MORTGAGE30US Explained: Meaning, Freddie Mac PMMS Calculation, Weekly Release

The most-cited U.S. mortgage rate, MORTGAGE30US, is a weekly aggregate Freddie Mac has built since April 1971 from a survey of national lenders. What it means depends as much on the standardized product underlying it as on the survey methodology.

TL;DR

MORTGAGE30US, Freddie Mac's weekly benchmark since April 1971, reports an offered rate on a tightly standardized prime loan, sitting below what the average U.S. borrower actually pays.

- It is an offered rate, not a contracted one, and excludes origination points, lender fees, and PMI; the all-in APR therefore runs systematically higher, historically by 20–40 bp.

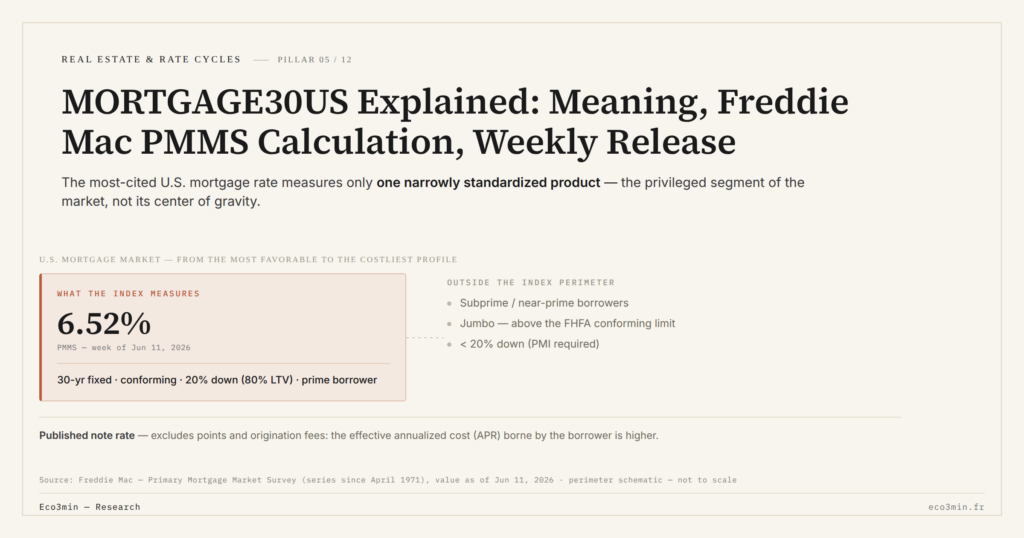

- Built from the PMMS, a Monday–Wednesday lender survey published Thursday at noon, it prices one product (30-year fixed, conforming, 80% LTV, prime, FICO above 740) and ignores subprime borrowers, who pay 100–300 bp more.

This article isolates the definition and the measurement mechanics of the instrument, leaving spread decomposition and historical level interpretation to other satellites in the cluster.

What MORTGAGE30US actually measures

MORTGAGE30US is the “30-Year Fixed Rate Mortgage Average in the United States,” published weekly by Freddie Mac since April 1971 and distributed through FRED by the Federal Reserve Bank of St. Louis. The data represents the average interest rate offered in the U.S. on a standardized mortgage product: 30-year fixed-rate loan, conforming to the lending limits of the government-sponsored enterprises Fannie Mae and Freddie Mac, with a prime-quality borrower.

What MORTGAGE30US is must be distinguished from what it is not. It is an offered rate, not a contracted rate. Lenders report the conditions they publicly advertised during the survey window, not the average rate actually signed on closed loans that same week. The difference is subtle but material: a lender may quote 6.80% while closing loans at 6.60% (with discount points purchased) or 7.00% (without points) depending on per-borrower negotiation.

The other critical distinction: MORTGAGE30US is not the all-in cost for the borrower. The published rate excludes origination points, lender fees, private mortgage insurance where applicable, and processing costs. For this reason, the effective annualized cost (APR) is systematically higher than MORTGAGE30US, typically by 20 to 40 basis points depending on borrower profile.

In short, the instrument is a market reference that allows comparison of financing conditions across periods, not an indicator of the effective cost borne by any individual borrower. To understand the rates-to-purchasing-power mechanic in full, MORTGAGE30US must be read as a proxy for the financing envelope available, not as the final invoice.

The PMMS — Freddie Mac methodology

MORTGAGE30US is derived from the Primary Mortgage Market Survey (PMMS), a weekly poll Freddie Mac has conducted since 1971. Each Monday through Wednesday, the institution surveys a sample of mortgage lenders active across the U.S. — typically national banks, credit unions, and specialized mortgage banks. Respondents report the conditions they offered during that three-day window for a precisely defined product.

The release lands every Thursday at noon Washington time (17:00 UTC in winter, 16:00 UTC in summer). The published figure therefore reflects the conditions of the first half of the same week. This cadence and time window create a slight lag: MORTGAGE30US released on Thursday, May 15, 2026 reflects the yields offered Monday May 12 through Wednesday May 14, not the Thursday itself. During periods of elevated volatility — around an FOMC meeting, for instance — the data may appear one to two days behind the MBS secondary market and the 10-year Treasury.

The composition of the surveyed lender panel is not fully public, but Freddie Mac states that respondents are selected to represent a reasonable geographic and institutional mix of the national market. This partial opacity is one source of debate about the representativeness of the index: large national lenders are mechanically overweighted relative to smaller regional lenders, who may offer different terms.

For the live data series, the FRED MORTGAGE30US weekly dataset aggregates the entire history since April 1971, with no major methodological discontinuity.

The standardized product: conforming, 80% LTV, prime

The product surveyed by the PMMS is not a generic mortgage but a narrowly defined one. Three cumulative characteristics apply.

First, it is a conforming loan. The principal amount stays under the annual cap set by the Federal Housing Finance Agency (FHFA) — the cap that determines whether the loan can be securitized by Fannie Mae or Freddie Mac. In 2024, the conforming cap for a single-family home in most of the country stood around $766,550 (above that level, the loan becomes a jumbo, which follows a distinct market with its own rates). The cap is adjusted every November for the following year, in line with the trajectory of home prices.

Second, the implicit loan-to-value (LTV) ratio is 80%. The borrower puts 20% of the purchase price down in cash, removing the requirement for private mortgage insurance (PMI). A borrower with higher LTV — say 95% — pays a different rate, because the default risk is higher and PMI adds cost.

Third, the surveyed borrower is prime: high FICO score (typically above 740), moderate debt-to-income ratio, clean credit history. Subprime and near-prime borrowers access materially higher rates — sometimes 100 to 300 basis points above MORTGAGE30US — that are not reflected in the index.

This triple standardization explains why the rate published by MORTGAGE30US is consistently lower than the average rate actually contracted across the full U.S. market. The PMMS measures the privileged segment of the market, not its center of gravity.

What the rate excludes, and why it matters

MORTGAGE30US is a note rate — the contractual nominal interest rate on the loan. Three components are systematically excluded.

First, origination points. One point equals 1% of the principal, paid upfront by the borrower to obtain a lower rate over the life of the loan. On a $400,000 loan, one point costs $4,000 cash at signing and typically reduces the rate by 25 basis points. Borrowers who buy down their rate effectively pay a cost above MORTGAGE30US once the point is amortized over the loan’s life. Related reading: interest rates and real-estate purchasing power.

Second, origination fees (origination, application, underwriting, title insurance, appraisal). These costs can represent 2 to 5% of the principal depending on jurisdiction and lender.

Third, private mortgage insurance where applicable (PMI), excluded by construction since the standardized product is defined at 80% LTV.

The gap between MORTGAGE30US and the APR — which annualizes all these costs — historically runs between 15 and 40 basis points. The gap widens during phases of elevated origination costs or expanding bank margins. For this reason, reading MORTGAGE30US at 6.80% as “the cost of borrowing in May 2026 in the U.S.” consistently understates the real cost.

Reading conventions and instrument limits

Three reading conventions should be internalized.

First, MORTGAGE30US exists as an uninterrupted weekly series since April 2, 1971, with no major methodological revision. This continuity is rare for a U.S. financial indicator — most comparable series have undergone at least one definitional revision. For the major 30-year rate cycles since 1971, this historical depth is one of the instrument’s principal strengths.

Second, MORTGAGE30US should be read alongside the 10-year Treasury (DGS10). The mortgage rate level alone carries limited information without context on the underlying risk-free yield. The difference — known as the mortgage-Treasury spread — captures the risk premia specific to the mortgage market. The spread decomposition versus the Treasury is treated in detail in the dedicated cluster satellite.

Third, MORTGAGE30US captures a U.S. institutional anomaly. No other major housing market globally offers a standardized 30-year fixed-rate product with an asymmetric refinance option for the borrower. This product, created in the 1930s under the impulse of the Federal Housing Administration, structures today the near-totality of the U.S. market and has no direct equivalent in Europe. The historical anomaly of the U.S. 30-year fixed (created by the FHA in 1934) deserves separate institutional treatment to understand why the PMMS itself has no direct European peer.

On limits, two points should be kept in mind. First, the PMMS sample remains partially opaque in its composition, which makes strict representativeness audit difficult. Second, the weekly publication is smoothed by construction and does not capture intra-week moves in the MBS secondary market, which reacts in real time to macro announcements.

- MORTGAGE30US is an offered rate, not a contracted rate; it excludes points, fees, and insurance, and therefore systematically understates the all-in cost for the borrower.

- The PMMS surveys a sample of national lenders Monday through Wednesday, publishes Thursday at noon, and covers a standardized product: 30-year fixed, conforming, 80% LTV, prime borrower.

- The instrument captures the privileged segment of the market, not its center of gravity; subprime borrowers access rates 100 to 300 bp higher that are not reflected.

- Read alone, the mortgage rate level carries limited information; it takes meaning relative to the 10-year Treasury, and within the macro frame of housing affordability.

Why this mechanic matters for what follows

Understanding the definition of MORTGAGE30US conditions any subsequent macro reading of the instrument. A quick interpretation that conflates the published rate with the effective cost of borrowing leads to repeated reasoning errors — on monetary policy transmission, on the elasticity of the housing market to policy rates, on historical cycle comparison. The instrument’s pedagogy is the mandatory upstream of any deeper analysis.

For the macro reading, MORTGAGE30US is only an entry point. How mortgage rates have structured affordability since 1971 remains the central analytical frame: across 54 years of data, the instrument allows decomposing the evolution of housing affordability between the contribution of rates and that of home prices themselves — an exercise that only makes sense with a continuous, comparable, methodologically stable series.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →US Rental Property Real Yield: What Cap Rate and NOI Actually Leave You

A rental listing leads with a yield. Divide the annual rent by the price and the number looks…

Cap Rate Spread: What Rental Yield Pays Over the 10-Year Treasury

A 5% cap rate sounds attractive. But 5% against what? A risk-free 10-year Treasury yields near 4.5% in…

US Rental NOI, Line by Line: What Net Operating Income Really Subtracts

A US rental yield is advertised gross: annual rent over price. Between that number and the income an…