MORTGAGE30US vs DGS10: What the Spread to the Treasury Reveals About Mortgage Risk

The MORTGAGE30US level says little without its distance to the 10-year Treasury. The spread, averaging around 170 basis points since 1971, breaks down into three premia — prepayment, rate volatility, MBS liquidity — making this gap the real diagnostic tool for U.S. mortgage financing conditions.

TL;DR

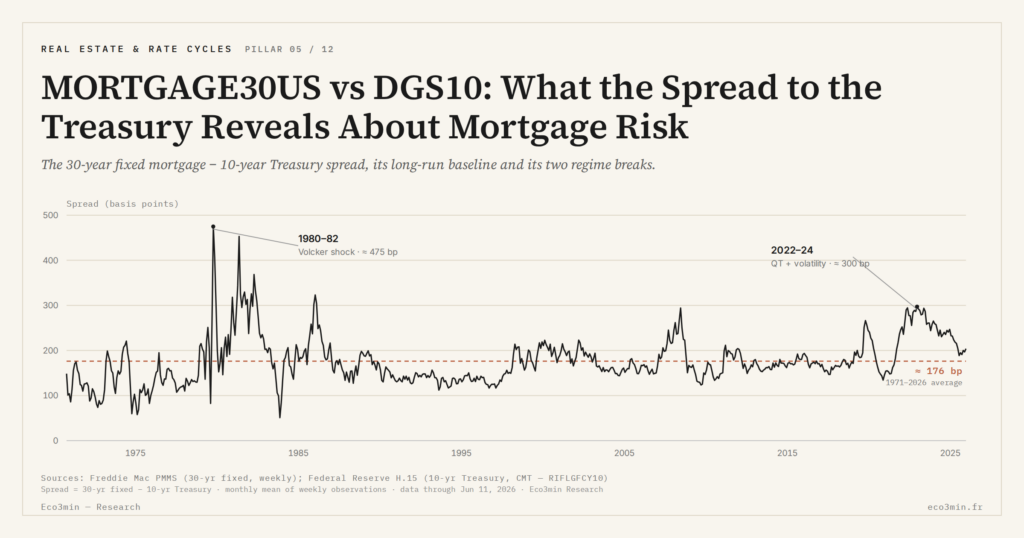

The MORTGAGE30US-to-Treasury spread sat within 30 bp of its 170 bp average about 60% of the time since 1971; the larger moves concentrate in regime shifts and credit stress.

- The prepayment premium funds the U.S. borrower's option to refinance at par when rates fall (the negative convexity of MBS); it can fall below 50 bp in calm markets or exceed 100 bp in volatile ones.

- The rate-volatility premium tracks the MOVE index, which hit 199 in March 2023 during the U.S. regional-banking crisis, its highest reading since 2009.

- The Fed held over $2.7 trillion of agency MBS at its 2022 peak; its quantitative-tightening exit leaves price-sensitive marginal buyers and sustains a wider liquidity premium than before 2022.

- On outstanding loans, average rates sit well below the prevailing MORTGAGE30US after the 2020-2021 refinancing window, deactivating the prepayment option for the typical borrower even as new MBS still price it.

This article isolates the mechanics of the MORTGAGE30US – DGS10 spread without re-litigating full Fed-to-mortgage transmission, treated separately in the cluster.

Why the mortgage rate level alone is largely uninformative

Reading MORTGAGE30US at 6.80% without context is like reading a thermometer without knowing whether it is sunny or raining outside. The same mortgage rate level can result from radically different configurations: a low 10-year Treasury with widened spread (signal of stress in the mortgage market), or an elevated Treasury with compressed spread (signal of restrictive Fed policy transmitting normally). Without decomposition, the interpretation remains ambiguous.

Consider two configurations that both produce a mortgage rate of 6.80%. In the first, the 10-year Treasury sits at 4.40% and the spread at 240 basis points. In the second, the 10-year sits at 5.10% and the spread at 170 bp. These two states of the market have nothing in common analytically. The first signals a mortgage market under structural stress despite an accommodative or neutral Fed policy. The second signals a restrictive Fed policy properly transmitted through the risk-free yield channel, with the mortgage market in normal condition. Further reading: our sub-pillar on rates and mortgage capacity.

This distinction is not theoretical. Across 2022-2024, the spread oscillated between 230 and 280 basis points — well above its historical average. Reading the mortgage rate at 7.79% in October 2023 as “the consequence of Fed hikes” missed the essential point: a significant portion of the level came from the spread itself, not from the underlying Treasury. To situate this mechanic within the broader macro frame, the rates-vs-prices decomposition over 54 years measures what rates actually contributed to housing affordability.

The historical spread: 170 bp as baseline, with significant excursions

The average MORTGAGE30US – DGS10 spread over the long run stands around 170 basis points, with marked phases of compression and widening. This average masks considerable dispersion: the empirical standard deviation over 1971-2024 exceeds 50 basis points, with crisis-episode extremes above 300 bp.

The most durable compression phase covers 2003-2004, when the spread fell to around 130 basis points. This compression coincided with a low rate-volatility environment and structurally strong demand for MBS from the government-sponsored enterprises themselves, in a mortgage-market expansion that preceded the great financial crisis.

The most extreme widening phase in fifty years covers 2022-2024, with the spread durably above 240 basis points and peaks beyond 280 bp. Three factors stack into this widening: the Fed’s gradual exit as structural MBS buyer under quantitative tightening, the explosion of rate volatility tied to uncertainty about the policy path, and the prepayment premium that deteriorated as borrowers from the 2020-2021 cohorts found themselves locked in at historically low rates.

These historical excursions matter because they provide a reference frame: a 170 bp spread is normal, 130 bp compressed, 240 bp widened. Without this reference, the absolute figure remains mute. Empirically, on the 1971-2024 window, the spread spent roughly 60% of weekly observations within ±30 bp of the 170 bp baseline. Excursions beyond ±50 bp are concentrated in episodes of policy regime change or credit stress.

The prepayment option that the U.S. borrower holds on a 30-year fixed mortgage is an institutional feature specific to the U.S. market. This option has a measurable economic value, and it is the MBS investor who funds it through a premium demanded on the security’s yield. Related Q&A: how the 30-year rate steers US housing.

Mechanically, when rates fall, the borrower refinances and repays the principal at par. The investor recovers cash in an environment where reinvestment rates have become lower — the negative convexity characteristic of MBS. When rates rise, the borrower does not refinance, extending the security’s duration in an environment where the investor would prefer cash returns to accelerate. This asymmetry is unfavorable to the holder, who therefore demands a premium.

The size of this premium varies with expected rate volatility. In a stable-rate environment (for instance 2017-2019), the prepayment premium can fall below 50 basis points. In a high-volatility environment (2022-2024), it can exceed 100 basis points on its own. The option has more value — and therefore more cost passed to the borrower ultimately — when rate moves are uncertain.

An additional twist applies to the 2024-2026 regime specifically: the average mortgage rate on outstanding loans in the U.S. sits well below the prevailing MORTGAGE30US, because many cohorts refinanced or originated during the 2020-2021 ultra-low-rate window. This rate gap deactivates the prepayment option for the average outstanding borrower, which paradoxically reduces effective convexity risk for newly issued MBS — but the market still prices the prepayment premium based on the option’s value at issuance, not at the cohort level.

Distinct from but correlated with the prepayment premium, the rate volatility premium compensates uncertainty about the 10-year Treasury path itself. It is measured through Treasury options (MOVE index), which capture implied volatility in the bond market.

When uncertainty about Fed policy is low — as during the post-GFC forward-guidance phase (2012-2015) — this premium compresses. When uncertainty is high — as during the aggressive hiking phase of 2022-2023, when the market revised its pivot expectations at every CPI release — it explodes. In 2022-2023, the MOVE index touched 199 points in March 2023 during the U.S. regional banking crisis, its highest reading since 2009.

This volatility premium adds to the prepayment premium in the observable spread. The two being correlated (high-volatility periods are also those where the prepayment option has the most value), they are difficult to separate empirically. But conceptually, they capture two distinct dimensions of the risk borne by the MBS investor.

The third element of the decomposition is less visible but material: the MBS market liquidity premium and bank originator margins. The MBS market, though vast (around $12 trillion outstanding in 2024 per SIFMA), can experience liquidity-stress phases that widen the gap between the yield demanded by ultimate investors and the rate the banking system can offer to borrowers.

The Fed was the dominant structural buyer of MBS during the QE phases (2008-2014 then 2020-2022), absorbing several trillion dollars of outstanding stock on its own. At its 2022 peak, the Fed held more than $2.7 trillion of agency MBS on its balance sheet. Its gradual exit through quantitative tightening — started in 2022 and still ongoing in 2026 per FOMC communications — leaves marginal buyers (commercial banks, REITs, bond funds, overseas investors) with less elastic appetite for MBS, sustaining a higher liquidity premium than before 2022.

Bank margins enter as a complement. When commercial banks face tighter regulatory constraints on their MBS exposure, or higher funding costs, they pass these costs onto the mortgage rate offered to the borrower. The shift in MBS holder composition since 2022 also matters: banks themselves, after the 2023 regional banking episode, materially reduced their appetite for long-duration MBS, leaving the marginal buyer further out on the credit and duration curve. The sub-pillar on mortgage financing conditions details how these frictions transmit into the final cost for the borrower. For the live spread series, the FRED mortgage spread dataset tracks the full history.

Combined reading: same mortgage rate, two different stories

Return to the opening example. A mortgage rate at 6.80% with the 10-year Treasury at 4.40% and spread at 240 bp tells a story of an MBS market under structural stress: elevated prepayment premium (2020-2021 cohorts locked at 3%), elevated volatility premium (Fed-path uncertainty), elevated liquidity premium (Fed exit from MBS). The same mortgage rate at 6.80% with Treasury at 5.10% and spread at 170 bp would tell a story of restrictive Fed policy properly transmitted by a normal-condition mortgage market.

For the macro analyst, the implication is clear: tracking only MORTGAGE30US provides very partial information. Tracking the pair (MORTGAGE30US – DGS10, DGS10) provides the decomposed information and identifies where the move came from. This reading frame applies to reading the spread in the 2024-2026 regime where Fed-to-mortgage transmission is manifestly impaired.

For the raw mechanics of the published figure and its measurement conventions, the Freddie Mac definition of the headline rate remains the mandatory upstream of any spread reading.

Many interpret a mortgage rate at 6.80% as a direct signal of Fed policy stance. This reading conflates the mortgage rate (composite) with the 10-year Treasury (underlying risk-free), and obscures the spread’s own contribution from mortgage risk premia. The correct reading always tracks the pair (spread, Treasury) rather than the mortgage rate alone.

Why the spread is the primary diagnostic tool

Spread decomposition is not a technical refinement reserved for MBS analysts. It is the central diagnostic tool for anyone trying to understand U.S. mortgage financing conditions at a given point in time. The spread level relative to the 170 bp historical average immediately indicates whether the MBS market is in normal, compressed, or widened condition. A deviation of more than 50 bp from this baseline deserves explanation through decomposition into prepayment, volatility, and liquidity premia.

This paired reading (MORTGAGE30US, DGS10) with spread decomposition is the analytical upstream of broader questions on affordability, transaction volumes, and housing price formation — all dimensions treated separately in the cluster and in the real-estate pillar.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →US Rental Property Real Yield: What Cap Rate and NOI Actually Leave You

A rental listing leads with a yield. Divide the annual rent by the price and the number looks…

Cap Rate Spread: What Rental Yield Pays Over the 10-Year Treasury

A 5% cap rate sounds attractive. But 5% against what? A risk-free 10-year Treasury yields near 4.5% in…

US Rental NOI, Line by Line: What Net Operating Income Really Subtracts

A US rental yield is advertised gross: annual rent over price. Between that number and the income an…