MORTGAGE30US 1971-2026: A Typology of the Major 30-Year Rate Cycles

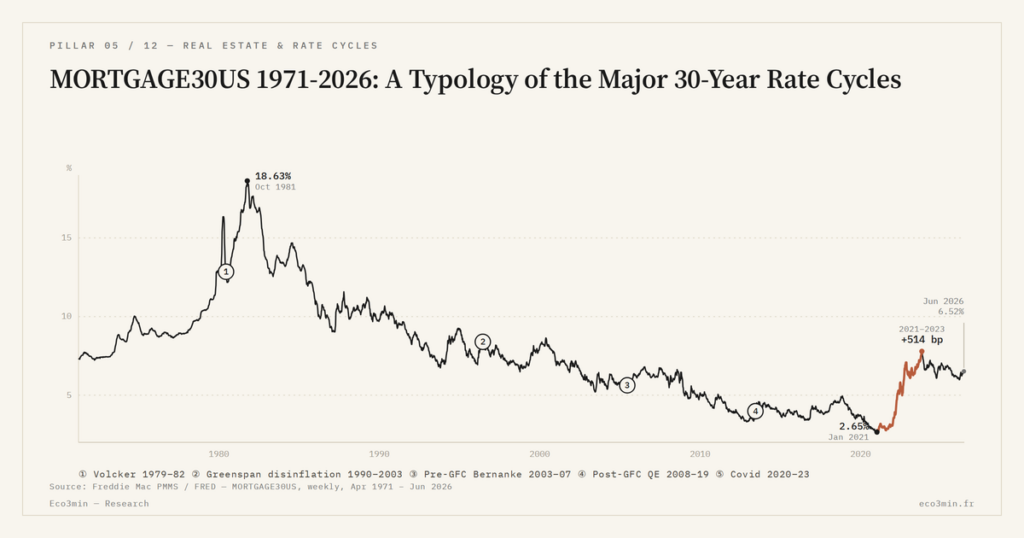

Five major cycles structure the MORTGAGE30US history since its 1971 inception: Volcker, Greenspan disinflation, pre-GFC Bernanke, post-GFC QE, COVID. Each has its trigger — monetary policy, inflation shock, financial crisis, pandemic — and a characteristic duration.

TL;DR

The 2021-2023 jump of 514 bp, from 2.65% to 7.79% in under three years, outpaces every prior MORTGAGE30US move since 1971, including the Volcker spike.

- Five cycles since 1971, each with its own trigger: the Volcker monetary shock, the Greenspan secular decline, the opaque pre-GFC Bernanke stability, the administered post-GFC QE compression, and pandemic-era COVID volatility.

- The 18.45% October 1981 peak and 2.65% January 2021 trough bound a 1,580 bp range; the series spends about 80% of its history between 4% and 9%.

- The 2020-2021 cohorts now sit more than 400 bp below MORTGAGE30US, the largest cohort gap in the series, which mechanically freezes part of the existing-home transaction pool for years.

This article maps the cycles, their triggers, and durations, leaving transmission into housing prices to the macro hub frame and to the credit-cycle satellite.

Five cycles structure fifty-five years of history

Between April 1971 — the first weekly PMMS release — and May 2026, the MORTGAGE30US series spans fifty-five years with no major methodological discontinuity. Across this window, the total amplitude is considerable: a minimum of 2.65% in January 2021, a maximum of 18.45% in October 1981, a 1,580 basis-point range. No other Western mortgage series matches this historical depth.

Five major cycles emerge from the raw reading. The Volcker cycle (1979-1982) peaks at levels never reproduced since. The Greenspan disinflation (1990-2003) gradually pulls the rate toward 5-6%. The pre-GFC Bernanke cycle (2003-2007) stabilizes it around 6% before the collapse. The figures are laid out in our framework for disinflationary phases. The post-GFC QE phase (2008-2019) durably compresses the rate between 3.5 and 5%. The COVID and post-COVID phase (2020-2023) delivers the steepest amplitude in fifty years. Each cycle has its own trigger and a distinct temporal signature. Related analysis: the March 2020 regime break.

The Volcker cycle (1979-1982): exiting inflation at any cost

When Paul Volcker took the Fed chair in August 1979, U.S. inflation exceeded 11% and MORTGAGE30US stood around 11%. The Volcker decision — shifting operational target from interest rates to money supply — triggered historic rate volatility. MORTGAGE30US crossed 15% in April 1980, briefly fell back to 12.2% in summer 1980, then rose above 17% from October 1981 onward. On that specific point, the borrowing-capacity mechanism that precedes price serves as the reference. The absolute peak of the series, 18.45%, was hit in October 1981. Our breakdown of Volcker’s rate-peak policy analyses its mechanics. On the same theme: the mortgage-capacity mechanism of rates.

At these levels, home ownership required pre-purchase savings rates and debt-to-income ratios with no modern equivalent. Transaction volumes collapsed: new home sales fell more than 50% between 1978 and 1982 per Census Bureau data. The Volcker disinflation — brutal and costly in unemployment terms (10.8% in November 1982) — nonetheless delivered the intended effect: MORTGAGE30US fell below 14% by end-1982 and entered a secular decline that would cover the following twenty-two years.

The Greenspan disinflation (1990-2003): gradual return to mean

The 1983-1989 period serves as transition. Under Volcker’s extended chairmanship and Greenspan from August 1987 onward, MORTGAGE30US oscillates between 9% and 12%, in a disinflation environment already anchoring. The 1990-1991 recession marks the inflection point: MORTGAGE30US falls below 10% in 1991 for the first time since 1978, and enters a regular slide.

Between 1992 and 2003, the decline is slow but durable. The rate touches 6.49% in October 1998 (its lowest reading since 1968), temporarily climbs to 8.52% in May 2000 under Fed tightening ahead of the dot-com peak, then falls back to 5.21% in June 2003. This secular decline reflects the durable anchoring of inflation around 2-3%, the compression of the Treasury term premium, and the maturation of the MBS market that compresses risk premia. Related series: the 10-year term-premium series.

The period is also the structural expansion of the U.S. mortgage market: outstandings grow, securitization generalizes, and the government-sponsored enterprises Fannie Mae and Freddie Mac see their secondary-market footprint expand. For how mortgage credit transmits beyond the rate itself, how mortgage credit cycles transmit into housing prices is the dedicated satellite. A companion question: the 30-year fixed mortgage and US housing.

The pre-GFC Bernanke cycle (2003-2007): stability before the rupture

Between 2003 and 2007, MORTGAGE30US trades in a narrow corridor between 5.2% and 6.8%. It is the most stable period of the series since inception. This apparent stability masks an accumulation of fragilities: rapid subprime credit expansion, underpricing of default risk, opacity of private-label securitization structures.

Under Ben Bernanke’s chairmanship (succeeding Greenspan in February 2006), MORTGAGE30US continues to oscillate within this corridor until the crisis triggers. The rupture arrives in 2008: between January and December, the rate moves from 5.76% to 5.29% with historic internal volatility. The financial system as a whole is under extreme stress; massive Fed MBS purchases from November 2008 onward — the first QE — would then force rapid compression.

The post-GFC QE phase (2008-2019): durable compression

From 2009 to 2019, MORTGAGE30US trades between 3.3% (low reached in November 2012) and 5% (high reached in November 2018). The post-crisis phase is characterized by durable rate compression combining three factors: near-zero Fed funds from December 2008 to December 2015, massive Fed MBS purchases across three successive QE rounds (QE1 late 2008, QE2 late 2010, QE3 2012-2014), and persistent low inflation.

This compression makes mortgage credit historically cheap for prime borrowers, and supports a recovery in U.S. home prices that surpasses pre-crisis levels by 2017 per the S&P CoreLogic Case-Shiller index. The phase also sees the private-label securitization industry nearly disappear, leaving Fannie Mae and Freddie Mac (and Ginnie Mae) absorbing virtually all the flow of new conforming MBS issuance.

The Fed tightening cycle started in late 2015 gradually pushes MORTGAGE30US higher, touching 4.94% in November 2018. The dovish Fed pivot in early 2019 quickly pulls the rate back below 4% by H2 2019. For the macro implications across this stretch, mortgage credit and broader financial cycles situates the period within the broader financial-cycle frame.

The COVID and post-COVID phase (2020-2023): the steepest amplitude in fifty years

March 2020 opens the most volatile phase in MORTGAGE30US history. The abrupt U.S. economic shutdown and the monetary policy response — Fed funds back to zero on March 15, 2020, massive QE redeployment with Treasury and MBS purchases — compress MORTGAGE30US to unprecedented levels. The rate crosses 3% in July 2020, then 2.80% in December 2020, and hits its historical low of 2.65% in January 2021. This compression coincides with a massive refinance wave: per Freddie Mac, around 14 million loans were refinanced between 2020 and 2021.

The exit from this compression is brutal. From March 2022 onward, the Fed begins its aggressive hiking cycle. MORTGAGE30US follows with short lag: 4% crossed in March 2022, 6% in September 2022, 7% in October 2022, partial retreat in early 2023, then renewed upward break to reach 7.79% in October 2023. That is the highest since November 2000.

The amplitude is unprecedented: 514 basis points of increase between the January 2021 low (2.65%) and the October 2023 high (7.79%), in less than three years. No prior cycle — including Volcker — had produced such rapid variation. For the detail of the 2024-2026 phase in continuity with prior cycles, the cluster’s next satellite extends the analysis.

Comparative reading and the use of historical depth

Comparing these five cycles yields several observations. First, extreme levels (above 10% or below 3%) are rare: the series spends about 80% of its observations between 4% and 9% since 1971. Second, transitions between regimes are sometimes slow (Greenspan disinflation over thirteen years) and sometimes extremely rapid (COVID cycle in under three years). Finally, each cycle has its signature: the monetary trigger (Volcker), the secular decline (Greenspan), the opaque stability (pre-GFC Bernanke), the administered compression (post-GFC QE), the pandemic volatility (COVID).

A second-order observation: each cycle leaves cohort-level scarring on the outstanding mortgage stock that compounds across decades. The 2020-2021 cohorts now sit on rates more than 400 basis points below MORTGAGE30US, the largest cohort gap in the series. This gap mechanically reduces refinance activity for years to come and effectively freezes part of the existing-home transaction pool — a structural carry-over from the cycle into the next.

This historical depth also helps situate the present in context. A MORTGAGE30US at 6.5-6.9% in May 2026 is neither a historic high (far from 18.45% in 1981) nor a historic low (far from 2.65% in 2021): it is a level close to the empirical mean of the series, slightly above. The pedagogy of the instrument and the Freddie Mac PMMS mechanic show why these levels do not all read as equivalent configurations. For the situation across the long-run affordability record since 1971, the rates-vs-prices frame of the hub MAJEUR explains what these cycles cumulatively produced for household purchasing power, while the cyclical dimension of purchasing power details how this cost varies with the phases. For the live historical series itself, the FRED MORTGAGE30US dataset for the full historical series aggregates every weekly observation since April 1971.

- Five cycles structure the MORTGAGE30US history since 1971: Volcker, Greenspan disinflation, pre-GFC Bernanke, post-GFC QE, COVID.

- The absolute peak of the series remains 18.45% in October 1981, the trough 2.65% in January 2021; total amplitude covers 1,580 basis points.

- The 2021-2023 rise (+514 bp in under three years) is the fastest ever recorded on the series, faster than the Volcker phase.

- The series spends about 80% of its observations between 4% and 9% since 1971; extreme levels are historically rare and tied to identifiable shocks.

Why this typology serves macro analysis

The MORTGAGE30US cycle typology is not a historical curiosity. It is a comparative reference frame that lets any contemporary phase be situated within its fifty-year context. Without this reference, reading the present remains ahistorical. With it, the analyst can identify which past cycles most closely resemble the current phase, which mechanisms were at work then, and which transitions preceded or followed comparable configurations.

This reading grid illuminates the MORTGAGE30US instrument itself. It does not, however, exhaust the questions of cycle transmission to housing prices, transaction volumes, or bubble formation — questions treated separately in the real-estate pillar.

Last updated — 18 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →US Rental Property Real Yield: What Cap Rate and NOI Actually Leave You

A rental listing leads with a yield. Divide the annual rent by the price and the number looks…

Cap Rate Spread: What Rental Yield Pays Over the 10-Year Treasury

A 5% cap rate sounds attractive. But 5% against what? A risk-free 10-year Treasury yields near 4.5% in…

US Rental NOI, Line by Line: What Net Operating Income Really Subtracts

A US rental yield is advertised gross: annual rent over price. Between that number and the income an…