MORTGAGE30US in 2024-2026: Why Fed Cuts Are Not Transmitting as Expected

May 2026: MORTGAGE30US prints around 6.5-6.9% even though the Fed started its cutting cycle in September 2024 and Fed Funds has fallen roughly 150 basis points. Fed-to-mortgage transmission is not operating with historical elasticity. Three competing readings circulate — widened spread, anchored Treasury, distorted MBS.

TL;DR

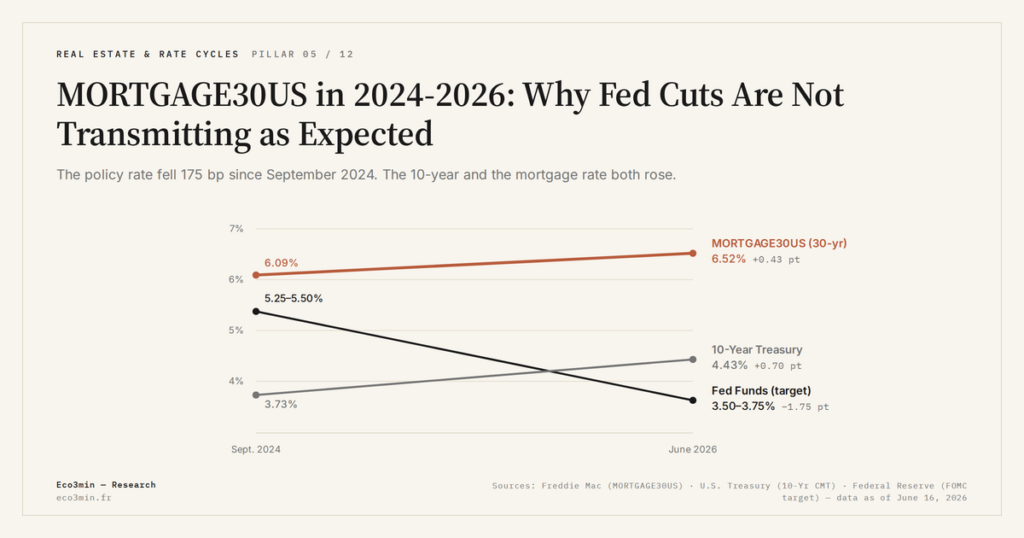

The Fed cut roughly 150 basis points after September 2024, but MORTGAGE30US still prints 6.5-6.9% in May 2026; three competing readings account for why the easing barely reached borrowers.

- The mortgage-to-Treasury spread, historically near 170 basis points, averaged roughly 240 across 2024-2026, absorbing part of every Fed cut before it reaches the borrower.

- The 10-year Treasury itself rose rather than fell: 3.73% the week before the first cut, around 4.2-4.3% in May 2026, held up by an anchored breakeven and a higher term premium.

- The MBS channel stayed distorted after the Fed let its $2.7 trillion agency-MBS peak amortize, leaving price-sensitive buyers such as REITs and bond funds to set the absorption price.

This article lays out the three readings without adjudicating, and notes the current market positioning as reflected in Fannie Mae and MBA releases, without prescribing it.

State of the present: Fed cuts started, mortgage rate flat

On September 18, 2024, the Fed begins its cutting cycle with an initial 50 basis-point cut, taking Fed Funds from 5.25-5.50% to 4.75-5.00%. Four additional cuts follow over the next twenty months. By mid-May 2026, Fed Funds stands around 3.75-4.00%, a roughly 150 basis-point reduction from the July 2023 peak.

Over the same window, MORTGAGE30US barely moved. The rate stood at 6.09% the week before the first Fed cut (week of September 19, 2024); it prints around 6.5-6.9% in May 2026, a net move close to zero or slightly positive over twenty months. If historical transmission had taken hold, MORTGAGE30US should sit closer to 5% than to 6.7%. This divergence calls for explanation.

Three competing readings circulate in macro analysis. None is sufficient alone. All three carry part of the explanation, and their relative weight shifts with the time window considered. To situate this phase in its historical context, the prior cycles for comparison in the historical satellite is the mandatory upstream.

First reading: the MORTGAGE30US – DGS10 spread remains durably widened

The first reading points to the spread. Historically around 170 basis points, the MORTGAGE30US – 10-year Treasury gap averages roughly 240 bp across 2024-2026, some 70 bp above baseline.

Three factors sustain this persistence: the rate volatility premium, which remains elevated while the market doubts the Fed path; the prepayment premium, which does not compress as long as the 2020-2021 cohorts (locked at rates 300 bp below current MORTGAGE30US) do not return to the refinance pool; and the MBS liquidity premium, kept high by the Fed’s gradual exit. For the detailed mechanic, the spread decomposition as diagnostic tool treats each premium individually.

In this reading, the Fed can lower Fed Funds, but as long as the spread stays widened at 240 bp, transmission to the mortgage rate is mechanically bridled. The wider the spread is, the more of any Fed cut is absorbed by the spread itself rather than passed through to the borrower. For the macro cadre across cycles, the mortgage-credit transmission to housing prices documents how this kind of impaired transmission alters the nature of Fed easing phases. Further on this: the US fixed-rate mortgage mechanism.

Second reading: the 10-year Treasury has only partly fallen

The second reading points to the underlying. The 10-year Treasury, itself an input to the mortgage rate, has not followed Fed Funds with the elasticity theory predicts. The week before the first Fed cut in September 2024, DGS10 stood at 3.73%. In May 2026, it prints around 4.2-4.3%, a net increase despite 150 bp of Fed cuts. In the same vein: how rates reshape buying power in housing.

This Fed Funds vs DGS10 divergence comes from two components of the long yield. First, 10-year inflation expectations (measured by TIPS break-evens) remain anchored between 2.2 and 2.4%, with no clear sign that inflation returns durably to the Fed’s 2% target. Second, the term premium — the compensation investors demand for bearing duration risk — has risen significantly since 2023, reflecting elevated U.S. fiscal deficits, net Treasury absorption by domestic buyers who are less price-elastic than the Fed, and the Fed’s own exit from the Treasury market under QT. For the mechanics, see our overview of duration risk. Companion dataset: Our long-run term-premium data.

In this reading, the mortgage rate faithfully follows DGS10 plus spread, and it is DGS10 that has failed to relay Fed policy. The breakdown matters: a Fed cut that does not translate into a lower 10-year Treasury cannot translate into a lower mortgage rate, regardless of how well the spread mechanic is functioning.

Third reading: MBS-channel transmission remains distorted

The third reading is operational. The effective Fed Funds → MORTGAGE30US channel runs through the MBS secondary market, whose health conditions the rate originators can offer to end borrowers.

This market remains structurally distorted since 2022. The Fed, which held up to $2.7 trillion of agency MBS at the 2022 peak, no longer purchases in flows and lets its stock amortize naturally. Commercial banks, after the U.S. regional banking episode of March 2023, materially reduced their appetite for long-duration MBS. Marginal buyers have become REITs, active bond funds, and some international investors — all more price-sensitive than the Fed ever was.

This recomposition of the MBS order book means that any Fed Funds cut must now traverse a secondary market where the absorption price is higher than before 2022. For housing-side leading indicators independent of the rate transmission, building permits as forward housing indicator can inform analysts about supply-side activation before prices or rates move materially. For the real cost of borrowing once inflation is netted out, the real mortgage rate dataset (inflation-adjusted) tracks the deflated series.

Beyond the MBS market itself, the cohort effect amplifies the friction. Borrowers from the 2020-2021 cohorts — who hold loans averaging 2.8-3.5% per Freddie Mac estimates — have no economic incentive to refinance or relocate as long as MORTGAGE30US stays above 5%. This transactional friction keeps the flow of new originations at historically low levels, which in turn affects the inventory of existing homes available for sale and sustains pressure on residential prices. The Fed → mortgage channel is bridled not only on yield but also on the volume of overall mortgage activity. A contiguous angle exists — the DTI-and-rate gate on mortgage approval picks it up.

Combined reading and reported market observation

The three readings overlap. The widened spread reflects both rate volatility (which depends on the Treasury) and MBS distortion (which depends on the buyer flow). The bridled Treasury reflects both inflation expectations and the term premium (itself fed by the Fed’s Treasury-market exit under QT). The MBS distortion reflects the exhaustion of Fed support and the absence of natural replacement at the same scale. None of the three is exclusive; the three operate simultaneously with varying weights.

On the reported observation side, market publications document a coherent positioning. Per the Fannie Mae Economic & Strategic Research Group April 2026 ESR Forecast, and the May 2026 MBA Mortgage Finance Forecast, a return of MORTGAGE30US to the 5.5-6% zone has historically been associated with a normalization of existing-home transactions — without either institution prescribing a timing for that return. This observation is reported here without validating or prescribing it; it appears in the market debate and constitutes an analytical reference point. For the broader frame beyond the MORTGAGE30US instrument, the rates-vs-prices frame from 1971 to today in the hub MAJEUR situates these levels within the long-run decomposition.

On the structural cost-of-financing side, the Fed-to-household transmission in the sub-pillar lays out how this transmission failure is felt at the household purchasing-power level, independent of the nominal mortgage rate.

Many expected a mechanical decline in the mortgage rate at the pace of Fed cuts (“150 bp of Fed cuts equals 150 bp of mortgage cuts”). This expectation conflates the policy rate (short instrument) with the mortgage rate (long composite, which tracks DGS10 plus spread). Historical transmission has varied from 0.5 to 1.5 across regimes; assuming it would equal 1.0 in 2024-2026 ignored the structural distortion of the post-QT MBS market.

What impaired transmission implies for macro reading

The 2024-2026 phase adds a textbook case to the historical typology of MORTGAGE30US cycles: a Fed easing cycle that transmits only partially to the long instrument. This case suggests that the transmission coefficients of the 2010s — calibrated with the Fed as a structural MBS buyer — do not apply mechanically to the 2020s without permanent QE.

For the macro analyst, the practical implication is clear: tracking only Fed Funds to anticipate the mortgage rate is insufficient. Tracking the triplet (Fed Funds, DGS10, MBS-Treasury spread) provides decomposed information and identifies which of the three components is moving and which remains stuck. The frame applies beyond 2026: as long as the composition of the MBS order book remains structurally different from before 2022, this decomposed reading will remain more informative than the monolithic reading of the mortgage rate. Comparable easing cycles in the past — notably 2007-2008 and 2019-2020 — saw mortgage transmission supported by active Fed MBS purchases. The 2024-2026 episode is the first easing cycle in nearly two decades without that institutional underpinning, which by itself justifies treating the current transmission impairment as a regime feature, not a transitory anomaly.

This logic also illuminates the Fed’s own communications. FOMC statements from 2024-2025 document explicit attention to transmission through housing financing conditions, without operational commitment on the QT pace. This stance suggests the Fed views the MBS friction as essentially structural rather than cyclical, and that it does not envisage redeploying QE as a mortgage-specific tool absent a materialized recession. For the analyst, this means that a rapid return of the spread to 170 bp would likely require either a slow normalization of the MBS order book over several quarters, or a negative shock to housing demand that reduces prepayment uncertainty. Neither path reduces to Fed Funds → MORTGAGE30US transmission at a coefficient of 1.0.

Last updated — 18 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →US Rental Property Real Yield: What Cap Rate and NOI Actually Leave You

A rental listing leads with a yield. Divide the annual rent by the price and the number looks…

Cap Rate Spread: What Rental Yield Pays Over the 10-Year Treasury

A 5% cap rate sounds attractive. But 5% against what? A risk-free 10-year Treasury yields near 4.5% in…

US Rental NOI, Line by Line: What Net Operating Income Really Subtracts

A US rental yield is advertised gross: annual rent over price. Between that number and the income an…