained by the reactivity of financial markets, which adjust asset prices within minutes. The non-specialist observer equates this market reaction with a real economic effect. The distinction between financial prices and real aggregates — output, employment, investment — is nevertheless fundamental. The impression of ineffectiveness that accompanies the first weeks after a decision stems directly from this confusion between financial and economic time horizons.

Attributing to monetary policy what stems from other factors

The second frequent error attributes to monetary policy developments that result from other forces. An employment rebound after a rate cut may stem from fiscal factors, a favourable supply shock or an inventory restocking cycle. Isolating the strictly monetary effect is a complex econometric exercise that everyday commentary bypasses through causal shortcuts.

The work of Christina Romer and David Romer (updated within the NBER framework, 2024) shows that identifying exogenous monetary shocks remains a major methodological challenge. The error of expecting fast and directly attributable results amplifies this bias: unable to isolate the monetary effect, the observer conflates it with the broader macro environment.

Projecting a symmetry that does not exist

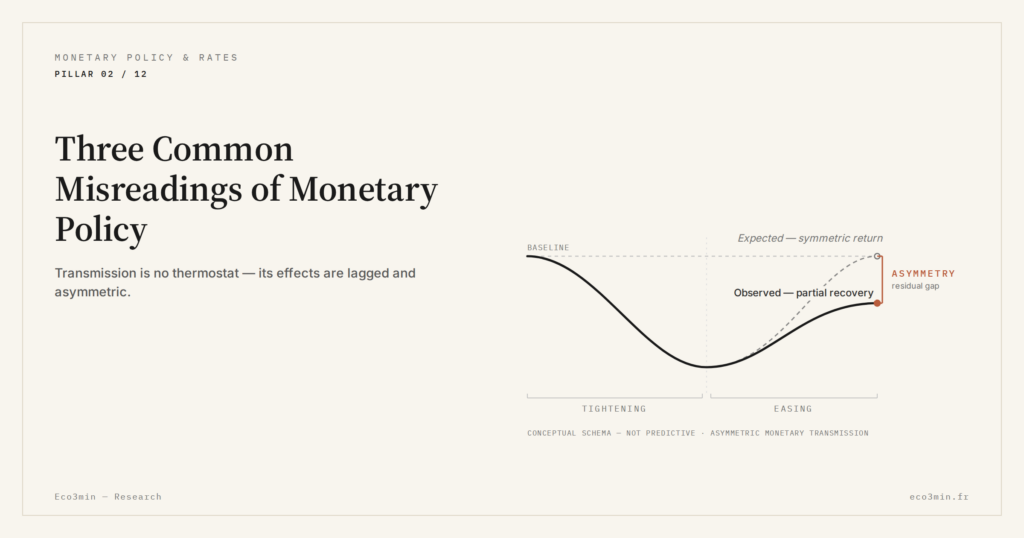

The third confusion rests on an implicit assumption of symmetry: if a 100 basis-point hike slows activity by X%, a cut of the same magnitude should stimulate it by as much. This reading ignores the non-linearities documented in monetary transmission. Contraction mechanisms — defaults, credit rationing, loss of confidence — do not reverse mechanically when rates come back down.

According to ECB estimates (structural macro model, December 2025 projections), the impact of a 100 basis-point rate cut on euro area GDP was estimated at between +0.3 and +0.6 percentage points over two years — markedly below the estimated contractionary impact of a symmetric hike, put at between -0.5 and -0.9 percentage points. This asymmetry, well established in the academic literature, remains widely ignored in market projections.

The effective restoration of liquidity conditions after a tightening cycle is not enough to revive the credit and investment dynamics destroyed in the restrictive phase. Damaged balance sheets, eroded confidence and abandoned projects do not rebuild at the pace of rate cuts.

Reading monetary policy like a thermostat: turn it up to cool, turn it down to warm. This mechanical metaphor masks the complexity of a system in which transmission lags, thresholds and asymmetries produce non-linear effects. The same monetary move can have very different consequences depending on the state of the financial system at the time it is taken. This thread is picked up in our examination of how earnings absorb a shift in rates.

From reading errors to positioning errors

These confusions are not merely intellectual. They translate into concrete positioning errors. An investor anticipating an immediate rebound in mortgage credit after a rate cut may find themselves out of step with market reality. A company postponing an investment while waiting for a “clear” monetary signal may miss a favourable financing window.

The intrinsically lagged nature of monetary transmission calls for a patient, sequential reading incompatible with the rhythm of cyclical commentary. Central bank communication seeks precisely to reduce these confusions by making its own transmission horizons explicit — but the message runs into simplified interpretive frames that persist.

Last updated — 7 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…