Monetary Transmission: Rates, Credit, Expectations

Monetary policy never operates through a single lever. Rates, credit, asset prices, FX and expectations propagate at distinct speeds, producing a transmission that is fragmented and at times incomplete.

Monetary policy does not transmit through a single channel but through a network of interdependent mechanisms within the rate cycle. Rates, credit, asset prices, FX and expectations diffuse monetary impulses at different speeds, producing a fragmented and at times incomplete transmission.

TL;DR

The euro area's rate cuts are reaching mortgages and equities while bank credit and cross-country spreads lag, exposing a transmission that runs at several speeds at once in early 2026.

- ECB statistics (December 2025) show new euro area mortgage rates easing toward roughly 3.2% from a 4.1% mid-2024 peak, yet the Germany-Italy gap topped 80 basis points.

- The ECB Bank Lending Survey (Q4 2025) recorded a tentative easing of corporate credit standards after eight consecutive quarters of tightening, a filter that can blunt rate cuts whatever the policy direction.

- Channels fire at different speeds, from hours for expectations to quarters for credit; European equities had already advanced about 12% (Euronext, January 2026) ahead of any confirmed real-economy recovery.

Understanding this architecture is essential to read the lags between central bank decisions and observed macroeconomic effects. Each channel has its own timing, its sensitivity to private balance sheets and its dependence on the prevailing macro-financial regime.

Monetary policy diffuses through several distinct channels with differentiated paces and macroeconomic effects.

Monetary policy never operates through a single lever. Interest rates, credit, asset prices, exchange rates and expectations are distinct yet interdependent transmission channels. Each has its own timing and its own sensitivity to the macro-financial context. Confusion often arises from a uniform reading of these channels, as if they produced simultaneous effects.

The central feature lies in their interdependence. A disruption in the credit channel alters the reach of the interest rate channel. A de-anchoring of expectations partially neutralises the effects of tightening. Related reading: The decomposition of the earnings response to a rate regime shift. In early 2026, this cross-cutting dimension takes on new importance: the rate cuts initiated by the ECB and the Fed are not transmitting uniformly across all transmission vectors. The full transmission mechanism, its lags and its heterogeneities is documented in the Eco3min study on monetary transmission lags and heterogeneities.

The interest rate channel: most visible, not the fastest

The most commonly identified channel links policy rates to market rates, and then to financing conditions in the real economy. An increase in the ECB’s refinancing rate first propagates to interbank rates (Euribor, €STR), then to bond yields and finally to rates offered to end borrowers — households and firms.

According to ECB monetary statistics (December 2025), the average rate on new euro area mortgages had begun to ease toward ≈3.2%, down from a peak of ≈4.1% reached in mid-2024. But this decline did not transmit uniformly: the gap between rates in Germany and Italy exceeded 80 basis points, signalling that financial heterogeneity within the euro area distorts monetary propagation.

Bank credit: a filter, not an automatic relay

The credit channel introduces a decisive layer of intermediation. Commercial banks do not simply pass on rates; they simultaneously adjust their lending standards, volumes and risk appetite. The balance sheet structure of the banking sector shapes the effective reach of monetary policy beyond what the rate level alone can explain.

The ECB Bank Lending Survey (Q4 2025) indicated a tentative easing of credit standards on corporate loans, after eight consecutive quarters of tightening. This gap between the direction of policy rates and actual bank behaviour illustrates the friction specific to this channel. The dynamics of financial conditions and available liquidity act here as an intermediate transmission belt that is often underestimated.

Expectations and asset prices: transmission through minds

A third vector operates even before rates move. The influence of expectations on the path of monetary policy manifests through the behaviour of financial markets, which adjust valuations and yield curves based on signals sent by central banks.

The asset price channel operates in parallel. When rates fall, equity and real estate valuations tend to rise, generating a wealth effect that supports consumption and investment. According to Euronext indices (January 2026), European equity markets had advanced by around 12% since the start of the easing cycle, embedding recovery expectations that the real economy had yet to confirm.

Some current assessments favour the hypothesis of fast and complete transmission. Yet empirical work from the BIS (Annual Report 2025) suggests that the expectations channel can also create a durable decoupling between the financial and productive spheres if credit conditions do not follow the move in rates.

The exchange rate: an open but unstable channel

The final significant vector runs through the FX market. A rate differential between currency areas alters relative currency values, which in turn affects export price competitiveness and import costs. This channel is particularly sensitive to capital flows and speculative movements, making it more volatile than the previous ones.

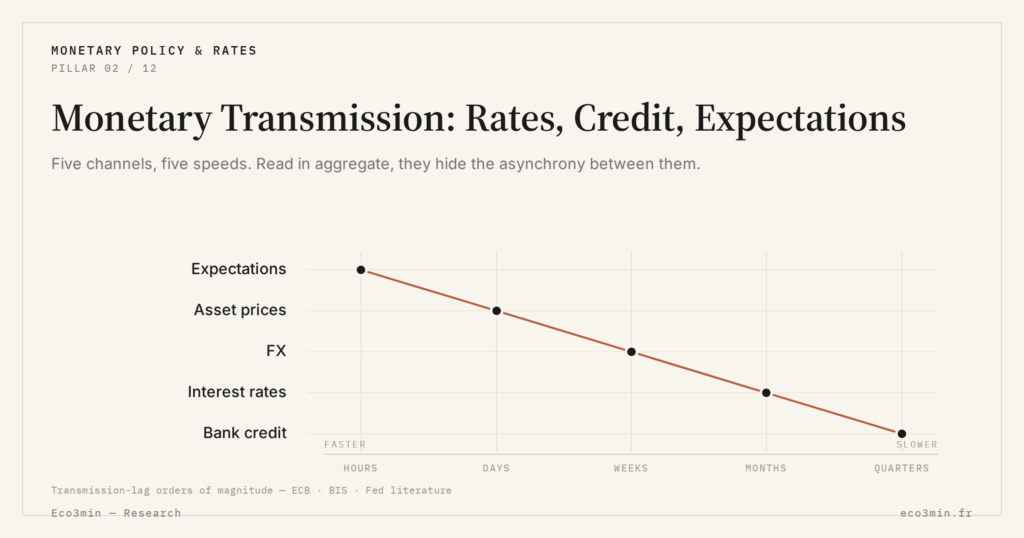

The structural lags separating monetary action from its real effects vary substantially across channels. The expectations channel can act within hours, the FX channel within weeks, the credit channel across multiple quarters. This asynchrony explains why a global reading of transmission often gives a misleading picture of its real effectiveness.

- Monetary policy propagates through at least five distinct channels: interest rates, bank credit, expectations, asset prices and exchange rates.

- Each channel has its own timing: from a few hours for expectations to several quarters for credit.

- The interaction between channels alters their respective effectiveness: a credit blockage can neutralise the effect of even a significant rate cut.

Reading monetary transmission as a mere movement of policy rates underestimates the complexity of the system. The toolkit deployed by monetary authorities simultaneously targets several of these channels, but their respective responsiveness depends on structural factors — banking health, market depth, institutional credibility — over which the central bank has only indirect control.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…